Filtered by Subscriptions: The Long Run Use setting The Long Run

While the consensus has become more optimistic about the near-term recovery, most analysts – and the majority of central banks – still believe that the pandemic will leave a legacy of lower global output over the long term. We disagree. And if we’re …

21st May 2021

There is typically more scope for female participation rates to rise and boost labour supply in EMs. This is particularly so in India and is one reason why we expect its economy to outperform in the long run. Increasing female labour force participation …

19th May 2021

The downward trend in average working hours in advanced economies has slowed or stalled in the past few decades. Yet there are reasons to think that the decline will resume, at least in some sectors and some countries. Other things equal, fewer hours …

13th May 2021

The 2020 US and China censuses add to the reasons why we think China will struggle to overtake the US as the world’s largest economy. China’s birth rate has continued to fall and the population will peak earlier than previously thought, so demographics …

11th May 2021

Download the pdf for the full report . Following their sharp rises earlier on in the year, government bond yields have steadied over the past few weeks. Perhaps reflecting this, both global equities and developed market (DM) REITs have generally rallied …

23rd April 2021

There is evidence that the pandemic has accelerated technology use, partly through increased equipment investment but mainly through a change in the way that people work. The effects on productivity might not be immediate or huge, but they will be …

16th April 2021

The rapid growth of the global labour supply in the past few decades looks set to give way to a period of much weaker growth. Some argue that this will reverse the decline in inflation seen in recent years as the bargaining power of labour rises and an …

24th March 2021

While the stock market fared much better than the economy in the US overall during the past ten years, we do not expect that to remain the case. A country’s stock market and its economy will grow at the same rate if there are no changes in the ratios of …

17th March 2021

We argued some time ago that globalisation had peaked and a period of deglobalisation might even lie ahead. It is now becoming clearer what to expect – namely a type of regionalism driven by the emergence of separate US-led and China-led spheres. While …

16th March 2021

One silver lining of the pandemic may be to accelerate the transformation to a “green” global economy. The related investment could boost demand, and possibly potential growth, in those countries introducing green stimulus measures. But it seems unlikely …

10th March 2021

In this first edition of the Long Run Returns Monitor we present an updated version of the projected returns from the major asset classes which feature in our annual Long Run Asset Allocation Outlook. The full report can be accessed by clicking on the …

5th March 2021

In light of our latest long-term economic and financial market forecasts, we have revisited our views for commercial property performance over the next three decades. We think that average returns will be lower than in the recent past, but that property …

1st March 2021

The equilibrium level of real interest rates in the global economy may not remain quite as low as of late, but we expect any rise to be gradual and small. With policymakers at the same time taking a more tolerant attitude towards inflation, actual real …

24th February 2021

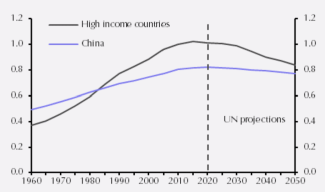

Our long-run forecasts suggest that China will still be the second largest economy, measured at market exchange rates, in 2050. The most likely scenario is that slowing productivity growth and a shrinking workforce prevent China ever passing the US. But …

19th February 2021

The Long Run is a new subscription service offering insight into issues that will shape the global economy and financial markets over the next 30 years. This Update outlines our ten key calls for the coming decades. 1. Pandemic won’t permanently weaken …

17th February 2021

We anticipate that US equities will outperform long-dated Treasuries over the next ten years, even though the valuation of the stock market is even higher now than it was at the beginning of the 1930s and approaching its level at the outset of the 2000s – …

16th February 2021

We do not expect the pandemic to do permanent damage to global economic growth as vaccines allow activity to resume. There will be sustained behavioural changes, but these need not be negative. Note, for example, that technology use has accelerated in …

12th February 2021

In our Future of Property research, we identified important post-pandemic shifts in most real estate sectors. How these trends interact will be key to the outlook for the urban locations where most real estate is clustered. We think it is premature to …

4th February 2021

The pandemic – and the associated increase in working from home – may cause a fundamental shift in the way that cities function in future. But this shift will not necessarily trigger a more fundamental economic decline in the world’s largest urban …

5th January 2021

Korea’s population last year shrank for the first time in its history, underlining the seriousness of the demographic “time bomb” facing the country. The poor demographic outlook is the key reason why we expect trend growth in Korea to slow sharply over …

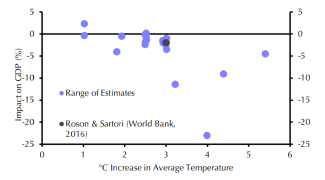

Climate change will be more costly to EMs than developed countries, with parts of Africa, as well as South and South East Asia most vulnerable to rising global temperatures. That said, some EMs could benefit as investments to mitigate climate change …

