Table of Key Forecasts Overview – The EM recovery is now entering a more difficult phase as the boost from economic re-opening fades, supply shortages bite, growth in China weakens and the terms of trade worsen for major commodity producers. Lower vaccine …

28th October 2021

While long-dated government bond yields have risen quite a bit in recent months, we suspect that continued inflationary pressure and the prospect of tighter monetary policy means they still have some way to climb. We expect yields to rise by the most in …

27th October 2021

Overview – Extremely low vaccine coverage continues to cast a dark cloud over recovery prospects in Sub-Saharan Africa and this will be compounded by deteriorations in the terms of trade and tighter fiscal policy. As a result, rebounds in most economies …

Table of Key Forecasts Global Overview – The global recovery will slow in the coming quarters as the initial post-lockdown rebound fades and policy support is reduced. At the same time, supply shortages are likely to persist well into next year, which …

26th October 2021

Overview - The economy slowed sharply in Q3. Weakness in services is already reversing as virus controls have been relaxed again. But industry and construction are on the cusp of a deeper downturn that could pull down China’s growth to just 3% next year. …

Overview – We now expect GDP growth to be 4.8% in 2021, rather than 5.0%, and 3.5% in 2022, down from 4.0%. Worsening labour shortages imply that spare capacity has been rapidly absorbed and point to a sharp acceleration in wage growth. In that …

20th October 2021

Overview – The region has experienced a rapid recovery, but the re-opening boost has now faded and the region is likely to face stronger headwinds in the near term due to surging COVID-19 cases, rising inflation and supply disruptions. Central European …

Overview – Growth in China will weaken further over the coming year as a downturn deepens in industry and construction. The outlook for the rest of the region is improving. We expect many economies to rebound strongly as governments ease restrictions on …

As highly-open economies, Switzerland and the Nordics are far from immune to the issues of slowing global growth and supply-chain shortages that are currently vexing investors. Sweden is perhaps most exposed; the impressive rebound there looks to have …

Overview – Supply chain problems will slow the recovery and keep inflation above target until around the middle of next year. Beyond that, however, the economy should get back on track. After regaining its pre-crisis level later this year, output is …

19th October 2021

Overview – Easing virus outbreaks and the lifting of restrictions boosted recoveries across Latin America in Q3, but growth looks set to slow sharply over the coming quarters. The re-opening boost will soon fade. Fiscal support is, or will be, unwound …

Overview – Economic recoveries in the Gulf will continue to gather pace over the coming year on the back of successful vaccine rollouts and higher oil output, and our GDP growth forecasts lie above the consensus. Outside the Gulf, though, recoveries are …

Overview – The UK economy is experiencing a taste of stagflation. This won’t be anywhere near as severe or as persistent as in the 1970s. But for the next six months, the worsening product and labour shortages will put the brakes on the economic recovery …

Overview – The whiff of stagflation is getting stronger as shortages worsen, leading to surging prices and weaker real GDP growth. Shortages of goods and intermediate inputs will eventually ease, although not for at least six to 12 months. But the drop in …

18th October 2021

Overview – Domestic demand is set to rebound from recent lockdowns and labour markets should remain tight. Meanwhile, soaring energy and food prices will keep inflation high for a prolonged period. To be sure, the Reserve Bank of Australia won’t respond …

14th October 2021

Overview – Following a rapid rebound from the second virus wave, India’s economy is beginning to lose some steam. And with vaccination coverage still low, downside risks remain significant. Under these circumstances, the RBI is likely to keep policy …

11th October 2021

Overview - With the Delta wave having ebbed and the majority of the population now fully vaccinated, we expect a strong rebound in domestic demand over the coming months. But the inflation concerns that hang over other major developed economies won’t …

7th October 2021

Overview – The apartment market is set for a stellar year. The reopening of cities is bringing vacancy rates down and pushing rents up, and strong investor demand has led to a sharp fall in yields. We expect national total returns of around 19% in 2021. …

1st October 2021

Overview – With absorption of landlord-held office stock set to remain negative for the foreseeable future, we continue to expect vacancy rates to climb and rents to fall in all six major office markets over the next few years. That will be particularly …

27th September 2021

Overview – Our forecast for the economic recovery to maintain its momentum in H2 bodes well for occupier and investment activity. But while we think industrial rental growth will pick up, we still expect office and retail rents to end this year lower. …

24th September 2021

Overview – The economic recovery and strong investor demand are supporting the property market upturn in Scandinavia and Switzerland. However, we expect 2021 to mark the peak for returns in most markets, except for Oslo where the start of the monetary …

23rd September 2021

Overview – While the Delta variant has slowed economic activity in other parts of the world, this has not yet been the case in the euro-zone, and we are cautiously optimistic that the bloc will continue to grow. This will support the property market …

16th September 2021

Although it has fallen back a bit over the past three weeks, the dollar has been on the front foot for much of the summer and we think it will make some further headway over the next few months. In part, the dollar’s strength in the past three months …

10th September 2021

Overview – This quarter there are short-term upgrades to all four major sector forecasts for 2021 on the back of strong investor demand for assets, which is driving up prices. Those upgrades mean that returns in the industrial and apartments sectors will …

Overview – The economic recovery has lost some momentum over the summer, but we expect that this will be a temporary setback and the backdrop will be strong into the medium term. There is growing evidence of a sustained commercial property upturn, albeit …

25th August 2021

The recent downward revision to our GDP growth forecasts and the recent hawkish signs from the Bank of England which prompted us to bring forward our forecast of when monetary policy will be tightened means the economic backdrop is a bit less conducive …

