- Our proprietary EM financial risk indicators show that economic and financial vulnerabilities in most EMs were low coming into the energy shock. Our aggregate EM currency crisis risk indicator remains near multi-decade lows, suggesting that the risk of high energy prices leading to balance of payments strains is much lower than it was in the aftermath of the start of the war in Ukraine. That said, currency crisis risks have increased the most in Turkey as FX reserves have fallen, while risks remain high in Egypt.

- There are no countries showing up as “high” banking crisis risk, although several EMs with existing banking vulnerabilities and high interest rates are approaching our risk thresholds. Banking sectors in the Middle East, which appear most vulnerable to spillovers from the Iran war, were among the strongest across EMs before the conflict started. And while sovereign debt vulnerabilities remain acute in a handful of smaller EMs, the overall story is that fiscal risks have continue to fall, particularly in Africa.

- Banking risk: Our latest aggregate EM banking crisis risk indicator edged down a touch, leaving it slightly above its average over the past decade. There are currently no countries at “high risk” of a crisis, although a handful of larger EMs have moved towards the higher end of “moderate risk”.

- Currency risk: Our latest aggregate EM currency crisis risk indicator ticked up slightly, but this still left it close to its lowest level of the past two decades. EMs came into the Iran war with strong external positions and while some oil importers will experience balance of payments strains, these are likely to be isolated.

- Sovereign risk: Our latest aggregate EM sovereign default risk indicator edged down to a five-year low, with our regional indicator for Africa falling further too. There are seven EMs at “high risk” of a debt crisis, which remains the joint-lowest number in the post-pandemic period.

- Spotlight: Turkey, Hungary, Colombia and Kenya.

To explore the data please visit our interactive dashboard. This EM Focus serves as a primer.

