Filtered by Subscriptions: Emerging Markets Economics Use setting Emerging Markets Economics

EM GDP growth picked up in the second half of 2024 but faces headwinds this year from tight policy at home and challenges abroad. Our growth forecasts generally sit below the consensus. Monetary easing will continue but, outside Asia, high inflation means …

20th February 2025

The decision by the US and Russia to “lay the groundwork” to end the war in Ukraine marks a potentially significant turning point after three years of conflict. Negotiations will take time and the macroeconomic implications will depend on the features of …

18th February 2025

We doubt that Donald Trump’s reciprocal tariff threat, nor his broader protectionist agenda, are priced in markets fully. We expect US Treasury yields and the dollar to edge up as these tariffs come into effect. In our view, this, alongside continued …

The outcomes of central bank meetings over the last few weeks underscore the point that Asia will lead the next phase of the EM monetary easing cycle this year, alongside Mexico. Meanwhile, there are a handful of EM central banks (particularly in Central …

17th February 2025

If the Trump administration pursues a reciprocal tariff strategy rather than a 10% universal tariff, then it could result in a smaller rise in the overall effective tariff rate than we have assumed. But while most DMs would come out relatively unscathed, …

13th February 2025

After last month’s shock postponement, South African Finance Minister Enoch Godongwana is finally expected to present a 2025 national budget on 12th March. But the ANC and DA have been arguing about fiscal plans, and we think Mr Godongwana faces a …

7th March 2025

Argentina's President Javier Milei has made impressive progress in turning the economy around, but the key question now is whether these achievements can be sustained. Our EM team held this online briefing to discuss the work Milei still needs to do and …

6th March 2025

The latest PMIs suggests that the weakness in EM manufacturing at the end of last year has continued into 2025. While the events of today have highlighted the uncertainty around Trump’s trade policy, tariffs will prove another headwind to EM manufacturing …

3rd February 2025

The Trump administration’s pausing of US aid is a big headwind for many conflict-ridden economies (including Syria and Ukraine) as well as parts of Sub-Saharan Africa, but is unlikely to move the macro needle for most EMs. The potentially bigger …

30th January 2025

March 6 will mark one year since Egypt embarked on a dramatic shift back to orthodox policymaking. So far, the authorities have stuck to most of their pledges. But has enough been done to deliver strong and sustained growth? Which areas still require …

29th January 2025

This is a revamped version of our quarterly Financial Risk Monitor to include commentary and analysis of our latest EM risk indicators. Currency risks remain low, but fiscal vulnerabilities continue to lurk Financial vulnerabilities remained near …

EM GDP growth picked up in the second half of 2024 but faces headwinds in 2025 from tight policy at home and challenges abroad. Our growth forecasts generally sit below the consensus. Monetary easing will continue but, outside Asia, high inflation means …

28th January 2025

India’s outbound tourism market is poised to become one of the world’s largest over the coming years. The Maldives and the UAE are arguably the biggest beneficiaries, though Oman and Thailand are well placed to take advantage too. Other EMs – particularly …

27th January 2025

Having hit a record high, we expect the trade-weighted US dollar to climb further in 2025. While the short-term danger that a strong dollar poses to the world economy tends to be overblown, the bigger risk is that is worsens external imbalances which …

24th January 2025

China’s surging exports have been gaining international attention, but concerns about overcapacity have focussed on “strategic sectors”. Far less acknowledged is the fact that China has been gaining significant global export market share across the board, …

22nd January 2025

We are pessimistic about the outlook for most emerging market assets in 2025, due to the effects of Donald Trump’s agenda, slowing Chinese activity, subdued commodity prices, and domestic challenges. Trump’s first day in office proved a decent one for …

Capital outflows from EMs have picked up again over the past few weeks amid a strengthening of the US dollar and broad increases in bond yields, but also country-specific issues – most notable declining optimism about the outlook for India’s economy and …

20th January 2025

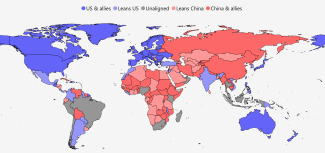

The Shape of the Fractured World in 2025 The share of the fracturing global economy that is accounted for by China and its geopolitical allies contracted in 2024, leaving it under a third the size of the US bloc at the start of 2025. This fall was in part …

17th January 2025

EM sovereign FX debt issuance surged over the past year and at the start of 2025, albeit with many sovereigns returning to global markets and issuing at high interest rates. Borrowing does not look excessive and there’s unlikely to be a further sharp rise …

14th January 2025

If Donald Trump were to impose a universal 10% tariff on US imports, we wouldn’t expect widespread reshoring of manufacturing production back to the US. And if it were accompanied by a 60% tariff on Chinese imports, the main beneficiaries would be other …

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

Brazil’s public finances have been in the headlines for all the wrong reasons over the past month. But while an extreme case, the combination of a large budget deficit and limited political will to rein it in isn’t unique to Brazil. Indeed, Mexico, …

The small fall in the aggregate EM manufacturing PMI in December and the declines in headline PMIs for most countries suggests that EM industry lost some pace at the end of the year. We think manufacturing activity will remain fairly subdued over the …

2nd January 2025

Tab le of Key Forecasts Overview – Headwinds to growth will remain strong in 2025 and our forecasts lie below the consensus. While more protectionist US trade policy will hit China and Mexico, the impact for most is likely to be limited. Currencies will …

