Filtered by Subscriptions: UK Markets Use setting UK Markets

Activity remains resilient, despite global banking issues The flash PMIs suggest the economy’s strong start to the year was sustained in March. But with the full drag from high interest rates yet to be felt, our hunch is still that the economy will enter …

24th March 2023

Too soon to conclude February’s rebound will be sustained The further rebound in retail sales volumes in February suggests the recent resilience in activity hasn’t yet faded. But we doubt this will last as the drag on activity from higher interest rates …

Too soon to conclude February’s rebound will be sustained The 1.2% m/m rise in retail sales volumes in February was much better than the consensus forecast of a +0.2% m/m rise (CE +0.5% m/m). That suggests the recent resilience in activity hasn’t yet …

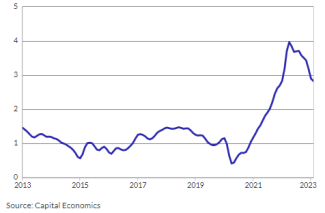

The Bank of England followed the Fed’s example by forging ahead today with a 25 basis point (bps) interest rate hike, taking rates from 4.00% to 4.25%. This could prove to be the last hike of the tightening cycle. But if wage growth and CPI services …

23rd March 2023

Bank of England may not yet be finished in its battle with inflation The Bank of England followed the US Fed’s example by forging ahead today with a 25bps interest rate hike and signalling that it may not yet be finished in its battle with inflation. As a …

Reacceleration in inflation supports the case for another rate hike The reacceleration in CPI inflation in February may be enough to tilt the Bank of England towards raising interest rates from 4.00% to 4.25% tomorrow despite the recent turmoil in the …

22nd March 2023

Reacceleration in inflation may force 25bps rate hike The reacceleration in overall CPI inflation from 10.1% in January to 10.4% in February (consensus 9.9%, BoE 10.2%) and core inflation from 5.8% to 6.2% (consensus 5.7%) may be enough to tilt the Bank …

Pre-election tax cuts in prospect, but risks to the fiscal outlook growing Despite February’s worse-than-expected public finances figures, we still think the Chancellor may have more headroom to cut taxes/raise spending later this year. But the big risk …

21st March 2023

Pre-election tax cuts in prospect, but risks to the fiscal outlook growing The news on the public finances may have raised the Chancellor’s hopes that he will be able to announce a pre-election giveaway later this year. But the big risk is that a further …

While the Credit Suisse rescue might draw a line under that particular institution’s problems, it is clear that confidence in the financial sector overall is still extremely fragile. So regardless of whether more financial institutions run into trouble, …

20th March 2023

The past week has provided a worrying reminder of the fragility of banking systems to rising interest rates. All our analysis on this can be found on our key themes page . Many metrics of financial market functioning have deteriorated worryingly fast and …

17th March 2023

This dashboard tracks medium-term inflation expectations in the US, euro-zone and UK. In a world where the Phillips curve is flat, inflation expectations become the key driver of actual inflation over the medium term. But getting a true handle on …

Close call, but if the situation doesn’t deteriorate further we think there will be a 25bps hike Beyond that, fading of banking worries and stronger data required for more hikes Markets may be underestimating how far interest rates will be cut next year …

16th March 2023

The Budget has taken a bit of a backseat given the renewed worries about the health of the global banking system, but the Chancellor, Jeremy Hunt, was a bit more generous than we expected and probably plans to splash more cash ahead of the 2024/25 …

15th March 2023

Chancellor a bit more generous, but may fall short on long-term growth Today’s Budget has taken a bit of a backseat given the renewed worries about the global banking system, but the Chancellor was a bit more generous than we expected and we suspect he …

This checklist helps clients keep track of the key forecasts announced during the Spring Budget at 12.30pm (GMT) on Wednesday 15 th March. Our more detailed preview is here . We will send a Rapid Response shortly after the speech, we are hosting a “Drop …

14th March 2023

Wage growth eases despite labour market remaining tight The labour market remained tight in January. Even so, the Bank of England will breathe a sigh of relief as wage growth is easing. Together with the collapse of a couple of US banks having tightened …

Wage growth eases despite labour market remaining tight The labour market remained tight in January. Even so, the Bank of England will breathe a sigh of relief as wage growth is easing. But the fallout from Silicon Valley Bank’s collapse suggests that the …

13th March 2023

We have revised up our forecasts for real GDP and no longer think the economy will be quite as weak. This has very little to do with the 0.3% m/m rise in real GDP in January released this morning. Most of that was a rebound after the widespread strikes …

10th March 2023

January’s strength won’t prevent contraction in GDP in Q1 The 0.3% m/m rise in real GDP in January (consensus +0.1% m/m, CE +0.4% m/m) will raise hopes that the economy will escape a recession in 2023 and will increase calls for the Chancellor to splash …

Resurgence in activity unlikely to last The 0.3% m/m rise in real GDP in January (consensus +0.1% m/m, CE +0.4% m/m) leaves the economy in better shape than we had expected just a few months ago. But looking beneath the surface, the figures suggest the …

The numerous “plans for growth” that have been announced by the Government, the Opposition, and various commentators in recent months vary in their analytical rigour but all miss one crucial point: many of the reforms required to lift the UK’s pitifully …

9th March 2023

We expect the Spring Budget on 15 th March to contain some giveaways confined to 2023/24. But a downgrade to the Office for Budget Responsibility’s (OBR) medium-term GDP growth forecasts will prevent an unwinding of the £54bn (1.8% of GDP) of fiscal …

8th March 2023

What will UK Chancellor Jeremy Hunt deliver in his Spring Budget? Will he be able to splash any cash, will he hold back sweeteners until closer to the next general election, or will the OBR’s new economic forecasts tie his hands? Group Chief Economist …