|

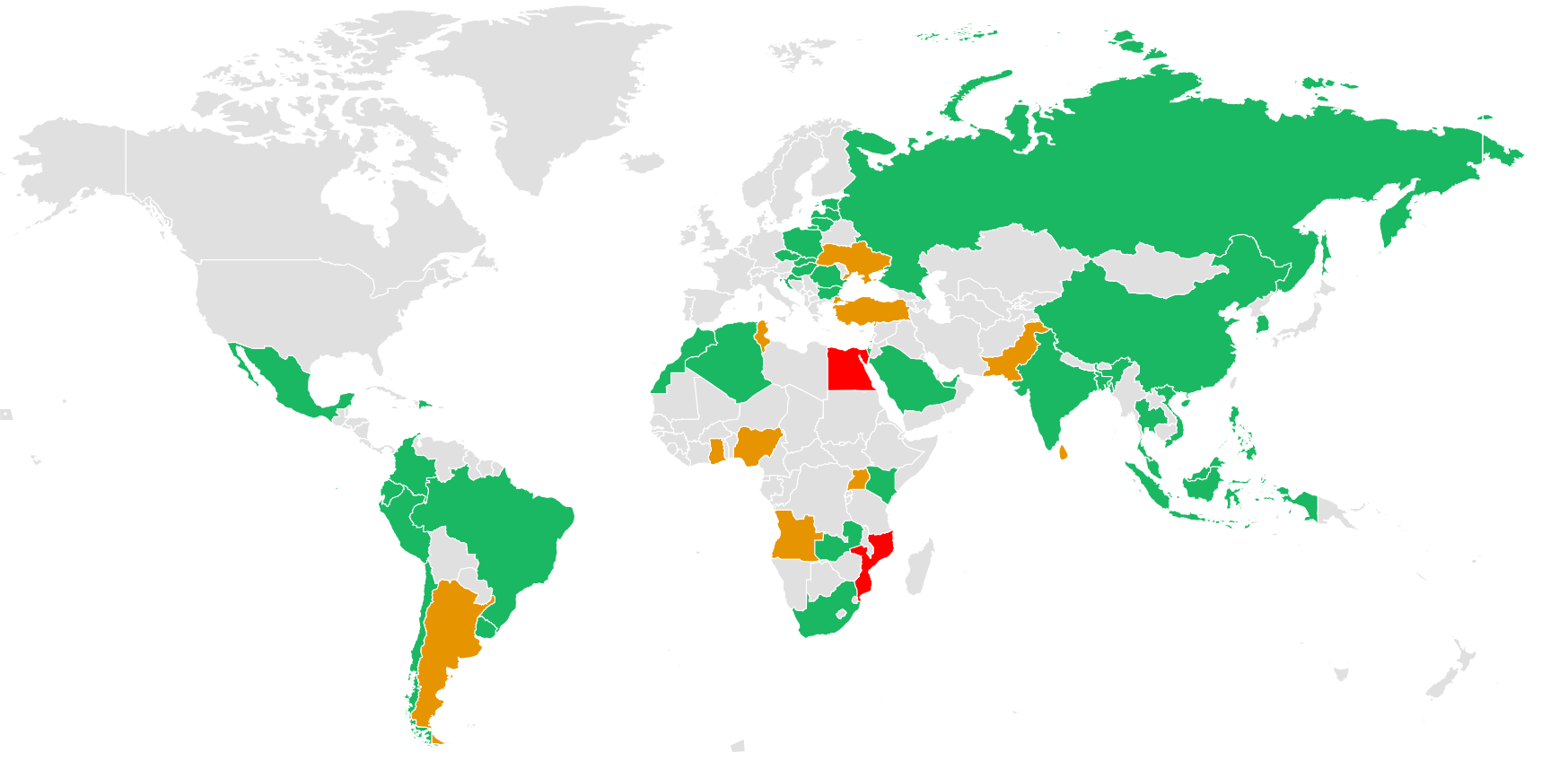

Chart 1: Overall Financial Risk Heatmap (Latest = Q1 2026) |

|

|

|

Sources: Various, Capital Economics |

Banking Risk

Banking risks remain low in most EMs

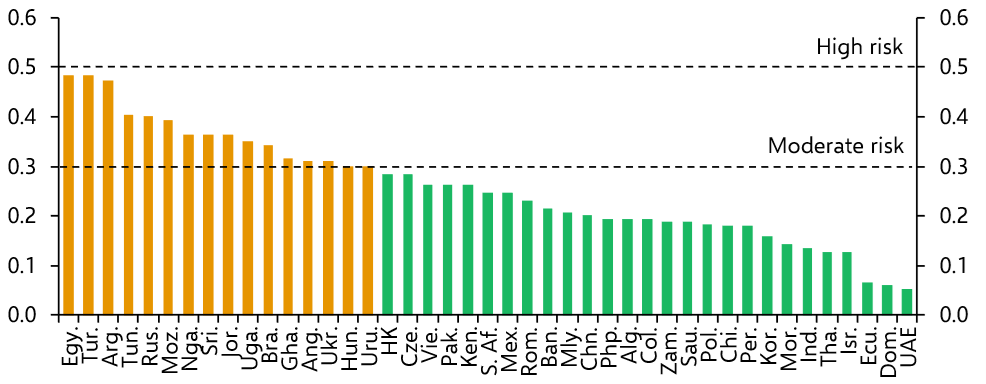

- Banking crisis risks are “moderate” in around one third of EMs that we cover, with Turkey, Egypt, Argentina, Tunisia and Russia continuing to stand out as among the highest. (See Chart 2.) This is driven in part by high interest rates and previous booms in credit.

- Indeed, tight monetary conditions have pushed our measure of banking risk to a five-year high in Turkey and Nigeria. Banking risks have fallen in Russia. Our indicator breached the “high risk” threshold a year ago. It has come down due to slower credit growth. But rising NPLs, high real interest rates and weak GDP growth remain a concern.

- Our banking risk indicator has remained stable in Brazil at “moderate”, despite a continued rise in NPLs. Broader measures of banking sector health, including capital ratios, remain strong. Banking risk in Hungary edged up slightly into “moderate” in the past year, although there are very few imbalances in the banking system.

- The Middle Eastern banking sectors are vulnerable to the spillovers from the Iran war, but they are starting from a strong position. Our indicator for Saudi Arabia fell from “moderate” to “low” in the run-up to the conflict the UAE remained “low risk”. NPLs may rise over time if debt problems surface but capital ratios across MENA are among the highest in the EM world.