19th November 2020

The COVID pandemic will leave a profound economic legacy. But unlike previous crises, this will not necessarily manifest itself in much weaker rates of long-term economic growth. Instead, the economic legacy of the pandemic will be felt in changes to …

17th November 2020

The pandemic has increased the odds that the US will eventually experience a period of high inflation, principally because we expect the Fed to be less committed to ensuring price stability in the future. The higher public debt burden, slower global …

16th November 2020

Financial repression – defined in the current context as measures that artificially lower the cost of government borrowing – will become an increasingly used tool to cope with higher public sector debt burdens post COVID-19. After all, it is more …

10th November 2020

We forecast that the returns from equities will beat those from government bonds in the world after COVID-19. However, we expect the outperformance of large-cap equities in the US to end. We have written extensively on our macroeconomic services about the …

20th October 2020

The state has taken on a much greater role in G7 countries during the pandemic and there is no guarantee that it will relinquish all its new powers when the coronavirus threat fades. The pandemic could accelerate the backlash against capitalism that had …

13th October 2020

In this Focus , we argue that the medium-term impact of the COVID-19 pandemic on both global economic growth and consumer behaviour has brought forward “peak oil demand” to around 2030 . As a result, we expect that real oil prices will be falling for much …

8th October 2020

With the US election result likely to have limited near-term implications for world GDP, the main issue for the global economy is how it affects US trade policy. Joe Biden would take a less aggressive approach, but he would not prevent a further …

5th October 2020

The immediate costs of the COVID crisis will be shouldered more by governments than the private sector. However, as fiscal support recedes in the coming years, a greater share of the costs will be borne by households and firms, and ultimately by their …

30th September 2020

Global supply chains have functioned well this year despite the disruption of social distancing and lockdowns, and people in many places appear more appreciative of migrants. But the pandemic is widening the rift between China and the rest of the world. …

22nd September 2020

Although low inflation is likely to be the story over the next couple of years, the huge amount of policy stimulus could push up inflation further ahead. Central banks, in theory, have the tools to nip any rise in the bud. So the bigger risk is if there …

10th September 2020

Chair Jerome Powell announced this morning that the Fed will be adopting what he described as a “flexible form of average inflation targeting”, which we expect will trigger additional policy stimulus in the form of stronger forward guidance and possibly …

27th August 2020

It is by no means inevitable that the coronavirus crisis puts a big permanent hole in the supply capacity of economies (i.e. their ability to produce goods and services). With the right government policies, many economies should be able more or less to …

29th June 2020

As long as social distancing isn’t practised for many years, then those behavioural changes triggered specifically by the coronavirus crisis will probably prove temporary. But those changes that were already underway and which have been supercharged by …

23rd June 2020

This Update draws together the conclusions from the various pieces of research that we have published in recent weeks on how the fiscal costs of the crisis will be dealt with. In short, we are generally sanguine about the rise in government debt, which we …

10th June 2020

Prime Minister Modi’s BJP has expedited structural reforms that normally face stiff political resistance, ostensibly as part of efforts to support recovery from the coronavirus crisis. These moves will do little to boost demand in the near term. But if …

2nd June 2020

The immediate effects of the coronavirus on the global economy are becoming increasingly clear and point to a sharp fall in output across the world. Recession looms. The effects over the longer term are less obvious. The most likely outcome is that …

19th March 2020

The coronavirus itself may not trigger a wholesale reorganisation of supply chains, but it strengthens the argument for companies to reduce associated risks. One response might be to introduce more redundancy into supply chains to lessen reliance on …

2nd March 2020

We side with the optimists regarding the chances of another major technological step forward, although we can only guess at the timing. We expect the US to remain at the forefront of these advances for now, but it will not lead in all areas of new …

13th February 2020

We expect most of the 2020s to be characterised by slow growth and very low inflation as persistently weak productivity growth leaves the developed world looking distinctly Japanese. But technological developments should ultimately bear fruit and we …

10th January 2020

One of the biggest disappointments of this decade has been the stubborn weakness of global productivity growth. While we do not think that this is a permanent shift, a turn-around does not look imminent. And any improvement depends in part on countries …

13th December 2019

We do not believe that there has to be a trade-off between preventing global warming and achieving economic growth. Even so, there is a clear risk that the world fails to prevent a significant further rise in global temperatures. Although it is only in …

3rd December 2019

The surge in the participation rate that has boosted employment by nearly a tenth since 2012 and thereby underpinned stronger economic growth is running out of steam. This will have a big impact, shaving close to a percentage point off Japan’s sustainable …

22nd July 2019

We think that world GDP growth will average around 3.0% over the next twenty years, compared to around 3.5% over the past two decades. Productivity growth is likely to rebound in advanced economies, led by the US, but this will be offset by a steady …

6th December 2018

Slowing population growth and population ageing will weigh heavily on economic growth in the coming decade or two, particularly in Europe and Asia. These forces will be only partly offset by increased participation in the workforce by women and older …

24th May 2018