Filtered by Region: G10 Use setting G10

The same questions kept coming up in our client briefings on the 2024 outlook and Group Chief Economist Neil Shearing tackles them in this latest episode of our weekly podcast. He talks about why economic resilience will be increasingly tested and which …

8th December 2023

Markets call the Fed’s bluff on higher for longer Markets abandon higher for longer The Fed may not be quite ready to abandon its tightening bias at this week’s FOMC meeting, but the markets are no longer buying its “higher for longer” mantra. Markets …

The Bank of Canada this week reiterated that strong immigration is putting upward pressure on inflation because housing supply is failing to keep up. Yet the Bank surely can’t be oblivious to the negative impact of high interest rates on construction. …

Inflation concerns easing The plunge in the University of Michigan’s consumer inflation expectations measures in December will give reassurance to the Fed ahead of its meeting next week that there are few signs of inflationary pressures reigniting. …

The further drop in UK market interest rate expectations this week means that investors now think the first interest rate cut will happen in June next year instead of August. And investors are now pricing in an 80% chance of a cut by May. That has led to …

Payrolls boosted by returning strikers The 199,000 increase in November payroll employment included 47,000 workers returning from strikes (30,000 UAW members and 17,000 SAG Aftra members). Stripping out that one-off boost, the 152,000 gain was roughly the …

Services inflation continues to accelerate The economic data released this week seem to vindicate the Bank of Japan’s caution when it comes to abandoning ultra-loose monetary policy. For a start, the timely Tokyo CPI showed that inflation slowed from …

Not higher, not longer Earlier today, the Treasury and the RBA published an updated Statement on the Conduct of Monetary Policy. The revised statement clarified that the RBA’s objective is to return inflation to the mid-point of its 2-3% target. That led …

This page has been updated with additional analysis since first publication. Wage growth will stay strong Regular wage growth accelerated in October and we expect it to stay strong in the coming months as the virtuous cycle between prices and wages …

7th December 2023

We expect the US dollar’s resilience to fade over the next year or so, and forecast it to weaken against most major currencies. There’s been something of a return of the “heads I win, tails you lose” story for the US dollar lately. The “higher for longer” …

Overview – Further declines in GDP in the coming quarters mean that the economy is unlikely to grow at all next year. Weak growth and a return in inflation to the 2% target will leave scope for the Bank of Canada to cut interest rates sharply, with the …

Bank of England to keep interest rates unchanged at 5.25% but retain its hawkish bias It won’t risk fuelling bets on earlier rate cuts by watering down its forward guidance We expect Bank Rate to be cut later, but by more than most expect With the Bank …

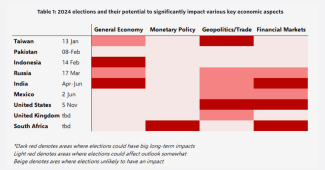

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

Even though we expect the economy to be weaker than the consensus in 2024, we think that lingering constraints on domestic supply will prevent wage growth and services CPI inflation from falling quite as fast as is widely expected. As a result, we think …

Halifax confirms that prices are on the rise again The second consecutive monthly rise in the Halifax house price index in November mirrored the increase in the Nationwide index, confirming that house prices have not only stabilised, but are rising. …

We think that sovereign bond yields in most major economies will generally reach their troughs around the same time over the next year or so. But with the Bank of Japan seemingly set to buck the trend once again, yields there may be an exception. The …

Net trade could remain a drag on growth in Q4 Notwithstanding the slight expansion in the goods trade surplus in October, net trade could subtract from growth this quarter. The rise in the goods trade surplus from a downwards-revised $6.2bn in September …

Property yields rose across all sectors in Q3, but this was offset by a sharp rise in alternative asset yields towards the end of the quarter. As a result, all sectors saw a deterioration in valuations, which pushed the retail sector back into the …

6th December 2023

The Bank of Canada is clinging on to the idea that restrictive policy is still needed to get inflation back to 2%. Nonetheless, with core inflation pressures muted, GDP and house prices falling, and labour market conditions loosening rapidly, it won’t be …

Overview – As core inflation is on track to return to the 2% target by the middle of next year, we expect the Fed to cut interest rates by 25bp at every meeting next year from March onwards, with rates eventually falling to between 3.00% and 3.25% in …

Bank maintains tightening bias, but next move likely to be a cut The policy statement from the Bank of Canada was a bit more hawkish than we expected, with the Bank reiterating that it is still concerned about the outlook for inflation and “remains …