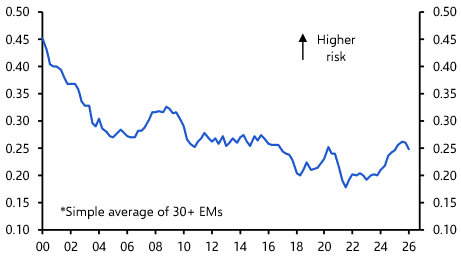

- The big picture is that EM banking risks look low. Although our EM indicator drifted higher throughout 2025 (see Chart 3), credit growth has slowed in most EMs and monetary conditions have become less restrictive. We categorise two-thirds of countries as “low risk”.

- Capital adequacy ratios are below our risk thresholds in almost all EMs. Recent declines in our banking risk indicators have been largest in Saudi Arabia and Pakistan. Those with the lowest banking risk include India, Indonesia, Poland, Thailand, the UAE and Chile.

|

Chart 2: CE Banking Crisis Risk Indicator (Latest) |

|

|

|

Sources: Various, Capital Economics |

|

Chart 3: CE EM Banking Crisis Risk Indicator |

|

|

|

Sources: LSEG, Capital Economics |

Currency Risk

FX vulnerabilities isolated in selected EMs

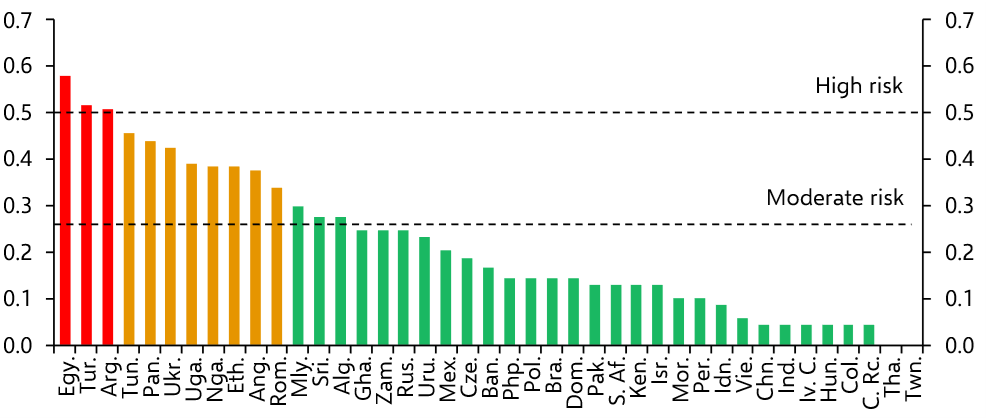

- Most EMs are at “low risk” of a currency crisis, while Egypt, Turkey and Argentina are at “high risk” given their fragile external positions.

- The Iran war will worsen FX vulnerabilities in some EMs but ease them in others, reflecting the impact of high oil prices on inflation and the balance of payments. Egypt and Turkey are among the most vulnerable. Our currency crisis risk indicator for Turkey has risen sharply since the start of the Iran war, largely due to a slump in FX reserves. (See our Spotlight section.)

- Tunisia, Ukraine, Romania and Sri Lanka are net energy importers and stand out as among the most vulnerable “moderate risk” EMs. They run current account deficits that could widen amid a prolonged period of higher oil prices. The risks to the Tunisian dinar look acute.

- In contrast, high oil prices should provide a net boost to net energy exporters like Argentina, Nigeria and Angola. Argentina remains “high risk” on our currency indicator but a sustained terms of trade boost could help to run current account surpluses and accumulate FX reserves. The oil boost comes at a key time for Angola as it has experienced one of the largest increases in our risk indicator in the past year, reflecting a widening budget deficit and falling FX reserves.

- Asian countries are among the most dependent on energy supplies from the Middle East, but we categorise all countries with “low” currency risk. That reflects sound external positions, strong export growth (which sustains trade surpluses) and high FX reserve coverage.

