Filtered by Region: G10 Use setting G10

Chancellor a bit more generous, but may fall short on long-term growth Today’s Budget has taken a bit of a backseat given the renewed worries about the global banking system, but the Chancellor was a bit more generous than we expected and we suspect he …

15th March 2023

Even as the economy has slowed nominal all-property rental growth has held up relatively well. But that largely reflects the impact of high inflation, which is now falling. In any event, underlying supply and demand conditions are ultimately the more …

This year’s Shunto should result in the strongest negotiated pay hikes in decades. But the average Japanese employee will have little to rejoice in. Weaker corporate profits as well as a likely loosening of labour market conditions on account of a …

Stronger-than-expected economic data in January led to a rebound in market interest rate expectations and a jump in mortgage rates from 6.2% at the start of February to 6.8% in March. That drove mortgage applications for home purchase lower and means …

14th March 2023

Euro-zone industrial production probably edged up in January (10.00 GMT) The UK’s Spring Budget may contain limited short-term fiscal loosening (12.30 GMT) We think that US retail sales fell by 0.8% in February (12.30 GMT) Key Market Themes How the …

Starting with the ECB today, some major central bank decisions are due in the shadow of recent banking sector turmoil. Will policymakers press ahead with their fight to rein in inflation, or will the risk of financial instability inject caution into their …

Strong inflation data counter financial stability concerns The 0.5% m/m rise in core consumer prices last month adds to the evidence that inflation remains stubbornly high, but the ongoing fallout from the SVB crisis over the coming days is still likely …

Strong inflation data unlikely to outweigh financial stability concerns The 0.5% m/m rise in core consumer prices last month adds to the evidence that inflation remains stubbornly high, but the ongoing fallout from the SVB crisis over the coming days is …

Latest figures confirm plummeting demand during Q4 The detailed mortgage lending data for Q4 showed a slump in demand, as rising mortgage rates began to bite. The latest MLAR data confirmed the sharp turnaround in market conditions and suggest that, with …

This checklist helps clients keep track of the key forecasts announced during the Spring Budget at 12.30pm (GMT) on Wednesday 15 th March. Our more detailed preview is here . We will send a Rapid Response shortly after the speech, we are hosting a “Drop …

Wage growth eases despite labour market remaining tight The labour market remained tight in January. Even so, the Bank of England will breathe a sigh of relief as wage growth is easing. Together with the collapse of a couple of US banks having tightened …

Wage growth eases despite labour market remaining tight The labour market remained tight in January. Even so, the Bank of England will breathe a sigh of relief as wage growth is easing. But the fallout from Silicon Valley Bank’s collapse suggests that the …

Australian banks are unlikely to experience the same valuation losses that resulted in the demise of Silicon Valley Bank. The biggest risk is that a freezing up of overseas bond markets shuts down funding avenues for the major banks, but the Reserve Bank …

Even if the collapse of several mid-tier banks doesn’t develop into a full-blown systemic crisis, it will more than likely trigger a credit crunch. That raises the risk that the economy will suffer a harder landing, which would accelerate the needed …

13th March 2023

Clients can find our coverage on the SVB collapse on our designated landing page here … …and sign-up here for our Drop-In on the policy outlook for the ECB (10.00 GMT) We think US consumer price inflation fell only slightly, to 6.1%, in February (12.30 …

Slight uptick in February’s lending, but still below 2022 average Net commercial real estate lending ticked up in February following a slowdown the month prior. That said, monthly lending activity across all sectors remained below the average for 2022. …

Overview – The economy is on the brink of a mild recession but with underlying inflation still accelerating, we expect new Bank of Japan Governor Ueda to end Yield Curve Control at the upcoming meeting in April. Key Forecasts Table Domestic Demand – We …

This dashboard shows our latest national sector-level commercial real estate forecasts for the next five years, as well as summary forecasts for a handful of core macroeconomic variables. If you have subscriber access to the data underlying this …

US authorities intervened on Sunday following the extraordinarily rapid collapse of Silicon Valley Bank last week. Have they done enough to calm markets, what does this mean for the need for further monetary policy tightening and what are the contagion …

Fed, Treasury and FDIC lay out fire break for banking system In the wake of the collapse of Silicon Valley Bank ($215bn in assets) – which has been followed today by the demise of Signature Bank ($110bn) – the Fed, Treasury and FDIC have acted …

12th March 2023

The circumstances of the Silicon Valley Bank (SVB) collapse are unique enough that it probably won’t trigger a widespread financial contagion. Nevertheless, it is a timely reminder that when the Fed is singularly focused on squeezing inflation by jacking …

10th March 2023

We think US consumer price inflation fell slightly to around 6% in February (Tue.) Retail sales in China probably rebounded in January and February (Wed.) We expect the ECB to hike by a further 50bp (Thu.) Key Market Themes US government bond yields …

Failed dockworker union negotiations on the West Coast have led to further diversion of US imports toward the East and Gulf Coasts, supporting warehousing demand in those markets for longer than expected. We expect a degree of this demand to persist into …

Powell in hawkish mood Fed Chair Jerome Powell confirmed this week that interest rates are set to rise higher than we previously anticipated. Powell noted that the strength of the January activity, employment and inflation data indicated that …

Payrolls strong but rest of report suggests 25/50bp Fed hike debate unresolved The above-consensus 311,000 increase in payroll employment last month confirms that the super-sized 504,000 gain in January wasn’t just a seasonal distortion, but the rest of …

