- March trade data show that higher oil prices have already driven up demand for China’s green tech exports. And our analysis suggests that stronger NEV demand could see the auto sector alone add at least 1%-pt to China’s export growth in 2026. As a result, we’re revising up our export forecasts for this year.

- China’s export growth slowed sharply in March, after surging over the first two months of the year. That’s been widely cited as a sign that China’s has suffered as higher oil prices have weighed on global trade.

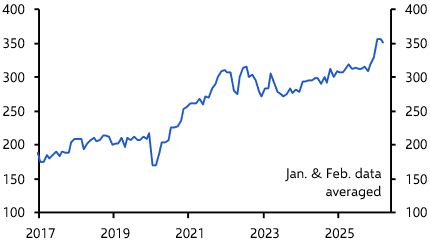

- We wouldn’t be so certain. Most of March’s slowdown was likely the result of seasonal factors. The Lunar New Year was unusually late this year, so the drag on output likely ran into early March. Indeed, in seasonally adjusted m/m terms, China’s exports only edged down a touch. (See Chart 1.) And early signs suggest that, aside from the maritime shipments directly impacted by the closing of the Strait of Hormuz, global trade has been holding up well.

- In fact, the conflict in the Middle East will provide a tailwind to China’s exports this year. That’s because higher oil prices are likely to drive up demand for green tech exports, an industry which China dominates.

- There are signs that demand has already picked up substantially. New energy vehicle (NEV, which include electric vehicles and plug-in hybrids) registrations in Japan, Korea and New Zealand more than doubled in compared to March last year, and they rose over 50% y/y in India, Australia and many European markets.

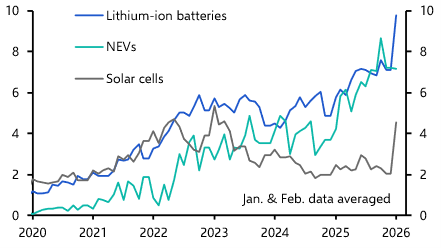

- This demand has yet to show up clearly in China’s EV export data. China’s exports of NEVs were flat in m/m terms in March (see Chart 2), and growth slowed in y/y terms. That’s not surprising – vehicles are logistically difficult to transport. Specialty roll-on, roll-off (Ro-Ro) ships are in short supply globally, and around 80% of capacity for this year has been pre-allocated. Some manufacturers such as BYD have invested in their own vessels, while a growing number of vehicles are shipped in containers with custom frames. But container shipping of autos is more expensive. The additional complexity and cost of transport means that some lag between the timing of orders being placed and shipped is likely.

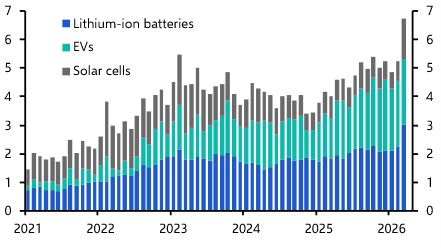

- By contrast, the impact of stronger green tech demand is already evident in China’s exports of lithium-ion batteries and solar cells (the other two of the “new three” green technologies promoted by the leadership). Exports of both surged in March. (See Chart 2 again.) The solar cell share of China’s exports more than doubled, while the combined share of the “new three” jumped to almost 7%, up from an average of 4.5% in 2025. (See Chart 3). Both batteries and solar cells can be shipped in standard containers, making it far easier for exports to ramp up quickly. What’s more, overcapacity in both industries is far more acute than in the EV sector. In the solar industry, capacity utilisation rates at some firms are reportedly as low as 40%, meaning production can increase rapidly in response to stronger external demand. EV exports should follow, albeit with a lag.

|

Chart 1: China Goods Exports ($bn, seasonally adjusted) |

Chart 2: China “New Three” Exports ($bn) |

|

|

|

|

Sources: CEIC, Capital Economics |

- Strong demand for green tech is likely to persist. Our baseline scenario is for Brent crude to end the year at $80/pb. But if tensions in the Middle East don’t unwind, oil prices could remain much higher.