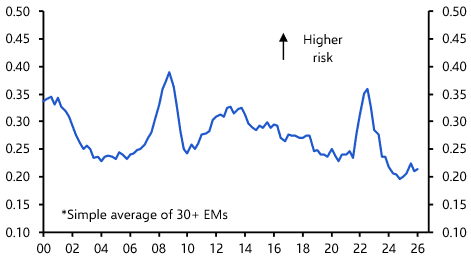

- The bigger picture is that our aggregate EM currency crisis risk indicator remained near multi-year lows before the Iran war started. (See Chart 5.) Currency risks in oil importers are likely to rise as oil prices stay high for longer, but EMs are in a strong position to cope in the event of renewed balance of payments strains.

|

Chart 4: CE Currency Crisis Risk Indicator (Latest) |

|

|

|

Sources: Various, Capital Economics |

|

Chart 5: CE EM Currency Crisis Risk Indicator |

|

|

|

Sources: Various, Capital Economics |

Sovereign Debt Risk

Sovereign debt risks falling in the majority of EMs

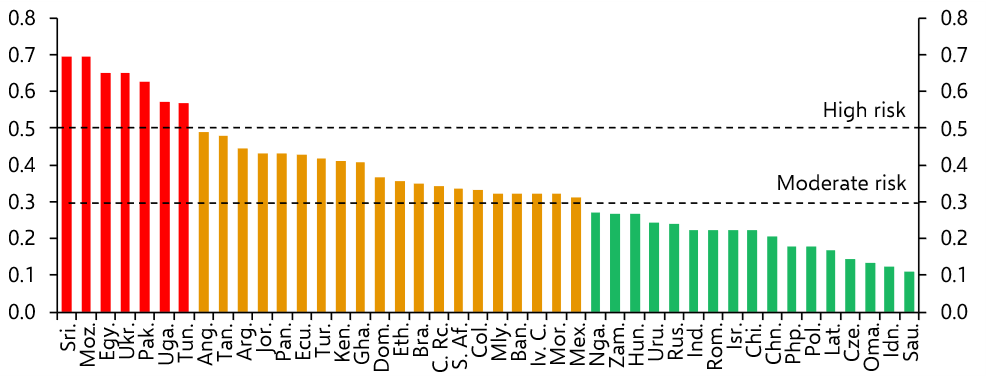

- We categorise seven EMs with “high” sovereign risk, which remains the joint-lowest in the post-pandemic period: Sri Lanka, Mozambique, Egypt, Ukraine, Pakistan, Uganda and Tunisia.

- Many of these are perennial high sovereign debt risk EMs with weak public finances. The pathway to improving fiscal positions will likely require a debt restructuring in some cases, particularly in Mozambique and Tunisia.

- Some EM governments that subsidise fuel prices will experience larger fiscal deficits this year, but most tend to be energy producers (e.g. Algeria and Angola). Egypt and Tunisia look the most concerning, given their existing fiscal vulnerabilities and large fuel subsidies.

- The oil windfall will provide some relief to the public finances in Nigeria and Angola, but we think this will be spent, keeping their budget deficits large. Angola had already moved closer towards our “high risk” threshold on the back of widening twin deficits before the conflict.

- In the larger EMs with longer-term debt problems, including Brazil, Mexico and Colombia, our sovereign risk indicators have neither worsened nor improved in the past year. Budget deficits remain large and the focus is on the need for more credible fiscal tightening to stabilise debt ratios and lower country risk premia. (See Spotlight for Colombia.)

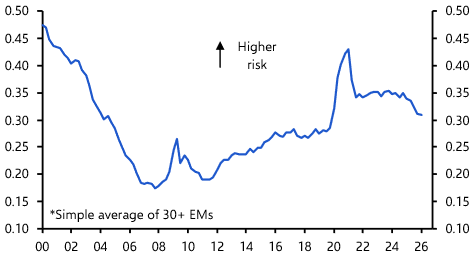

- More broadly, the story for most EMs remains one of falling sovereign debt risk, with our risk indicator declining in twice as many EMs as it has risen in the past year, and our aggregate EM indicator is at a multi-year low. (See Chart 5.) Most of the falls have been in Africa, notably South Africa, Kenya and Zambia, with our regional Africa sovereign risk indicator at a ten-year low. The biggest decline in risk has been in Peru, which is at a pre-pandemic low.