Employment strong, but rest of report suggests 25/50bp Fed hike debate still unresolved While the above-consensus 311,000 increase in payroll employment last month confirms that the super-sized 504,000 gain in January wasn’t just a seasonal distortion, …

We have revised up our forecasts for real GDP and no longer think the economy will be quite as weak. This has very little to do with the 0.3% m/m rise in real GDP in January released this morning. Most of that was a rebound after the widespread strikes …

January’s strength won’t prevent contraction in GDP in Q1 The 0.3% m/m rise in real GDP in January (consensus +0.1% m/m, CE +0.4% m/m) will raise hopes that the economy will escape a recession in 2023 and will increase calls for the Chancellor to splash …

Governor Phil Lowe’s proclamation at Wednesday’s AFR business summit that the RBA was closer to a pause in interest-rate increases has fed speculation of a dovish pivot on the part of the Board. Indeed, financial markets have tamped down their …

Lower inflation means Norges Bank can stick to 25bp hikes February’s decline in headline and core inflation takes some of the pressure off the Norges Bank and means that it is likely to hike by 25bp at the meeting in two weeks’ time. After surprising on …

Resurgence in activity unlikely to last The 0.3% m/m rise in real GDP in January (consensus +0.1% m/m, CE +0.4% m/m) leaves the economy in better shape than we had expected just a few months ago. But looking beneath the surface, the figures suggest the …

The Bank of Japan didn’t make any policy changes at Governor Kuroda’s last meeting today but we expect incoming Governor Ueda to abandon Yield Curve Control in April . While that decision was widely anticipated, we were among the few who predicted the …

Case for end of YCC a touch weaker but still strong Contrary to our expectations, the Bank of Japan did not make any changes to Yield Curve Control (YCC) at today’s meeting. And the case for abandoning the policy now looks a little less compelling than a …

BoJ still likely to end Yield Curve Control The Bank of Japan didn’t make any policy changes at Governor Kuroda’s last meeting today but we expect incoming Governor Ueda to abandon Yield Curve Control in April. We were among the few who expected the Bank …

The Fed is clearly trying to avoid a premature easing in financial conditions and a repeat of 1970s-style “stop-go” monetary policy. This Update discusses some lessons from that period for equity markets today. Equities have struggled over this week, …

9th March 2023

The US may not have a monarchy, but cash has arguably become its proverbial king of investments. If history is a guide, it is a reign that is likely to feature equities underperforming bonds amid a recession. Last November, the yield of a 3-month Treasury …

We expect industrial completions to exceed 3.5% of inventory this year, despite the first quarterly drop in space under construction in Q4 for over two years. But new starts are already slowing and with higher interest rates, elevated construction costs …

The numerous “plans for growth” that have been announced by the Government, the Opposition, and various commentators in recent months vary in their analytical rigour but all miss one crucial point: many of the reforms required to lift the UK’s pitifully …

Patches of positivity unlikely to last The slight recovery in the new buyer enquiries balance in February suggested that the reversal of the autumn spike in mortgage rates allowed a limited revival in demand. But with sales volumes falling and price …

The JOLTS survey showed a drop back in job openings in January, with the timelier job postings data from Indeed pointing to a more marked deterioration in labour market conditions in February. (See Chart 1.) The private job openings rate has …

8th March 2023

China inflation data likely to show rising price pressures (01.30 GMT) We expect interest rates to be left on hold in Malaysia… (07.00 GMT) …and also expect Peru’s central bank to leave rates unchanged (23.00 GMT) Key Market Themes Most “risky” assets …

With another 50bps rate hike at the European Central Bank’s March meeting looking like a done deal, all eyes will be on how policymakers signal the path ahead for monetary tightening. Will the resilience seen in some of the recent data be reflected in the …

Strong start to 2023 unlikely to be sustained The widening in the international trade deficit to $68.3bn in January, from $67.2bn, included big rebounds in both imports and exports which, at face value, add to the signs that demand is strengthening at …

We expect the Spring Budget on 15 th March to contain some giveaways confined to 2023/24. But a downgrade to the Office for Budget Responsibility’s (OBR) medium-term GDP growth forecasts will prevent an unwinding of the £54bn (1.8% of GDP) of fiscal …

A record amount of industrial space is currently under construction, which looks poorly timed given the upcoming recession. However, the sector is entering the downturn in a strong position with very low vacancy. And we expect the share of online retail …

Industrial rebound, but recession still coming The big rebound in German industrial production in January suggests that industry may continue to hold up well in the face of the energy crisis. However, with the renewed drop in retail sales pointing to …

What will UK Chancellor Jeremy Hunt deliver in his Spring Budget? Will he be able to splash any cash, will he hold back sweeteners until closer to the next general election, or will the OBR’s new economic forecasts tie his hands? Group Chief Economist …

7th March 2023

Powell confirms higher peak in rates Fed Chair Jerome Powell appears to have confirmed today that interest rates are set to rise a higher than we previously anticipated. But with most evidence still pointing to economic weakness and lower inflation this …

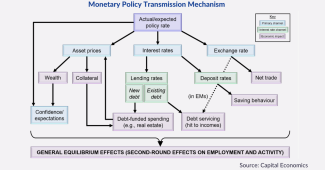

We think that most – perhaps two thirds – of the drag on activity from tighter monetary policy in advanced economies is still to come through in 2023. So, despite some surprisingly resilient data recently, we are sticking to our forecasts for advanced …