Filtered by Subscriptions: UK Economics Use setting UK Economics

While the 0.1% q/q rise in GDP in Q4 of last year was stronger than we and most other forecasters expected, the combination of higher taxes for businesses announced in last October’s Budget, a lingering drag from the previous interest rate hikes and …

5th March 2025

The events of the past two weeks have called into question whether the US is severing ties not just with adversaries such as China but also allies, including Canada, Mexico and the European Union. This would radically alter the shape of the fractured …

4th March 2025

This page has been updated with additional analysis since first publication. Households still in the mood to save rather than spend The stagnating economy is partly because households appear to be continuing to save rather than spend, which is unlikely to …

3rd March 2025

Things change quickly with Trump as President. Only two weeks ago, the title of our UK Economics Weekly was “Trump’s tariffs tirade becomes more troubling for the UK” as it looked as though the UK’s goods exports to the US would be hit with a 25% …

28th February 2025

It is very unusual for the Bank of England to be cutting interest rates when inflation is above the 2% target and is expected to rise further. There’s a growing risk, then, that inflation fears will force the Bank to stop cutting rates. Equally, though, …

27th February 2025

A combination of weaker UK growth, higher yields and more defence spending make for a difficult Spring Fiscal Forecast for Rachel Reeves. In this special preview, our economists highlighted what to watch for in the Chancellor’s upcoming statement to …

26th February 2025

Our senior economists hosted this special online briefing shortly after Rachel Reeves delivered her Spring Forecast, to answer client questions about the macro and market implications, including: The big takeaways on tax, spending and investment; What …

The Prime Minister’s announcement that defence spending will rise from 2.3% of GDP now to 2.5% by 2027 is likely to be only the start of a more substantial and longer-lasting increase in defence spending that could be funded by cuts to public spending …

25th February 2025

The strength of the recovery in housing activity and prices in the second half of last year caught many off guard. But can the market continue to recover at this pace in the face of higher stamp duty and a weaker economy? Members from our UK Housing, …

The news on inflation this week was worrying, raising the risk that CPI inflation will remain higher for longer and interest rates will be cut more slowly than we expect and/or not as far. (See here .) Data released this week revealed that wage growth was …

21st February 2025

This page has been updated with additional analysis since first publication. PMIs point to businesses cutting employment to cope with higher taxes. The composite activity PMI was unchanged in February, which is consistent with the economy moving sideways …

This page has been updated with additional analysis since first publication. Bad news continues for the Chancellor While January’s disappointing public finances figures may not be as bad as they first appear, they continue the run of bad news for the …

This page has been updated with additional analysis since first publication. Supermarkets win, restaurants lose The leap in retail sales volumes in January shows that the retail sector shot out of the blocks at the start of the year. But some of that …

This page has been updated with additional analysis since first publication. Climb in inflation to 3% will be uncomfortable for the BoE CPI inflation took another step up from 2.5% in December to 3.0% in January (consensus, BoE, CE 2.8%) and will probably …

19th February 2025

The decision by the US and Russia to “lay the groundwork” to end the war in Ukraine marks a potentially significant turning point after three years of conflict. Negotiations will take time and the macroeconomic implications will depend on the features of …

18th February 2025

This page has been updated with additional analysis since first publication. Weak employment, but wage growth still too high for BoE’s liking While there was a small improvement in labour market activity in December and January, employment growth remains …

The potential tariffs that UK exporters could soon face for sending goods to the US became bigger this week. On Monday, Trump said that US imports of steel and aluminium from all countries would face tariffs of 25% from 12 th March. Then on Thursday he …

14th February 2025

This page has been updated with additional analysis since first publication. Higher taxes and weaker global demand hold the economy back The 0.1% q/q rise in real GDP in Q4 (consensus, CE and BoE forecasts all -0.1%) leaves the economy all-but stagnating …

13th February 2025

This analysis has been edited to reflect the influence of the Q4 2024 GDP data released two days after the initial analysis was published. Higher taxes for businesses, a lingering drag from the previous interest rate hikes and softer overseas demand …

11th February 2025

The overall message from the Bank of England this week was decidedly dovish, raising the risk that interest rates will be cut further and faster than our forecast of a fall from 4.50% to 3.50% by early 2026. But as we unpacked in our reaction to the …

7th February 2025

While cutting interest rates from 4.75% to 4.50% today, which was the third 25 basis point (bps) cut in seven months, the Bank of England showed some signs that it may cut rates faster and further than our forecast of a decline to 3.50% by early 2026. …

6th February 2025

For updated and more detail analysis see here . Dovish development adds downside risk to our forecast for Bank Rate to fall to 3.50% While cutting interest rates from 4.75% to 4.50% today, which was the third 25bps cut in seven months, the Bank of …

Despite the recent weak news on activity and the uncertainty around the global outlook due to Trump’s US import tariffs, the stronger news on domestic price pressures means the Bank of England will probably continue to cut interest rates only gradually. …

5th February 2025

The Chancellor’s plans to “kickstart economic growth”, which she set out in a speech this week, probably won’t lift the economy out of its recent malaise in the coming quarters. But at the margin, the announcement of some policies and initiatives aimed at …

31st January 2025

Bank to cut interest rates by 25bps at February’s meeting, from 4.75% to 4.50% The tail risks of both faster disinflation and slower disinflation have increased Rate cuts to stay gradual, but rates to fall to 3.50% in 2026 versus market pricing of 4.00% …

