Roles

Sectors

Filtered by Region: G10 Use setting G10

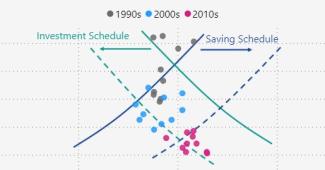

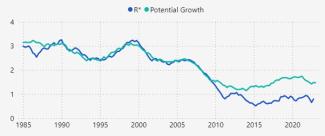

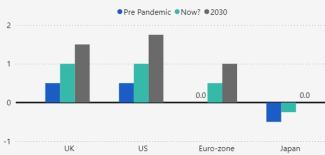

Chapter 2: How will the savings/investment balance affect r*? …

17th October 2023

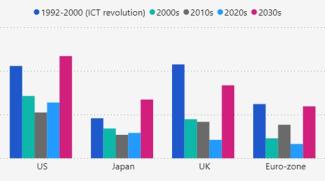

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

Further evidence of economic strength in September The 0.3% m/m rise in industrial production in September is another sign that the real economy remains in solid shape. Production was hit by a slight 0.3% m/m drop-back in utilities output, but that was …

This page has been updated with additional analysis since first publication. Consumption solid heading into Q4 The unexpectedly-strong 0.7% m/m rise in retail sales in September continues the theme of consumer resilience in the face of higher interest …

What will a world of structurally higher interest rates look like? How will central bank behaviour change in the coming years? What will this mean for market returns? Our senior economist team hosted a special online briefing all about their new work …

This page has been updated with additional analysis since first publication. Wage growth passed its peak, but it will fall only gradually Cooling labour market conditions appeared to start feeding through into an easing in wage growth in August. That …

RBA will probably hike rates in November The minutes of the RBA’s October meeting support our view that the Bank will deliver a final 25bp rate hike at its November meeting. While the Bank decided to keep rates unchanged at that meeting, it kept …

This page has been updated with additional analysis since first publication. RBNZ to remain on hold as inflation continues to soften With price pressures on track to moderate further, we think that Reserve Bank of New Zealand won’t lift rates any higher. …

16th October 2023

The Bank of Canada’s quarterly surveys show that businesses’ inflation expectations continue to decline, albeit slowly, and point to a growing risk that the economy will fall into recession. Accordingly, we continue to doubt that the Bank will raise …

September saw sharp drawback in lending The jump in lending in August proved temporary as net lending to commercial property totalled just $13.5bn in September, below the average for 2023 thus far. This took total outstanding real estate debt to $5.5trn. …

Manufacturing losing momentum The surprise fall in manufacturing sales volumes in August reduces the chance of GDP rising by any more than the initial preliminary estimate of a 0.1% m/m gain, and means a second consecutive contraction is still on the …

The job-to-applicant ratio has usually signalled earlier than the Tankan that the labour market has taken a turn for the worse. But despite the recent fall in the number of jobs relative to applicants, we still think that the labour market will soon start …

There are growing indications that household finances are coming under pressure as mortgagors struggle with rising debt-servicing costs. Although households benefit from substantial liquidity buffers, we suspect they won’t be rushing to run those down to …

The fall in house prices in September shows just how quickly conditions in the housing market have shifted and the plunge in the sales-to-new listing ratio points to more weakness to come. That is another reason to expect the Bank of Canada to cut …

13th October 2023

Confidence suffers from renewed inflation concerns The sharp fall in the University of Michigan consumer sentiment index to a five-month low of 63.0 in early October, from 68.1, probably reflects the hit from recent financial market moves, as well as …

There appears to be growing support at the Fed for the idea that the recent sell-off in long-term Treasuries reduces the need for further policy rate hikes, but the more persuasive reason for the Fed to pause is that inflation is continuing to ease …

Almost as fast as gilt yields rose (see here ) they have subsided. After surging from 4.68% on 2 nd October to a 21-year high of 5.11% last Friday, the 30-year gilt yield dropped to 4.72% on Thursday, although it has since ticked up to 4.85% on the back …

The latest activity and survey data have provided even more evidence that the resilience in activity in advanced economies over the first half of 2023 is now fading. High interest rates are clearly weighing on credit growth, and a further rise in debt …

Economy probably won’t overheat The IMF this week revised up its forecast for Japan’s 2023 GDP growth from 1.4% to 2.0%, broadly matching our own. With activity rising much faster than its sustainable rate, any remaining spare capacity in the economy has …

What to expect from a change of guard The headlines this week have largely been dominated by the last leg of campaigning ahead of New Zealand’s general election on October 14 th . The latest opinion polling suggests that five parties are likely to cross …

Surging interest rates caused mortgage demand to slump in Q3 at the same time as rising defaults led lenders to tighten mortgage credit conditions. Similarly, it became more difficult to secure commercial real estate loans. We expect availability of …

12th October 2023

This page has been updated with additional analysis since first publication. Core inflation to remain on downward trend The 0.3% m/m rise in core consumer prices in September suggests, at face value, that the downward trend in core inflation may be …

