Filtered by Subscriptions: Europe Economics Use setting Europe Economics

Today’s policy announcement confirms that Norges Bank is likely to start cutting interest rates at its meeting in March, almost certainly with a 25bp reduction to 4.25%. We think it will then loosen monetary policy a little more quickly than its latest …

23rd January 2025

Norges Bank to start cutting in March Today’s policy announcement confirms that Norges Bank is likely to start cutting interest rates at its meeting in March. We think it will then loosen monetary policy a little more quickly than its latest projections …

Developments over the past year have put France’s public debt on a steeper upward path, with the debt ratio now likely to rise from 113% of GDP last year to around 126% by 2030. We see little chance of a sustained fiscal consolidation in the coming years …

21st January 2025

Oil prices up, but inflation will still fall We now think that headline inflation will be a touch higher this year than we previously expected, but it will still probably average around 2% and the core rate will keep falling. So this doesn’t change our …

17th January 2025

Services inflation in the euro-zone was stuck around 4% last year but we remain convinced that it will decline significantly in 2025. Data released today confirmed that euro-zone headline inflation rose from 2.2% in November to 2.4% in December. The core …

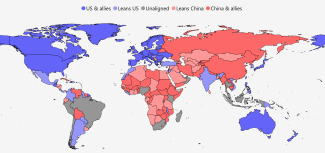

The Shape of the Fractured World in 2025 The share of the fracturing global economy that is accounted for by China and its geopolitical allies contracted in 2024, leaving it under a third the size of the US bloc at the start of 2025. This fall was in part …

December’s weaker-than-expected inflation outturn won’t sway Norges Bank: we still expect it to wait until March to start cutting interest rates. We suspect that it will then lower rates gradually, once per quarter, until the key policy rate reaches 3% in …

16th January 2025

This page has been updated with additional analysis since first publication. Outlook weak despite rise in production The small uptick in euro-zone industrial production in November will be of little relief to the beleaguered sector. Surveys suggest that …

15th January 2025

Germany still in the doldrums Preliminary GDP data for Germany suggest there is still no sign of the country exiting stagnation, with GDP down slightly in both Q4 and in 2024 as a whole. We forecast a very small cyclical recovery in 2025, but even that …

The CDU’s economic policy agenda, released today, clearly recognises the scale of Germany’s economic challenges and proposes some sensible policies to address them. But some of the measures are not ambitious enough and many will not be implemented in full …

10th January 2025

We expect the euro-zone economy to grow at only a sluggish pace this year, with southern economies outperforming the core. Germany’s election will lead to only a modest loosening of its restrictive “debt brake”. France’s budget deficit will remain very …

ECB to keep cutting rates gradually With data this week revealing that services inflation remained stuck at 4% in December, ECB policymakers will feel in no hurry to slash interest rates. (See here .) We have taken out the 50bp rate reduction that we had …

Weak retail sales at the end of last year The 0.1% m/m increase in euro-zone retail sales in November was a little worse than expected (CE +0.7%, consensus +0.4%) and follows a fall in sales of 0.3% in October (previously estimated at -0.5%). This …

9th January 2025

The outperformance of the peripheral economies since early 2022 is likely to continue over the next year, supported by high immigration, tourism growth and Next Generation EU funding. That said, growth in the periphery will not be particularly strong by …

November pick-up but outlook still poor German industrial production picked up in November. But the level of output was still very low by past standards and with industry facing several structural headwinds we expect the sector to continue to struggle …

This page has been updated with additional analysis since first publication. EC survey points to economy stagnating and price pressures remaining sticky The EC survey is broadly consistent with euro-zone GDP stagnating in Q4. It also suggests that …

8th January 2025

Inflation lower than expected, Riksbank to cut in January The fall in inflation in December will ease policymakers’ concerns about upside risks to inflation. We had previously been expecting them to wait until March before cutting the policy rate for a …

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

This page has been updated with additional analysis since first publication. Sticky services inflation suggests ECB will continue cutting slowly The continued stickiness of euro-zone services inflation means that the ECB is likely to keep cutting interest …

Inflation down in December and to fall sharply this year The fall in Swiss inflation in December suggests that the SNB’s decision to cut by a bumper 50bp in December was fully justified. We think the SNB will cut the policy rate by a further 25bp at its …

Higher-than-expected inflation in December Data for Germany and Spain suggest euro-zone inflation was higher than expected in December. However, we still think that inflation is likely to undershoot the ECB’s forecasts later this year causing the Bank to …

6th January 2025

The Alternative für Deutschland (AfD) has attracted attention recently because of its strong opinion poll ratings and endorsement by Elon Musk. The party has no plausible route to power after February’s elections, but it is influencing the policies of …

3rd January 2025

Next week will be a busy one for data releases in Europe. We think that the data will underline that core price pressures are continuing to ease gradually in the euro-zone, while economic growth remains weak. For those who were able to step back from work …

The termination of European imports of pipeline natural gas from Russia via Ukraine will only increase the EU’s dependence on imports of LNG and ensure that energy prices there remain much higher than in the US. The latest rise in EU natural gas prices …

2nd January 2025

Germany took a further step towards early elections this week as Chancellor Olaf Scholz intentionally lost a confidence vote in parliament as expected. Most political parties also published their manifestos. The main economic proposals of the CDU , which …