9th August 2021

Overview – Vaccination campaigns across Sub-Saharan Africa will continue to struggle, leaving the region vulnerable to renewed virus outbreaks. This, combined with tight fiscal policy, a slow return of tourists and falls in commodity prices means that …

5th August 2021

Overview – Although the prices of industrial metals have picked up again recently, we still expect them to be falling over the next year or so. Underpinning this view are our forecasts for economic growth to slow in China, a continued rebound in supply …

4th August 2021

Overview – After a blistering rally for much of 2021, we expect the prices of energy commodities to be easing back as we move into 2022. Oil supply, particularly from OPEC+, is set to rebound strongly over the next year, which will be a factor weighing on …

3rd August 2021

Overview – There are already signs that the end of the stamp duty holiday will take some heat out of the housing market, with house price inflation set to cool from 10% to 7% by the end of the year. But as we think that the tax break was just one of …

2nd August 2021

While long-dated government bond yields have plummeted in recent months, we suspect that high inflation and the prospect of tighter monetary policy will see them turn a corner before long. We forecast long-term yields to rise across most major economies, …

30th July 2021

Download the PDF for the Full Report Overview – We think that the widespread rallies in commodity prices from their pandemic-induced lows are now close to, or in some cases already past, their peak. Most notably, we anticipate that Q3 will be as good as …

29th July 2021

Table of Key Forecasts Overview – Low vaccine coverage means that the threat to economic recoveries from the highly-contagious Delta variant is much larger in the emerging world than in developed economies. And EMs will take longer to return to their …

Table of Key Forecasts Global Overview – The initial post-pandemic resurgence is nearing its zenith, but strong policy support and limited private sector net debt should allow most economies to grow at a healthy pace over the next two years. The US and …

28th July 2021

Overview – China’s economy has been defying gravity thanks to elevated global demand but this support may now be fading. Meanwhile, last year’s policy easing has been fully reversed. An abrupt slowdown is not likely to follow, but highly-indebted firms, …

23rd July 2021

As elsewhere in mainland Europe, activity in Switzerland and the Nordic economies rebounded in Q2 as services sectors re-opened and the strength of global trade has buoyed exports. Our GDP forecasts for 2021 are generally above the consensus and output …

22nd July 2021

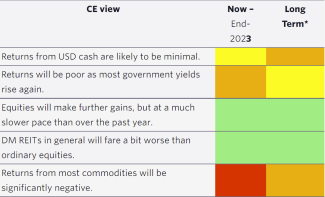

We no longer expect equities and corporate bonds to outperform “safe” government bonds by anything like as much as we did a couple of quarters ago, and we continue to forecast that some other “risky” assets, including most commodities, will struggle over …

21st July 2021

Overview – Strong COVID-19 vaccine rollouts in most of the Gulf and Morocco mean that remaining virus restrictions should be lifted by the end of this year, providing a boost to recoveries that, in the Gulf, will be turbo-charged by the recent OPEC+ deal …

Overview – Rapid recoveries are underway across the region and GDP should return close to its pre-pandemic path sooner than in most other EM regions. While the spread of highly transmissible virus strains poses the greatest threat to the near-term …

Overview – Surging infections across South East Asia and the slow progress of vaccine rollouts mean that COVID-19 will continue to cause widespread economic disruption across large parts of the region until at least the end of the year. We have cut our …

20th July 2021

Overview – Our forecast that COVID-19 won’t significantly reduce potential supply means that the economy can run a bit hotter for longer without generating the persistent rise in inflation that would require monetary policy to be tightened. Admittedly, …

Overview – Virus outbreaks are easing in much of Latin America which should support activity in the near term. And while vaccination coverage is still weak in most of the region, suggesting there is still a clear risk of further virus waves, economies are …

19th July 2021

Overview – The euro-zone is on the way to an almost full recovery. We expect Germany to regain its pre-pandemic level of activity later this year and the tourist-dependent southern countries to do so next year. The Delta variant may lead to some voluntary …

16th July 2021

Overview – Even as mortgage rates have remained low, housing market activity has dropped back as booming house prices, tight credit conditions and a lack of inventory have put off buyers. We expect that dynamic to continue over the remainder of the year. …

15th July 2021

Overview – The lifting of restrictions and ongoing policy support should translate into a sustained period of above-potential GDP growth, driven by consumption and business investment. We expect GDP growth of 6.3% in 2021 and 4.0% in 2022, followed by a …

Overview - Sydney’s lockdown will keep a lid on Australia’s recovery for now, but booming housing markets should support consumer spending and dwellings investment in both countries. We don’t expect labour shortages to ease much when the border opens, so …

Overview – Supply shortages will ease only gradually over the next couple of years, putting sustained upward pressure on core inflation and constraining real activity. We expect core inflation to remain above 3% for the remainder of this year, with only a …

13th July 2021

Overview - Japan’s lagging vaccine rollout has finally reached cruising speed, which should allow a rapid recovery in activity over the second half of the year. The labour market may soon be as tight as it was before the pandemic, but we expect this …

7th July 2021

Overview – India’s ferocious second virus wave is subsiding as quickly as it emerged, enabling the recovery to get back on track. However, the rapid scaling back of containment measures that is underway increases the threat of further outbreaks. And …

1st July 2021

Overview – With cities reopening apartment demand will see a substantial rise this year, boosted by the arrival of households who delayed a move last year. Vacancy rates will fall back in all six major cities covered in this Outlook with those hit hardest …

29th June 2021