Fed Chair Jerome Powell is resolute in his belief that the burst of stronger inflation we are about to see will prove temporary, with underlying inflation dropping back to the 2% target next year. We are not convinced. Given the breadth of the upward …

6th May 2021

The closure of the border will reduce Australia’s potential output by around 2.5%. But this will be partly offset by higher productivity growth due to increased usage of technology and more employees working from home. And the usual red flags that have …

Stimulus cheques and a lack of opportunity to spend money pushed the saving rate to a record high last year. Some of that saving made its way into down payments, with the average first-time buyer putting down an extra 30% in November compared to a year …

4th May 2021

Policy stimulus and tolerance of inflation by central banks may lead to higher inflation in some G7 countries in the coming years. Given the parallels with the run-up to the high-inflation era of the 1970s, it is natural to be worried about history …

29th April 2021

The surge in house prices and very high transaction volumes have led to concerns that the housing market is entering a bubble. After all, the house-price-to-earnings ratio has risen to a fresh all-time high. But because interest rates have continued to …

22nd April 2021

Israel has been the world leader in the vaccination race and the early evidence is that the rapid re-opening of the economy has driven a strong rebound in activity, particularly in services sectors. In this Focus , we launch our coverage of Israel and …

There is evidence that the pandemic has accelerated technology use, partly through increased equipment investment but mainly through a change in the way that people work. The effects on productivity might not be immediate or huge, but they will be …

16th April 2021

Ongoing disruption to global auto production has highlighted the extent to which semiconductors have become an essential input in products that aren’t traditionally considered electronics and also how dependent the world is on Taiwan to produce them. This …

13th April 2021

A rise in US Treasury yields and tightening of external financial conditions could cause vulnerabilities in Turkey and a handful of smaller frontier markets to crystallise. However, most major EMs’ dependence on capital inflows looks limited. Instead, in …

12th April 2021

We suspect that Argentina’s government and the IMF will thrash out a new deal, the 22 nd in their history, but we doubt that this will lead to the sustained turnaround in policymaking that is needed to put public debt onto a sustainable path. The upshot …

7th April 2021

In a world where the Phillips curve is flat, inflation expectations become the key driver of actual inflation over the medium term. But getting a true handle on inflation expectations is difficult because of the large number of diverse measures that are …

31st March 2021

The economic recovery from the COVID-19 crisis may not push CPI inflation above 2.0% for a prolonged period until 2023, although there is a risk that it happens sooner. And further ahead, the government’s desire to use fiscal policy to achieve its …

22nd March 2021

The Brazilian central bank’s 75bp hike in the Selic rate (to 2.75%) and hawkish statement point to a front-loaded tightening cycle in the coming months. We now expect a further 200bp of hikes (to 4.75%) over the next three meetings. But we think the cycle …

18th March 2021

Tunisia’s public finances have deteriorated further during the COVID-19 crisis and, with the government unlikely to be able to push through much-needed fiscal austerity, a debt restructuring looks increasingly likely in the coming years. Tunisia has been …

History shows that supercycles are usually demand-driven, and that the performance of individual commodity prices has varied hugely both within and between past supercycles. In addition, supercycles can temporarily give way to shorter-run boom/bust …

17th March 2021

China’s new policy blueprint seeks above all to promote a large and hi-tech manufacturing sector, both as a defence against decoupling by the West and as a source of productivity gains. Policymakers are pinning their hopes on rapid domestic innovation to …

15th March 2021

Given that the natural vacancy rate (NVR) provides a better gauge of office market conditions than the absolute vacancy rate, we set out to estimate the NVR across European office markets. Future market conditions implied by our NVR estimates are broadly …

11th March 2021

The upcoming state elections in India will have an important bearing on economic policy at the local level. But perhaps more significant, the outcome of the state elections could be important in determining whether Prime Minister Modi’s BJP will be able …

10th March 2021

While most governments are focussed squarely on maintaining or increasing fiscal support for their economies, in today’s Budget the Chancellor, Rishi Sunak, adopted a different two-staged plan for the UK – spend big for the next two years and tax big for …

3rd March 2021

While policymakers in the US are wrangling about how much additional stimulus is required, the debate in the UK is more about what tax rises are needed to repair the damage to the public finances caused by the pandemic. Admittedly, in next week’s Budget …

25th February 2021

The equilibrium level of real interest rates in the global economy may not remain quite as low as of late, but we expect any rise to be gradual and small. With policymakers at the same time taking a more tolerant attitude towards inflation, actual real …

24th February 2021

Much of the recent discussion on whether the proposed $1.9trn fiscal stimulus, equivalent to nearly 9% of GDP, could be too big when the output gap is closer to 3%, has glossed over the fact that the remaining shortfall in output is concentrated in the …

23rd February 2021

Europe’s natural gas pipeline network is already extensive, and we think that it is going to get bigger in the coming decades. Existing pipelines in Turkey are set to be expanded and new pipelines from Africa and the East Mediterranean Sea will probably …

22nd February 2021

Even though the unemployment rate is still as high as it was during the mining bust, job vacancies and the share of firms reporting staff shortages have surged. We suspect that this has been driven by a broad-based drop in labour mobility during the …