20th December 2024

The Riksbank’s decision to cut its policy rate by 25bp to 2.5% was widely anticipated and we expect it to cut just one last time next year, by 25bp in March. In contrast, Norges Bank left its policy rate unchanged today at 4.5% and is unlikely to start …

19th December 2024

Riksbank slows pace of cuts, likely to pause loosening at next meeting The Riksbank cut its policy rate by just 25bp today to 2.5% and it is unlikely to cut at its next meeting in January. Further ahead, we now expect just one more 25bp cut next year, in …

Underlying inflation remains high but is on a downward trend and we expect it to fall much further next year. This should prompt the ECB to cut interest rates a bit further than investors anticipate. Data published this morning revealed that euro-zone …

18th December 2024

This page has been updated with additional analysis since first publication. German economy set to remain weak The Ifo Business Climate Index (BCI) remained deep in recessionary territory in December. While the survey has overstated the weakness in the …

17th December 2024

Overview – We expect economic growth in the euro-zone to remain sluggish. This is partly due to adverse demographics and structural forces hampering the competitiveness of industry. But past monetary tightening will continue to weigh on investment and …

16th December 2024

This page has been updated with additional analysis since first publication. PMIs strengthen the case for looser monetary policy December’s PMI survey for the euro-zone suggests that the economy is contracting and that price pressures remain largely under …

Mood at the ECB shifting gradually In our view, this week’s ECB meeting didn’t spring any surprises, and the message was clear that we should expect further interest rate cuts. (See here .) Yet the market reaction during and after the press conference …

13th December 2024

This page has been updated with additional analysis since first publication. October worse than it looks, long-term outlook bleak October’s euro-zone industrial production data look much worse without Ireland, where the data are notoriously volatile. The …

Next Thursday, we expect the Riksbank to reduce its policy rate from 2.75% to 2.5% as it closes in on the end of its loosening cycle. In contrast, we think Norges Bank will leave its policy rate unchanged again next week at 4.5% as it waits until early …

12th December 2024

Today’s ECB policy statement and press conference suggest that policymakers are increasingly confident of meeting their inflation goal and increasingly conscious of downside risks to the economy. We think the outlook is weaker than the Bank believes and …

ECB likely to accelerate policy easing next year While the ECB’s decision to cut its deposit rate by 25bp was widely expected, the accompanying statement suggests that policymakers are less concerned than previously about upside risks to inflation and …

Bumper SNB rate cut, further to come This morning’s 50bp rate cut by the SNB, which brought the policy rate to 0.5%, came as a surprise to most economists. That said, it was balanced by a revised policy statement which implies that policymakers think this …

The price of natural gas in Europe was thrust into the spotlight during Europe’s energy crisis and remains a key political and industrial pressure point. In short, we expect natural gas prices in the EU to halve over the coming years as global LNG …

10th December 2024

GDP growth picked up in Q3 but timelier data suggest that it has slowed in Q4. We expect growth to remain sluggish next year regardless of whether President Trump raises tariffs on imports from Europe. We also think that inflation will be below 2% in …

6th December 2024

The end of Michel Barnier’s administration after just three months on Wednesday was something of an anticlimax for bond markets as it had already been discounted by investors. Spreads on French bonds have actually narrowed this week. There remains a lot …

Data released today show that euro-zone household consumption rose strongly in Q3. But slowing real income growth means that we expect spending growth to be subdued in the coming quarters. Meanwhile, investment and exports were weak in Q3 and the outlook …

In contrast to market pricing, we think that the SNB will be cautious and cut its policy rate by just 25bps, to 0.75%, next week as the Bank sticks to a gradual approach to loosening monetary policy. That said, the SNB is likely to lower its inflation …

5th December 2024

Consensus on ECB Governing Council points to 25bp cut next week But we expect policymakers to step up the pace of cuts next year… …and think the deposit rate will be just 1.5% by the middle of the 2025 While there is a strong case for the ECB to …

Retail sales lose momentum October’s decline in euro-zone retail sales followed a good third quarter for retailers. We suspect that the strength in sales in Q3 was just a one off and that growth will be subdued in the coming quarters. The 0.5% m/m fall in …

Riksbank will be unfazed by rise in inflation While all three key measures of inflation in Sweden rose in November, this does not change the underlying story that inflation is around its target level and is likely to stay there over the next year. CPIF …

An interactive guide to the fiscal sustainability challenges faced by euro-zone economies. This content was last updated on 13th May 2025. If you have subscriber access to this data, you can download it via the menu options in the top right of each …

Note: We’ll be discussing the French budget crisis in a Drop-In on Tuesday, 3rd December at 1000 ET/1500 GMT . Click here to register for the 20-minute online briefing. France is unlikely to have a government with a mandate to tighten fiscal policy …

3rd December 2024

This page has been updated since publication with additional analysis. Rise in inflation will prove temporary The uptick in Swiss inflation in November is likely to prove short-lived and should not prevent the SNB from cutting interest rates again in …

Unemployment rate set to rise next year With the unemployment rate unchanged at 6.3% in October, the euro-zone labour market appears to be holding up reasonably well. However, this looks set to change in the coming months as the outlook for economic …

2nd December 2024