19th December 2024

EM GDP growth picked up in the second half of the year but faces headwinds in 2025 from tight policy at home and challenges abroad. Our growth forecasts generally sit below the consensus. Monetary easing will continue but, outside Asia, high inflation …

16th December 2024

Capital inflows into EMs have been resurgent over the past few weeks amid a broader improvement in global risk appetite. Looking ahead, however, likely policies from President-elect Trump point to a renewed strengthening in the US dollar – an environment …

12th December 2024

2025 will be a far quieter year in terms of elections than this year was. But there are some key votes that will, among other things, determine whether Argentina’s President Milei builds support for his radical stabilisation plan and whether the Czech …

10th December 2024

The declaration of martial law by Korea’s president is an extraordinary step that seems likely to trigger either the suspension of Constitutional democracy in Korea or the president’s own rapid impeachment and removal. For investors the key question is …

3rd December 2024

The pick up in the aggregate EM manufacturing PMI in November was largely driven by China. Elsewhere, manufacturing activity looks as though it will remain relatively soft into next year. The surveys suggest that goods price pressures picked up last …

2nd December 2024

We held an online session on US import tariffs on 26th November. (See a recording here ). In this Update we answer the questions we were most asked. What are Trump’s motives for threatening tariffs and will he follow through? Trump has spoken about using …

29th November 2024

EM GDP growth ticked up in Q3 but is likely to fall short of expectations over the coming quarters as stimulus in China disappoints and still-tight monetary policy takes it toll. For most EMs, a universal 10% tariff on US imports – our working assumption …

27th November 2024

Amid the Trump Trade, capital outflows from EM financial markets have persisted over recent weeks. Looking ahead, we expect the US dollar to strengthen further, suggesting that outflows will continue. This will not be a problem for most EMs, but those …

26th November 2024

We discussed the global impact of higher tariffs in a Drop-In on Tuesday, 26th November. Click here to watch the 20-minute online briefing. In this Focus, we construct a framework to explore the channels through which an import tariff works, which we use …

25th November 2024

Friendshoring into India has for the most part been limited to high-end manufactured goods, but broader supply chain reconfiguration into the country could take place if the Trump administration imposes a 60% tariff on China. Trump has also been critical …

21st November 2024

The experience of the first Trump administration suggests that other countries will retaliate to the imposition of new US tariffs but in a way that is measured and minimises the risk of escalating tensions with Washington. The imposition of …

20th November 2024

We held a series of client meetings in the US last week which focused on the implications of Trump’s victory in the US election and the spillovers to EMs. This Update answers some of the most frequent and important questions that came up. What impact will …

US President-elect Donald Trump’s plans to curb immigration and undertake a mass deportation of undocumented migrants could boost labour supply in countries that are the source of migrants. But there could be social and fiscal costs, as well as lower …

18th November 2024

The environment of higher US Treasury yields and a stronger dollar that we think will accompany a second Trump administration is one that, historically, has been associated with crises in EMs with large macro imbalances. The good news is that currency …

12th November 2024

Despite the tick-up in the EM manufacturing PMI in October, manufacturing activity appears to have remained soft and we think this will be the case over the rest of the year. The surveys suggest that goods price pressures were contained last month, but …

4th November 2024

We think that if Vice President Harris wins the US presidential election next week, she would be more likely to stick to policy continuity, and EM risk premia would remain low. If former president Trump is elected, we would expect an initial adverse …

1st November 2024

This is a revamped version of our quarterly Financial Risk Monitor to include commentary and analysis of our latest EM risk indicators. Currency risks ease further, regional divergence among fiscal risks Financial vulnerabilities have declined further …

30th October 2024

EMs are playing a growing role as substitute markets for Chinese exporters that face rising trade barriers in DMs. A second trade war with a re-elected President Trump would only accelerate that shift. It is plausible that a sizeable portion of the loss …

Our measure of capital outflows from EMs has jumped to its highest level since July 2022 amid the recent surge in US Treasury yields and strengthening of the dollar. If Donald Trump wins the US election, there is plenty of scope for these market moves to …

29th October 2024

EM GDP growth picked up in Q3, but we expect growth to slow over the coming quarters - despite the recent stimulus announcements in China. The threat of more protectionist trade policy in the US poses an additional downside risk to our already …

24th October 2024

We held online Drop-In sessions this week to discuss how we factor the US election into our thinking on the macro and market outlook for the US and other parts of the world. See here for a recording of the session focused on the US and here for the rest …

A victory for Donald Trump in the US election would probably result in higher US Treasury yields and a stronger dollar. That’s an environment in which central banks in EMs with strained balance sheets (notably Turkey) could hike rates and others that are …

The outcomes of the EM central bank meetings since the beginning of October underscore the point that Asia will lead the next phase of the EM easing cycle. Central banks in Central and Eastern Europe and Latin America are slowing the pace of (or pausing) …

21st October 2024

Several EMs have reached provisional agreements with creditors to restructure their sovereign debts in recent months, including Zambia, Ukraine, Sri Lanka and Ghana. In principle, restructurings should pave the way for improved fiscal positions, stronger …

17th October 2024

The BRICS+ summit in Russia next week is likely to see another push on expansion, mainly to close allies of China and Russia. But limited economic benefits for potential new members, divisions among existing members, and concerns (for some) about …

15th October 2024