30th January 2025

This page has been updated with additional analysis since first publication. Downbeat outlook isn’t heavily weighing on households’ financial decisions December’s money and lending figures suggest the downbeat economic outlook isn’t weighing on households …

In the first glimpse into how the economy has started the new year, this week’s data took another turn for the worse. First, according to the CBI Industrial Trends Survey (ITS) of the manufacturing sector, in Q1, the optimism, expected activity and …

24th January 2025

This page has been updated with additional analysis since first publication. Stagflation concerns remain at the start of 2025 Despite the small rise in the composite activity PMI from 50.4 in December last year to 50.9 in January, at face value it is …

Our analysis suggests that most of the recent rise in the household saving rate can be attributed to cyclical rather than structural factors, which means the saving rate will slowly fall as interest rates decline. That lends support to our view that …

23rd January 2025

This page has been updated with additional analysis since first publication. Figures not as bad as they appear but challenges remain Against a backdrop of slowing GDP growth and high interest rates, December’s overshoot in borrowing is further …

22nd January 2025

This page has been updated with additional analysis since first publication. UK wage growth rebounds further, but there are signs of cooling further ahead While the further rise in regular private sector pay growth in November will cause the Bank of …

21st January 2025

We know that the economy flatlined or suffered a small contraction in Q4. But that would have been much worse if not for what appears to be a rise in government spending, which will play an important role in driving GDP growth throughout 2025 too. With …

20th January 2025

The Chancellor was able to breathe a sigh of relief this week after favourable CPI inflation prints for December in both the UK (see here ) and the US (see here ) led to a reversal in last week’s leap in gilt yields. In fact, the 28 basis points (bps) …

17th January 2025

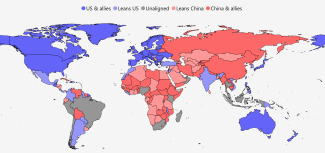

The Shape of the Fractured World in 2025 The share of the fracturing global economy that is accounted for by China and its geopolitical allies contracted in 2024, leaving it under a third the size of the US bloc at the start of 2025. This fall was in part …

This page has been updated with additional analysis since first publication. Disappointing Q4 not a sign of things to come December’s 0.3% m/m fall in retail sales volumes was worse than expected (consensus forecast +0.4% m/m, CE 0.0% m/m) and rounded off …

Economy still at risk of contracting in Q4 While the smaller-than-expected 0.1% m/m rebound in GDP in November (consensus and CE forecast +0.2% m/m) offset the 0.1% m/m decline in activity in October, it’s clear that the economy has a bit less momentum …

16th January 2025

This page has been updated with additional analysis since first publication. Soft surprise boosts February rate cut odds While a lot of the surprisingly large fall in services inflation from 5.0% in November to 4.4% in December (CE forecast 4.8%, BoE …

15th January 2025

Our base case is that a stabilisation and eventual fall back in gilt yields will allow the government to muddle through and wait until the next fiscal event on 26 th March before making any decisions on taxes and spending. However, a significant worsening …

14th January 2025

While the economy lost all momentum at the end of last year, we still expect GDP growth to accelerate from 0.8% in 2024 to an above-consensus 1.3% in 2025. Admittedly, activity could be restrained if the increase in the government’s borrowing costs due to …

13th January 2025

This week’s leap in gilt yields creates more problems for the Chancellor and is an extra headwind for the economy. But it is not a crisis. Admittedly, it is always worrying when UK bond yields rise by more than yields elsewhere and the pound weakens. …

10th January 2025

With long-dated gilt yields hitting multi-decade highs, we held an online Drop-In session on Wednesday to discuss the outlook for the gilt market and the implications for government policy and the UK macro and housing market outlook. (See a recording here …

9th January 2025

We originally published an Update ahead of the general election on 4 th July on what taxes the next government could raise. In light of the recent rise in gilt yields putting the Chancellor on course to break her fiscal rule, we have refreshed this …

The troubling start to 2025 is casting doubt over our key non-consensus forecasts for 2025. But we still think other forecasters are underestimating how fast the economy will grow, how far inflation will fall and how many times the Bank of England will …

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

There is a significant chance that the Office for Budget Responsibility (OBR) will judge that the Chancellor, Rachel Reeves, is on course to miss her main fiscal rule when it revises its forecasts on 26 th March. To maintain fiscal credibility, this may …

This page has been updated with additional analysis since first publication. Downbeat sentiment continues to weigh on households’ financial decisions November’s money and lending data suggests that households’ caution with their borrowing and saving ahead …

3rd January 2025

This page has been updated with additional analysis since first publication. Economy is going nowhere, although households in a decent position The downward revision to Q3 GDP from +0.1% q/q to 0.0% (consensus and CE 0.1%) isn’t quite as bad as it looks …

23rd December 2024

A look back at 2024 reveals that some of our forecasts were good and some were off. We were right to forecast this time last year that Bank Rate would be cut only gradually, from the peak of 5.25% to 4.75%. (See here .) That turned out to be closer than …

20th December 2024

This page has been updated with additional analysis since first publication. Little festive cheer for retailers The 0.2% m/m rebound in retail sales volumes in November was slightly worse than expected (consensus +0.5% m/m) and leaves sales on course to …