Higher interest rates weighed sharply on households’ demand for mortgages in Q3 and banks expect demand for mortgages to fall further in Q4. This is a clear sign that higher interest rates are working. And our forecast that mortgage rates will stay above …

We think euro-zone equities’ recent run of underperformance relative to those in the US will extend over the next couple of years, as bond yields fall back and enthusiasm around “AI” continues to grow. With the bond market sell-off seemingly having abated …

This page has been updated with additional analysis since first publication. August’s resilience won’t prevent contraction in GDP in Q3 The 0.2% m/m rise in real GDP in August followed July’s 0.6% m/m contraction and will raise hopes that the economy has …

Surveyors reported the most widespread price falls since February 2009 in September as mortgage rates of over 5% took their toll. Looking ahead, a further slide in house prices appears inevitable. The drop in the past prices balance to a fresh 14-year low …

Most of the recent surge in net migration has been driven by the increased arrival of foreign students, who generally spend less, work fewer hours and demand less housing than the average Australian. On balance though, the surge in net migration probably …

This page has been updated with additional analysis since first publication. Non-residential investment probably declined in Q3 Machinery orders are on track for a fall across the third quarter, consistent with our forecast of a decline in business …

Minutes stress uncertainty over economic outlook Despite the ‘higher for longer’ message from the Fed’s updated rate projections last month, the minutes from the September FOMC meeting suggest that officials’ confidence in those forecasts is limited, with …

11th October 2023

Overview – The outlook for offices is negative across all markets, but we expect substantial differences across the 17 metros we forecast. We now think Seattle, San Francisco and Austin will see vacancy rise by more than 5%-pts over 2023-25, taking the …

The recent strength of core inflation compared to that in the US is mainly due to a rebound in durable goods prices. That has little to do with demand, which has weakened to a greater extent in Canada, suggesting that either the earlier depreciation of …

Labour has made housing a major theme of its conference, and the party’s attitude towards New Towns and social housing means that the next election could prove a turning point in the structure of the UK housing market. Over the past 30 years successive …

10th October 2023

Surging Treasury yields have pushed mortgage rates above 7.5%, higher than we had anticipated. If these borrowing rates persist, lending and sales volumes could fall even further in the near term creating a risk that house prices fall rather than stagnate …

Any fall in bond prices resulting from higher bond yields won’t affect the BoJ’s balance sheet unless the Bank decides to sell its holdings. By contrast, rising interest payments on commercial banks’ reserve holdings could create losses, though those …

Central banks in both Australia and New Zealand are likely to retain their hawkish bias in the near term, given that inflation is far from tamed in either country. While we think the RBNZ's tightening cycle is over, we expect RBA to hand down one final …

The recent shift towards looser fiscal policy in Italy and increase in sovereign bond yields once again have raised concerns that investors may lose confidence in Italy’s ability to sustain its debt burden. We don’t think this will morph into an acute …

9th October 2023

Welcome to a world of higher interest rates. This in-depth analysis shows you how the structural forces that have weighed on equilibrium real interest rates over the past two decades have faded, and the powerful new drivers that are likely to push them …

Our latest Chart Pack on Japan's economy is embedded below. With the economy growing at an above-trend pace, the labour market should soon start to tighten again. There are mounting signs that a virtuous cycle between wages and prices is starting to form …

The US stock market has rallied so far today and is on track to bring to an end a spell of weekly losses. Although we think that the proximate cause of this recent weakness – rising bond yields – has largely run its course, we don’t expect the fortunes of …

6th October 2023

The further rise in home listings in September and likelihood that mortgage rates will increase amid the global bond market sell-off suggests that house prices will soon fall again. While employment rose strongly in September, the fall in hours worked …

We expect the euro-zone economy to struggle over the next 18 months, and a mild recession in the coming quarters looks more likely than not. Headline and core inflation should keep falling, but the labour market will remain tight, keeping wage growth …

Rising long rates a fiscal rather than monetary problem Surge in long yields not all due to higher for longer The conventional wisdom is that the recent surge in Treasury yields is a reaction to the Fed’s “higher for longer” message. But that surge has …

The recent rise in gilt yields has been almost as fast as the political furore over the cancellation of the northern leg of HS2 this week. The 30-year gilt yield rose from 4.68% at the start of last week to a 20-year high of 5.06% at the time of writing …

Wage pressures easing This page has been updated with additional analysis since first publication. The strong headline employment gain in September was entirely due to a rebound in educational services employment, with employment elsewhere edging down. …

Despite strong payrolls, wage growth continues to slow The surprisingly strong 336,000 increase in non-farm payrolls in September adds to the evidence on real activity that the economy is holding up well despite the headwind from higher interest rates. …

What to make of the bond market sell-off? We have covered the implications of the bond sell-off for the global economy here . Three additional points are worth making in relation to the euro-zone. First, the increase in yields and associated tightening of …