|

Chart 7: CE Sovereign Default Risk Indicator (Latest) |

|

|

|

Sources: Various, Capital Economics |

|

Chart 7: CE EM Sovereign Default Risk Indicator |

|

|

|

Sources: Various, Capital Economics |

Spotlight – Turkey, Hungary, Colombia and Kenya

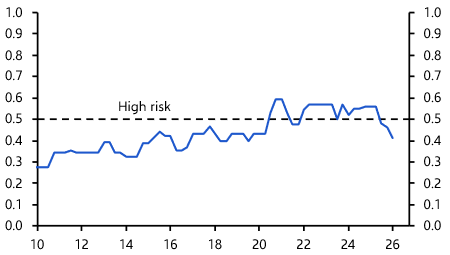

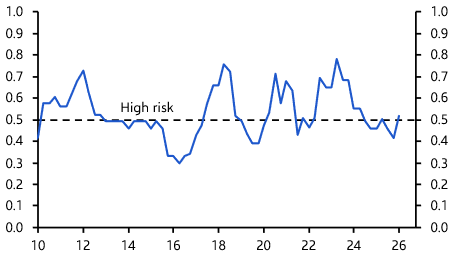

- Turkey has moved back into “high risk” on our currency crisis indicator. The central bank’s FX reserves declined markedly in March amid the start of the Iran war and surge in oil prices, pushing many of the key metrics that we track back through our risk thresholds. FX reserves have rebounded this month, but a prolonged period of high oil prices is a major risk that would result in balance of payments pressures, likely forcing interest rate hikes and policymakers to loosen their grip on the lira.

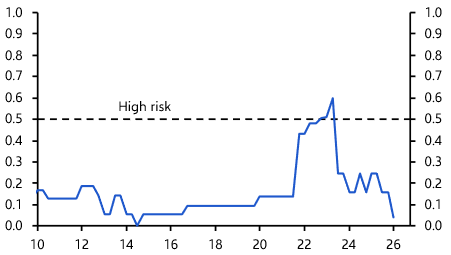

- In contrast, our measure of currency risk in Hungary has fallen to its lowest in a decade, reflecting a sharp rise in FX reserves this year that has reduced external financing constraints. More generally, the external position before the oil price spike was solid, with a current account near balance. The victory for Tisza in the recent election has now brought euro adoption into discussion. While this would eliminate FX risks, euro entry does not look plausible until 2030s.

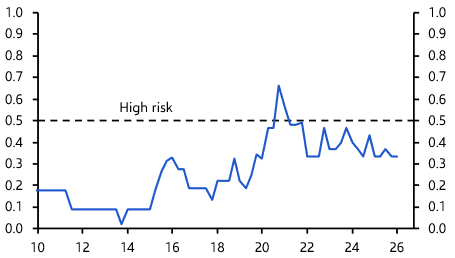

- Colombia has remained at “moderate risk” on our sovereign debt risk indicator. Colombia had already breached many of our thresholds for the size of the budget deficit (which is at almost 6% of GDP) and interest expense ratios but this has been offset to an extent by Colombia’s strong external position and low FX financing needs. The winner of the presidential election in May will need to push through large fiscal tightening to put the public finances on a sustainable footing and reduce risk premia on local assets.

- Kenya moved out of our “high risk” threshold for sovereign debt into “moderate” over the past year, reflecting broader improvements in the country’s fiscal metrics, but we’re sceptical that this will last. Kenya has requested assistance from the World Bank to help with the Iran shock. And while policymakers have raised fuel prices sharply (rather than maintain expensive subsidies), the risks appear skewed towards looser fiscal policy and a wider budget deficit ahead of next year’s election.

|

Chart 8: CE Turkey Currency Crisis Risk Indicator |

|

|

|

Sources: Various, Capital Economics |

|

Chart 9: CE Hungary Currency Crisis Risk Indicator |

|

|

|

Sources: Various, Capital Economics |

|

Chart 10: CE Colombia Sovereign Debt Risk Indicator |

|

|

|

Sources: Various, Capital Economics |

|

Chart 11: CE Kenya Sovereign Debt Risk Indicator |

|

|

|

Sources: Various, Capital Economics |