Officials not yet willing to fully endorse rate cut bets; tightening bias could be retained New SEP should confirm rates are at the peak but significant downgrades unlikely We expect the first rate cut in March and 175bp of easing in total next year With …

Imports and exports set for further growth in Q4 Despite the widening in the trade deficit in October, net trade looks set to be only a modest drag on fourth-quarter GDP growth. But the survey evidence suggests renewed weakness in exports may still lie …

Slump in imports only partly due to UAW strike The slump in import volumes in October was partly due to the knock-on effects of the UAW strike in the US, but it also suggests that firms are now drawing down their inventories as demand weakens. That raises …

Falling rates allow mortgage demand to recover Falling mortgage rates sparked a modest uptick in mortgage applications for home purchase in November. Recent falls in Treasury yields mean further falls in mortgage rates are imminent, so the trough in …

GDP growth will continue to disappoint GDP growth was softer than most expected in Q3 and with that weakness set to continue, we think that the RBA is done tightening policy. The 0.2% q/q rise in output fell short of the analyst consensus of 0.4% as well …

Although the relative performance of the three “big-tech” sectors of the S&P 500 has underwhelmed recently, we suspect that they will be at, or near, the front of the pack again in 2024. While the three big-tech “growth-heavy” sectors that contain the …

5th December 2023

November JOLTS data suggest that labour market slack is growing, even as payroll growth remains relatively resilient. With signs pointing to a sharper fall in wage growth ahead, the Fed can be reassured ahead of its meeting next week that that …

First-time buyer (FTB) loan originations have been weak for over a year now. That’s mainly down to higher mortgage rates which have made buying too expensive for many younger adults. And as we think mortgage rates are unlikely to drop much below 6.0% …

Muted ISM services consistent with GDP stagnation; job openings drop back The modest rebound in the ISM services index to 52.7 in November, from 51.8, left our weighted composite index at a level consistent with an outright stagnation in GDP. Admittedly, …

Overview – With higher interest rates taking longer to percolate through the economy, we now think the recession will be shallower and GDP growth will stay weak throughout all of 2024. It’s a softer landing for the economy, but the runway is longer. And …

Given the high bar for further rate hikes, we’re more confident than ever that the Reserve Bank of Australia is done tightening policy. That said, there is a good chance that the cash rate will remain at its cyclical peak for longer than we currently …

RBA is done hiking rates Although the RBA won’t tighten policy any further, there is a good chance that the Bank will hold the cash rate at its current peak for longer than we anticipate. The RBA’s decision to leave rates unchanged at its meeting today …

This page has been updated with additional analysis since first publication. Inflation won’t reach BoJ’s target until end-2024 While inflation excluding fresh food in Tokyo wasn’t far above the Bank of Japan’s 2% target in November, we think it will take …

4th December 2023

All-property values are down by 12.5% since mid-2022, but we expect an eventual decline of above 20%. Much of the correction at the all-property level is driven by our forecast for cap rates to go above 5% for all-property. For offices, additional drivers …

Although we expect US equity office REITs to benefit further from falling long-dated Treasury yields, we continue to think that their long-run prospects are blighted by a structural reduction in demand. Real estate was the best-performing sector of the …

With the budget deficit rebounding over the last year and Congress characterised by partisan dysfunction, the odds of a full-blown fiscal crisis developing over the next decade are rising. The US faced a similarly bleak fiscal outlook in the early 1990s …

Overview – Following a strong 2023, GDP growth is set to slow towards potential next year and the labour market will tread water for now. However, with the virtuous cycle between consumer prices and inflation set to gain momentum, we expect the Bank …

Despite strong growth, core inflation normalising Q3 growth up, Q4 down This week’s modest upward revision to third-quarter GDP growth, which is now estimated to have been as strong as 5.2% annualised, rather than 4.9%, was certainly eye-catching. It …

1st December 2023

The revisions to the national accounts leave the post-pandemic recovery looking stronger than we thought. But that is partly due to intense inventory building, which leaves the economy vulnerable to a period of destocking now that demand is weakening. …

The manufacturing PMI surveys have overstated the weakness in industrial production over the past couple years. But, even taking this into account, November’s PMIs suggest that while global industry might be past the worst, it looks set to end 2023 and …

This page had been updated with additional analysis since the first publication. Manufacturing activity continues to struggle The unchanged reading of 46.7 for the ISM manufacturing index in November suggests that manufacturing activity continued to …