Filtered by Subscriptions: UK Economics Use setting UK Economics

President Trump’s latest flurry of tariffs implies that the US effective tariff rate will rise to about 17%, from 2.3% last year. That is a little higher than we assumed and so presents modest downside risks to our forecast for global GDP growth and a …

1st August 2025

We’re discussing the outlook for Bank of England, Fed and ECB policy in a 20-minute online Drop-In at 3pm BST today. (Register here .) And a t our in-person Roundtables in London on Tuesday 1 st July, clients can discuss with our economists and their …

19th June 2025

The overnight strikes by Israel on Iran mark a major escalation in the conflict in the region and, with the oil market tighter than it was a few months ago, the risks to oil prices look more balanced than we’d previously thought (rather than skewed to the …

13th June 2025

The 2025 Spending Review is the tightest (outside of the austerity years in the early 2010s) since 2000 and the tough decisions for Chancellor, Rachel Reeves, won’t end here. The government’s U-turns on benefit and welfare spending and higher borrowing …

11th June 2025

According to the measures of wage growth that we consider the most useful and the fundamentals of the recent easing in the demand for labour relative to the supply, it is only a matter of time before wage growth slows to rates that are more consistent …

4th June 2025

The suggestion that the Chancellor may be considering cutting 50,000 civil service job cuts wouldn’t weigh on employment growth much over the next few years. Only if the government were to cut public sector employment towards its post-austerity and …

2nd June 2025

U-turns on benefit and welfare spending, increased pressure to ramp up defence spending and higher borrowing costs have left the Chancellor, Rachel Reeves, in a sticky position. If she wishes to avoid a political backlash and/or an adverse reaction in the …

29th May 2025

In this Update, we answer several key questions about how the US Court of International Trade (CIT) tariff ruling might affect the US and other economies. The outlook may now rest on the decision of the Republican-stacked Supreme Court. The upside risks …

The recent climbdown has left the effective US tariff rate on the rest of the world at around 15% as opposed to the 27% which was threatened at the height of this year’s trade war. While this is still the highest since the 1930s, it is unlikely to cause a …

13th May 2025

We don’t foresee further common-currency outperformance of MSCI’s UK Index vis-à-vis its USA Index, which has largely been a function of their compositions and the strength of cable since Donald Trump’s return to the White House . This is because we …

Global Trade Stress Monitor …

The US and China have each suspended for 90 days all but 10% of their Liberation Day tariffs and cancelled other retaliatory tariffs. This is a substantial de-escalation. However, the US still has much higher tariffs on China than on other countries and …

12th May 2025

The UK-US trade deal announced by President Trump and Prime Minister Starmer today won’t make a big difference to the UK economy as a whole, although it is more significant for certain sectors such as cars and steel. The upcoming UK-EU reset won’t be a …

8th May 2025

More UK rate cuts coming, but not as quickly as investors expected The Bank of England predictably cut interest rates from 4.50% to 4.25% today and gave the impression that it will continue to cut rates at the current pace of 25 basis points (bps) every …

President Trump’s trade war has created material downside risks for the global economy. Our forecasts assume that tariffs on most countries outside China will stay at 10% and retaliation by other governments will be moderate. In this scenario, global GDP …

10th April 2025

Despite President Trump’s latest decision to pause the US’s “reciprocal” tariff regime for 90 days, there is still a real risk that the second-order effects of higher US tariffs on the UK economy are bigger and that UK inflation and interest rates fall …

We hosted two online Drop-In sessions on 3 rd April to discuss the fallout from President Trump’s Liberation Day tariff announcement. (See a recording here .) This Update contains answers to some of the questions that we received and links to several more …

3rd April 2025

Our scenarios of how different rates of US tariffs on UK exports could influence the UK are designed to provide clients with some real-time context when President Trump announces tariffs tonight. These are rough rules of thumb for blanket tariffs on all …

2nd April 2025

In this Update, we answer several key questions about how the announced 25% tariffs on US imports of autos and parts might affect the global economy and the US itself. Mexico, Slovakia and Korea are most exposed with up to 1.6% of GDP at risk. But the …

27th March 2025

While leaving interest rates at 4.50% today, the Bank of England seemed less committed to continuing to cut rates by 25bps every quarter. We had already been pondering this possibility and today’s news has tipped us towards putting a pause in the rate …

20th March 2025

Our new CE UK Employment Indicator , which extracts the overall signal from a range of measures of employment, suggests that while employment growth has continued to slow in Q1 this year, it is cooling rather than collapsing. This lends support to our …

19th March 2025

The events of the past two weeks have called into question whether the US is severing ties not just with adversaries such as China but also allies, including Canada, Mexico and the European Union. This would radically alter the shape of the fractured …

4th March 2025

It is very unusual for the Bank of England to be cutting interest rates when inflation is above the 2% target and is expected to rise further. There’s a growing risk, then, that inflation fears will force the Bank to stop cutting rates. Equally, though, …

27th February 2025

The Prime Minister’s announcement that defence spending will rise from 2.3% of GDP now to 2.5% by 2027 is likely to be only the start of a more substantial and longer-lasting increase in defence spending that could be funded by cuts to public spending …

25th February 2025

This analysis has been edited to reflect the influence of the Q4 2024 GDP data released two days after the initial analysis was published. Higher taxes for businesses, a lingering drag from the previous interest rate hikes and softer overseas demand …