- And China is well placed to benefit. The country accounts for around 25% of global NEV exports (by value) and well over 50% of global exports of solar cells and lithium-ion batteries. Green technologies were already providing a significant tailwind to China’s exports. While the “new three” only accounted for around 4.5% of China’s exports in last year, they drove almost 20% of China’s overall export growth.

- It’s difficult to predict precisely how much further demand will increase. But considering some scenarios helps to frame the potential upside. In a scenario in which the pace of the global shift towards NEVs doubles compared to last year (an 8.5%-pt increase in the NEV share of global car exports), China’s market share across both NEVs and ICE vehicles rises at the same pace as in 2025, and growth in global auto demand also remains unchanged, China’s auto exports would pick up by over 60%. Autos alone would drive an almost 1%-pt increase in China’s exports this year, up from 0.5%-pts in 2025. This accounts for the relative decline in ICE vehicle demand, and excludes non-car vehicles (like buses) which account for 30% of China’s NEV exports. If China’s total “new three” exports were to increase by 50% this year (up from 25% in 2025), that would add over 2%-pts to China’s export growth this year.

- An even more optimistic scenario seems possible if the oil price shock helps to jolt more economies (particularly in the emerging world) onto the steeper part of the S-shaped EV adoption curve, and China manages to capture a large proportion of that increase in demand. In a scenario where both global NEV adoption and China’s market share rise more rapidly (the NEV share of global car exports increases by 12%-pts, and China’s share of global NEV exports rises by 8%-pts), the boost from auto exports could be over 1.5%-pts. If total “new three” exports doubled, then the contribution of green tech alone could approach 5%-pts.

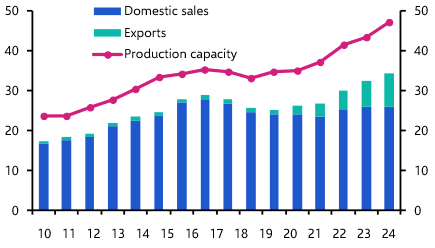

- Of course, demand is not the only factor that will determine the scale of the increase in exports. Production capacity also matters. While data on vehicle production and sales suggests that overall capacity utilisation in the auto sector was around 70% in 2025 (see Chart 4), much of the excess capacity is reportedly concentrated in ICE vehicle production.

- In March of last year, the vice minister of the Ministry for Industry and Information technology claimed that China had already built over 20 million units of NEV capacity. Actual output in 2025 was 16.6 million units, which would put the sector’s capacity utilisation rate at around 83%. While that’s much higher than the utilisation rates in the other “new three” industries, or ICE vehicle production for that matter, it still leaves significant room to ramp up output. If domestic sales remained flat this year, China could more than double its NEV exports without hitting capacity constraints. In other words, China is extremely well placed to respond to a surge in global demand.

|

Chart 3: Green-tech Share of China’s Exports |

Chart 4: Auto Production Capacity, Sales & Exports |

|

|

|

|

|

|

Sources: CEIC, CAAM, Capital Economics |

||

- Indeed, China has already shown that it can expand EV exports quickly – shipments picked up by almost 50% last year. And weak domestic demand means that manufacturers are selling at much lower margins at home. The bulk of China’s auto production still serves the domestic market (see Chart 4 again), so if external demand strengthens sufficiently, producers will have a strong incentive to reallocate output towards exports, even if that adjustment takes some time. What’s more, domestic NEV sales dropped back at the start of this year due to an end to tax exemptions for NEV purchases. That should free up some additional capacity for export.

- Crucially, any boost to green tech exports is likely to outlast the conflict in Iran. Repeated oil price spikes in recent years have underscored the fact that stable fuel prices cannot be relied upon in an uncertain global geopolitical environment. And at the same time, the upfront cost gap between NEVs and ICE vehicles has continued to narrow. In several countries including the UK, Brazil and Thailand, the cheapest EVs are now cost-competitive, even before accounting for lower running costs.

- As a result, we expect green tech exports to support China’s exports for some time. Alongside the AI driven surge in memory chip prices, this informs our view that China’s export growth will accelerate this year. We’re pushing up our export growth forecast for this year from 6% y/y to 11% y/y, which would be the fastest growth since the pandemic boom in global goods demand in 2021.