The pandemic hasn’t had a major disinflationary effect in Central Europe and the region is in what we think will turn out to be a prolonged period of above-target inflation. But how this affects monetary policy will differ across the region. Interest …

18th February 2021

One legacy of the pandemic is a huge expansion in central banks’ balance sheets. Fears that this will automatically boost inflation are overdone. So, too, are worries that central banks will provoke a destabilising rise in bond yields by selling their …

17th February 2021

The COVID-19 crisis has led to something of a paradox: Italy’s public debt ratio has risen, but the probability of default has fallen. That’s largely because BTP yields are likely to stay far lower than seemed plausible before the pandemic, meaning that …

11th February 2021

We suspect that President Joe Biden’s plan to more than double the minimum wage within four years would have only a minimal impact on GDP. While there would almost certainly be some job losses as a result, we expect most of the adjustment would come via …

10th February 2021

Spain’s economy had been set for a bright 2021 as the vaccine offered hope of a bumper summer tourism season. But the poor start to the rollout means that is now looking less likely. Moreover, the pandemic has exposed structural weaknesses that we think …

Our view that the recovery from the COVID-19 pandemic will be quicker and more complete than most forecasters expect suggests that the economic legacy of the crisis may not be a permanently smaller economy but instead higher inflation and bigger public …

8th February 2021

The period covered by the new Five-Year Plan offers Vietnam an opportunity to establish itself as a major export manufacturing hub. Policy priorities will be to improve the business environment so as to nurture the private sector and to attract more …

1st February 2021

We now expect the RBNZ to tighten monetary policy in the years ahead as GDP growth, the labour market and inflation will be much stronger than the Bank has anticipated. We expect asset purchases to be wound down from this year before the Bank hikes rates …

26th January 2021

The Finance Ministry faces a tough balancing act in the Union Budget for FY21/22 as it aims to stabilise the public finances while avoiding economically and politically-damaging spending cuts. The most likely outcome is that it will set ambitious revenue …

25th January 2021

We think that the Mexican central bank’s (Banxico’s) reaction function will gradually tilt towards tolerating higher inflation. As a result, we think that interest rates in Mexico will stay low for several years, perhaps until 2024, while most analysts …

14th January 2021

The relative resilience of real global merchandise trade during the pandemic has reflected several factors, most importantly robust goods spending in advanced economies. Merchandise trade flows are likely to flatten off next year as the removal of …

23rd December 2020

We estimate that the exports of goods and services that are already facing restrictions by China contribute around 1.8% to Australia’s GDP. While we still expect iron ore and liquefied natural gas exports to remain spared, that figure could rise to around …

Ten years on from the “Arab Spring” uprisings that afflicted large swathes of the Middle East and North Africa, hopes for a shift to democracy that would unleash reforms and transform the region’s economic prospects have failed to materialise. Even once …

17th December 2020

Our forecasts for GDP growth across emerging Asia in 2021 are much higher than consensus expectations across the board. Even so, in many places, output will still be below the pre-crisis level until the end of the year and it will remain well below its …

16th December 2020

The distribution of an effective COVID-19 vaccine in India will brighten the economic outlook next year, but India’s recovery will still be one of the weakest among major economies. One consequence is that government bond yields will remain exceptionally …

Due to lower spending and the generosity of government transfers, households are set to save $200bn more in 2020 than in 2019. With that rise equivalent to 14% of consumption, there are upside risks to our already above-consensus GDP growth forecasts if …

15th December 2020

President-elect Joe Biden stood for election on a far-reaching environmental plan which, although it will be harder to implement with the Republicans likely to control the Senate, still represents a dramatic U-turn from President Donald Trump’s term in …

9th December 2020

At some point, there may need to be a fiscal squeeze to pay for any lasting increase in spending caused by the COVID-19 crisis and increases in age-related spending. But the biggest danger is that fiscal policy is tightened too much too soon to fill a …

8th December 2020

We think that the spreads of “peripheral” government bonds in the euro-zone are likely to fall next year to levels not seen since before the region’s sovereign debt crisis and that they will stay low over the next decade. This reflects our view of the …

4th December 2020

This Focus sets out a framework for thinking about how the distribution of COVID-19 vaccines will affect the outlook for EMs. For much of Emerging Europe and Chile, these developments may allow economies to return to normal more quickly than we had …

30th November 2020

Despite renewed concern from policymakers in Thailand over the appreciation of the Thai baht, we find little evidence that the rising currency is having a negative effect on the economy, and we don’t think it will be a major drag on the recovery. At its …

The negative economic impacts of COVID-19 have bypassed the housing market so far due to the extraordinary support measures put in place by the government, regulators, and banks. But while policy has probably reduced and delayed the impact of COVID-19 on …

27th November 2020

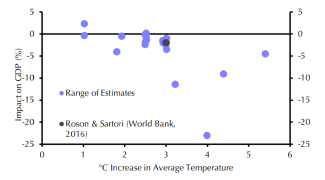

Climate change will be more costly to EMs than developed countries, with parts of Africa, as well as South and South East Asia most vulnerable to rising global temperatures. That said, some EMs could benefit as investments to mitigate climate change …

19th November 2020