7th March 2023

Brexit looking a bit brighter The economic developments this week were generally positive, starting with news that the Prime Minister, Rishi Sunak, struck a deal with the EU on trading arrangements for Northern Ireland, officially known as the Windsor …

3rd March 2023

Higher interest rates hurt housing, but other borrowing remains strong While January’s money and credit figures suggest that higher interest rates are continuing to act as a drag on the housing market, they appear to be having less influence in other …

1st March 2023

A widening in profit margins could mean that inflation is slower to fall back to the Bank of England’s 2.0% target than we expect. That would cause the Bank to raise interest rates even further than we currently anticipate and/or keep them higher for …

28th February 2023

Higher interest rates hurt housing but not other borrowing January’s money and credit figures suggest that higher interest rates are continuing to act as a drag on the housing market, but they appear to be having less influence in other areas of the …

The more hawkish tone in financial markets this week is justified. Prior to this week, investors seemed to be optimistic that the previous increases in interest rates would be enough to bring inflation back down to the Bank of England’s 2.0% target, and …

24th February 2023

The recent resilience of economic activity has left us comfortable with our view that the Bank of England will raise interest rates from 4.00% now to a peak of 4.50%, rather than to 4.25% as analysts expect, and keep rates at that higher level all year. …

23rd February 2023

There is mounting evidence that households’ pandemic savings will no longer be able to support real spending. That implies from now on, real consumer spending will have to evolve in line with real incomes. The conventional wisdom is that households and …

22nd February 2023

PMIs suggest activity rebounded in February, but we doubt it will last The sharp rebound in the flash UK composite PMI in February suggests that the economy remained resilient to the dual drags from high inflation and high interest rates at the start of …

21st February 2023

Tighter fiscal policy probably still on its way despite borrowing undershoot January’s public finances figures suggest the Chancellor will have scope for some giveaways in his Budget on 15 th March. But with the OBR poised to slash its medium-term GDP …

Tighter fiscal policy probably still on its way despite big borrowing undershoot January’s public finances figures suggest the Chancellor may have scope for some giveaways in his Budget on 15 th March. But with the OBR poised to slash its medium-term …

PMIs suggest activity rebounded in February, but we doubt it will last The sharp rebound in the flash UK composite PMI in February suggests the economy continued to remain resilient to the dual drags from high inflation and high interest rates. But we …

20th February 2023

Being ranked by the Sunday Times as the top UK economic forecaster for 2022 is a great accolade and has generated a lot of interest in what we expect to happen next. Our forecasts for 2023 imply a tougher year than the consensus, with higher inflation …

In a previous edition of the UK Economics Weekly we said that the CPI core services inflation and private sector pay figures released this week would prove pivotal in determining whether the Bank of England raises interest rates further or calls time on …

17th February 2023

Too soon to conclude that retail is coming out of its funk The rebound in retail sales in January was better than expected, had echoes of the leap in US retail sales and suggests that the festive/new year period wasn’t a complete write-off. But while …

2023 may be better than 2022 for retailers, but it will still be a struggle The 0.5% m/m rise in retail sales volumes in January was better than the consensus forecast of a 0.3% m/m decline (CE +0.5% m/m), echoes the leap in US retail sales earlier this …

The UK avoided a recession last year partly because of more spending by households on restaurants and trains and partly because of more investment by businesses in aircraft, cars and cruise ships. This suggests the recovery from the pandemic cushioned …

16th February 2023

Moderating services inflation makes Bank of England’s life easier The fall in CPI inflation from 10.5% in December to 10.1% in January (consensus and CE forecast: 10.2%, BoE forecast: 10.1%), the drop in the core rate from 6.3% to 5.8% and the easing in …

15th February 2023

Moderating services inflation makes Bank of England’s life easier The sharp fall in CPI inflation from 10.5% in December to 10.1% in January (consensus and CE forecast: 10.2%) was the most eye-catching part of today’s CPI release. But it is the easing in …

Wage growth continues to accelerate despite cooling labour demand December’s labour market data showed that, despite an easing in labour demand, labour market conditions stayed tight and the market continued to support strong wage growth. The Bank of …

14th February 2023

Wage growth continues to accelerate despite cooling labour demand December’s labour market data showed that, despite an easing in labour demand, labour market conditions stayed tight and the market continues to support strong wage growth. The Bank of …

13th February 2023

It doesn’t really matter if the economy was in recession last year or not (although according to the technical definition it was not). (See here .) Two other factors are more important. First, recession or no recession, the economy is weak. Real GDP …

10th February 2023

Recession may come this year as resilience recedes The economy escaped a recession in 2022 by the skin of its teeth (£77m to be precise). But with the full drags from high inflation and high interest rates yet to be felt, we think there will be a …

Avoiding a recession in 2023 will prove harder The 0.5% m/m fall in real GDP in December was worse than expected (consensus -0.3%), but the 0.0% change in Q4 (consensus 0.0%, BoE +0.1%) meant that the economy avoided a recession last year by the skin of …

We think business insolvencies may rise to a record high of around 8,400 per quarter by Q2 2024 and take until at least early 2025 to return to a more “normal” level of just over 4,000 per quarter. The total rise in insolvencies above this normal level is …

9th February 2023

Since the full effects of the previous surge in energy prices and the hike in interest rates have yet to be felt, we still think the economy will succumb to a recession this year. Admittedly, pandemic savings and the government’s handouts appear to have …

8th February 2023

While the Bank of England raised interest rates by a further 50 basis points (bps) yesterday, from 3.50% to 4.00%, it hinted that if Bank Rate is not already at a peak, it is very close to one. As we unpacked in our “Drop-In” webinar on this week’s policy …

3rd February 2023