11th February 2025

While cutting interest rates from 4.75% to 4.50% today, which was the third 25 basis point (bps) cut in seven months, the Bank of England showed some signs that it may cut rates faster and further than our forecast of a decline to 3.50% by early 2026. …

6th February 2025

Our analysis suggests that most of the recent rise in the household saving rate can be attributed to cyclical rather than structural factors, which means the saving rate will slowly fall as interest rates decline. That lends support to our view that …

23rd January 2025

We know that the economy flatlined or suffered a small contraction in Q4. But that would have been much worse if not for what appears to be a rise in government spending, which will play an important role in driving GDP growth throughout 2025 too. With …

20th January 2025

Our base case is that a stabilisation and eventual fall back in gilt yields will allow the government to muddle through and wait until the next fiscal event on 26 th March before making any decisions on taxes and spending. However, a significant worsening …

14th January 2025

With long-dated gilt yields hitting multi-decade highs, we held an online Drop-In session on Wednesday to discuss the outlook for the gilt market and the implications for government policy and the UK macro and housing market outlook. (See a recording here …

9th January 2025

We originally published an Update ahead of the general election on 4 th July on what taxes the next government could raise. In light of the recent rise in gilt yields putting the Chancellor on course to break her fiscal rule, we have refreshed this …

The troubling start to 2025 is casting doubt over our key non-consensus forecasts for 2025. But we still think other forecasters are underestimating how fast the economy will grow, how far inflation will fall and how many times the Bank of England will …

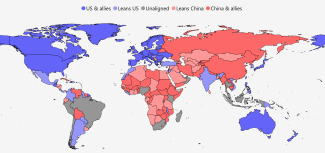

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

There is a significant chance that the Office for Budget Responsibility (OBR) will judge that the Chancellor, Rachel Reeves, is on course to miss her main fiscal rule when it revises its forecasts on 26 th March. To maintain fiscal credibility, this may …

While the Bank of England left interest rates at 4.75% today, it struck a slightly more dovish tone. This supports our view that the next 25 basis points (bps) rate cut will come in February and that the Bank will cut rates further and faster than …

19th December 2024

With pressures on public spending continuing to grow, this has raised the chances that the Chancellor, Rachel Reeves, raises spending further in her 2025 Spending Review. If she raises spending and funds it with higher taxes, that would probably add to …

11th December 2024

Our new Bank of England Caseometer helps track whether the Bank is becoming more inclined to cut interest rates faster and further or slower and not as far. Our forecast is that rates will continue to be cut gradually, but that they will fall to 3.50% in …

10th December 2024

We held an online session on US import tariffs on 26th November. (See a recording here ). In this Update we answer the questions we were most asked. What are Trump’s motives for threatening tariffs and will he follow through? Trump has spoken about using …

29th November 2024

The Chancellor, Rachel Reeves, has confidently claimed that she will not be “coming back with more taxes”, but developments since the Budget have already whittled away her fiscal ‘headroom’. Further tax hikes are not inevitable, but they are more likely …

28th November 2024

President-elect Donald Trump’s first threatened tariffs since the election are designed to extract concessions on drug trafficking and illegal border crossings, which means it may be possible for the countries targeted – Canada, Mexico and China – to head …

26th November 2024

The UK is not as exposed to US import tariffs as many other economies and we suspect any resulting reduction in UK GDP would be very small. That said, the car and pharmaceutical sectors are the most vulnerable areas of the UK economy. And we don’t think …

14th November 2024

Watch a recording of our post-MPC online briefing here . While cutting interest rates from 5.00% to 4.75% today, the Bank of England implied that the Budget means rates will continue to fall only gradually. We agree and due to the Budget (and not the US …

7th November 2024

While the market fallout from yesterday’s UK budget announcement is still a very long way from the 2022 “mini-budget” debacle, the surge in Gilt yields and fall in sterling over the past couple of days has some similarities to that episode. A meltdown of …

31st October 2024

The Bank of England’s Q3 Credit Conditions Survey suggests house prices will rise further in Q4 and supports our view that a mild slowdown in GDP growth this year is more likely than another recession. Despite the fall in the average quoted mortgage …

10th October 2024

One way the US election could influence the UK economy would be if Donald Trump won and delivered on his pledge to put a 10% tariff on UK exports being sent to the US. We suspect the impact on UK activity from such a policy would be small (and perhaps …

2nd October 2024

We held an online Drop-In session last week to discuss the likely pace and extent of interest rate cuts and their implications now that the US Fed has joined the party. (See a recording here .) This Update answers some of the questions that we received, …

23rd September 2024

We’ll be discussing the differences in the policy outlook for the Bank, the ECB and the Fed in a 20-minute online briefing at 3pm BST today. (Register here .) By leaving interest rates at 5.00% the Bank of England showed it is more like the ECB than the …

19th September 2024

We don’t think the slew of inflation-busting public sector pay deals that have been agreed by the new government will prevent wage growth from slowing next year to the rates of 3.0-3.5% we think are consistent with the 2.0% inflation target. But the big …

21st August 2024

The news that the economy may now be 2.6% bigger than its Q4 2019 pre-pandemic size, rather than 1.8%, suggests it is in better shape than we previously thought. But with the UK still suffering from balefully low productivity and labour force growth, …

7th August 2024

Although the UK has clearly been caught up in the recent turmoil in global financial markets, we do not think a double-dip recession is on the cards. Nonetheless, the disorderly market reaction, if sustained, raises the downside risks to our GDP forecast …

6th August 2024