Note: We’ll be discussing the UAE's exit from OPEC in an online Drop-In briefing on Wednesday, 29th April at 09:00 BST/16:00 SGT. Register here for the 20-minute session.

- This Update considers the economic and geopolitical implications of the UAE’s departure from OPEC, as well as the future of the group.

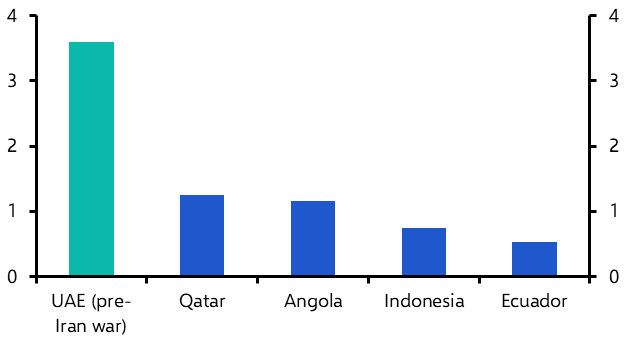

- 1) How unusual is it for countries to leave OPEC? It is not unprecedented for countries to leave the group. Indeed, Angola (2024), Ecuador (2020), Indonesia (2016), and Qatar (2019) have all terminated their membership with the group over the past decade (and Gabon, which left in 1995, rejoined in 2016). That said, it is worth noting that the UAE is a much larger and more influential oil producer within the group than the others at the time of departure. (See Chart 1.)

- 2) Does leaving OPEC always lead to higher oil output? Part of the UAE’s rationale for leaving appears to be that it wouldn’t be burdened by its “obligations” to the wider OPEC group, so that it has greater “flexibility” to produce more oil. For context, the UAE had previously been pushing for a more aggressive unwinding of group-wide oil output cuts whilst seemingly producing above their own official quota in recent years. In the near term, UAE oil output remains constrained by the effective closure of the Strait of Hormuz. As and when traffic flows more freely through the Strait, though, there appears scope for the UAE to raise output by roughly 1mn bpd (~1% of global oil demand) above pre-conflict levels to 4.5mn bpd.

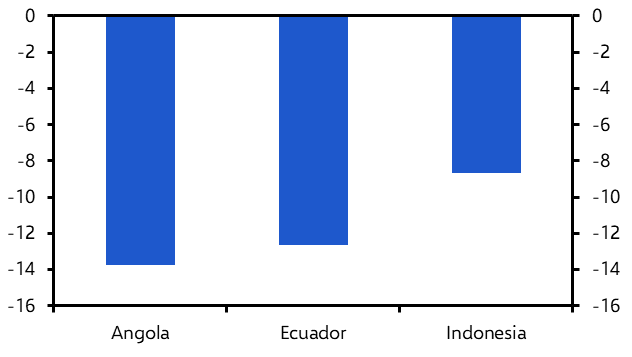

- A key lesson from previous examples of members leaving OPEC is that it is not a one-way ticket to higher oil production. In particular, Angola, Ecuador, and Indonesia all left the group following disputes over output quotas and oil production has fallen since then (see Chart 2), presumably in part due to a lack of investment in production facilities. For the UAE, however, a lack of investment probably won’t be an issue, especially given its strong balance sheet and the fact that it has recently been investing heavily to expand production capacity. So, the UAE could prove to be the exception.

|

Chart 1: Crude Oil Production at Time of OPEC Exit (Million Barrels per Day) |

Chart 2: Change in Monthly Oil Production Since Leaving OPEC (%) |

|

|

|

|

Sources: LSEG, EIA, OPEC, CE |

- 3) What does the UAE’s departure mean for the rest of OPEC? The UAE accounted for 12% and 9% of the total OPEC and wider OPEC+ oil production in 2025, respectively. And the loss of UAE oil output from the group reduces OPEC+’s share of global oil production from 47% to 42%. Meanwhile, the UAE’s exit increases Saudi Arabia’s influence over OPEC oil output policy even further. That said, it could also embolden other members to follow the UAE’s lead by leaving OPEC and OPEC+ or, at the very least, undermine group cohesion. For what it’s worth, Iraq and Kazakhstan also have a recent history of not sticking to output quotas.

- To be clear, this is not necessarily the death knell for OPEC and the wider OPEC+ group. But against the backdrop of growth in non-OPEC supply and the prospect of peak oil demand, a more fractious and weaker OPEC could constrain the group’s influence on oil prices. That could manifest itself in higher oil price volatility and, all else equal, skew the balance of risks towards lower oil prices over time. (We explored this in more detail in a report last year.)

- 4) What will be the economic impact for the UAE and the rest of the Gulf? In the very near term, there won’t be any impact. The de facto closure of the Strait of Hormuz means that the UAE’s ability to export oil is constrained by capacity on its pipeline to Fujairah. But assuming that the UAE could eventually pump an additional 1m bpd as and when the Strait reopens, that could provide a mechanical boost to the level of real GDP of around 7%.

- What’s more, the UAE is well placed to increase supplies and live with lower oil prices (particularly compared with other Gulf economies) given its diversified economy, lower reliance on oil revenues and substantial foreign currency savings; these amount to ~$2.5trn (or more than 450% of GDP). Prior to the war, we estimated that the oil price needed to balance the UAE’s current account was just $10-15pb.

- Saudi Arabia, Oman and Bahrain have considerably higher break-even oil prices (estimated at $60-80pb before the war). Fiscal policy will need to be tighter than would otherwise be the case. And, more broadly, the prospect of higher global oil supplies may prompt policymakers across the Gulf to accelerate diversification efforts.

- 5) What are the geopolitical implications of the UAE’s departure? Today’s announcement is another sign that the UAE is willing to ruffle feathers within the Gulf Cooperation Council (GCC), especially when it comes to its relations with Saudi Arabia. The two countries were closely aligned when Saudi Crown Prince Mohammed bin Salman moved up the ranks of the royal family a decade ago. More recently, however, the two countries have increasingly found themselves at odds over a range of regional issues, including conflicts in Sudan and Yemen. Saudi Arabia has also sought to challenge the UAE’s role as the region’s business and financial hub. The outbreak of the Iran war initially appeared to force the Gulf countries together. But the UAE has cut a frustrated figure as the war has dragged on, decrying the response from the rest of the GCC.

- There’s clearly a risk that the UAE’s decision to leave OPEC adds to tensions with Saudi, and potentially the wider GCC. There’s a wide range of possibilities of how this could play out, from reduced cooperation over key issues to more extreme scenarios akin to the blockade of Qatar in 2017-21. Either way, there could be disruptions to trade and investment flows that we explored in more detail here.

- The UAE’s stance on the Iran war, along with its decision to leave OPEC, could also be interpreted as further evidence that it is seeking to deepen ties with the US and Israel. The country was an early signatory to the Abraham Accords and has pledged large AI-related investments in the US. This was underscored by last week’s revelation that the UAE had requested a currency swap line from the US. (See here.) While speculative, the UAE’s decision – and the prospect for higher oil production – could be seen as a positive decision in US-Emirati ties insofar as it helps to reduce US energy prices.

Hamad Hussain, Climate & Commodities Economist, hamad.hussain@capitaleconomics.com

Jason Tuvey, Deputy Chief Emerging Markets Economist, jason.tuvey@capitaleconomics.com