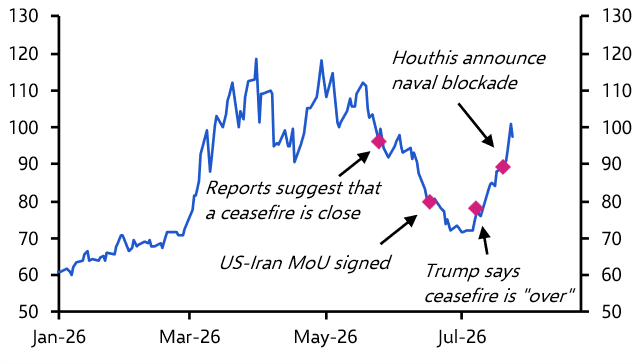

The surge in global oil and gas prices that has followed the outbreak of war with Iran has inevitably drawn comparisons with the energy shock that followed Russia’s invasion of Ukraine four years ago.

Back then, governments – particularly in Europe – rolled out large-scale fiscal support to shield households and businesses from soaring energy costs. At the same time, central banks across the developed world embarked on the most aggressive monetary tightening cycle in four decades. This combination delivered the worst performance for government bonds since the 1970s.

The obvious question is whether we are now witnessing a rerun of 2022. There are certainly parallels. But there are also some systemically important differences.

A smaller shock (so far)

The first is the scale of the shock. Admittedly, the potential magnitude of the current disruption could be even greater. While Russian oil and gas pipelines were a critical energy artery for Europe, the Strait of Hormuz is a vital artery for the entire global economy. Roughly a quarter of global seaborne oil trade and about a fifth of seaborne natural gas shipments pass through it. If the Strait were to remain closed for a sustained period, the resulting shock could dwarf the one triggered by the loss of Russian energy supplies.

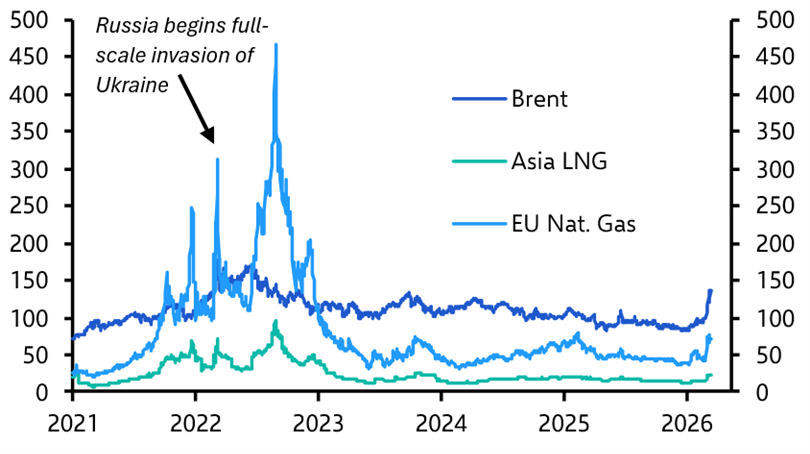

So far, however, market reactions have been comparatively restrained. Oil prices briefly spiked toward $120 a barrel last week, but have since traded in a range between the mid-$80s and the high-$90s. Additionally, the surge in natural gas prices, which was a real source of pain for Europe in 2022, has been much more modest this time. (See Chart 1.) Markets appear to be betting on a severe but short-lived campaign against Iran, broadly consistent with the more benign macro scenario outlined in our note last week.

|

Chart 1: Global Energy Prices (27th Feb 2026 = 100) |

|

|

|

Sources: LSEG Data & Analytics |

Not so tight

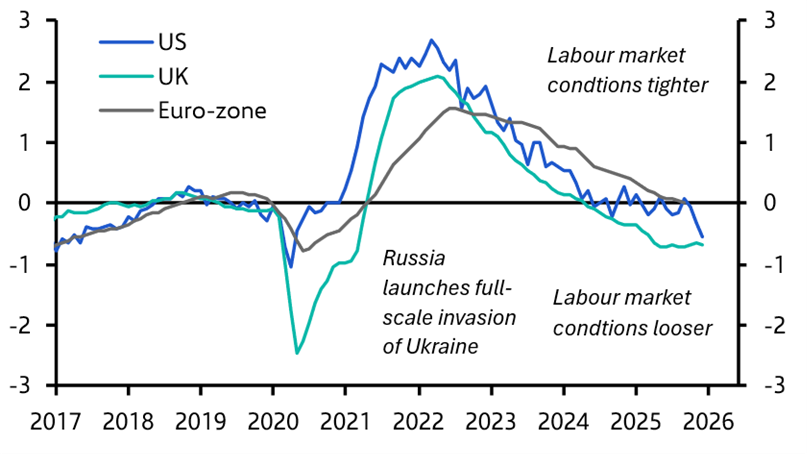

The second important difference is the cyclical positions of major economies. In 2022 labour markets were extraordinarily tight and inflation expectations were already elevated. That proved to be a toxic combination when energy prices surged.

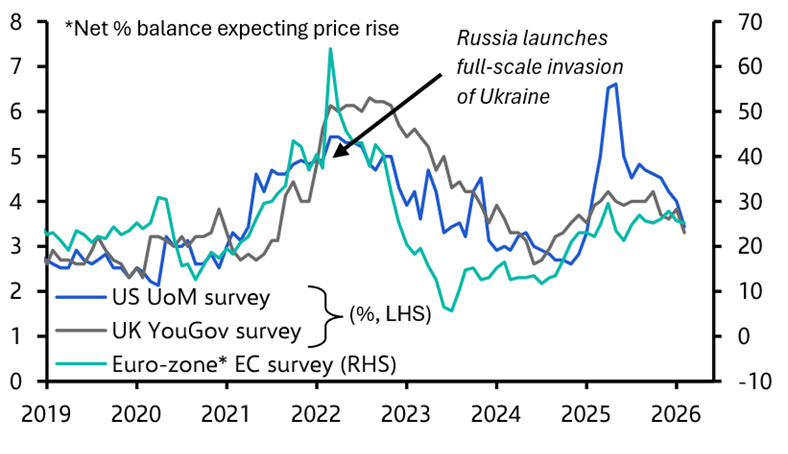

Today the picture looks rather different. Labour market conditions are, on the whole, looser. This is particularly true in the UK and the US, though the same trend is visible in the eurozone as well. Measures of labour market slack – such as the ratio of job vacancies to unemployed workers – are now markedly lower than they were four years ago. (See Chart 2.) Inflation expectations have also drifted down. (See Chart 3.)

|

Chart 2: Job Vacancy Rate (Z-scores, 2018-19 avg. = 0) |

|

|

|

Sources: LSEG Data & Analytics |

In 2022 the energy shock generated a surge in costs that firms were able to pass through relatively easily to consumers. The conditions that allowed that to happen are much less favourable today.

|

Chart 3: Surveyed Households 1-Year ahead Inflation Expectations |

|

|

|

Sources: LSEG Data & Analytics |

Behind the curve

The third important difference is the starting point of policy. Fiscal support by European governments following Russia’s invasion came on top of the enormous stimulus deployed during the pandemic. Households were already sitting on unusually large excess savings, which helped cushion the blow from higher energy prices even before governments stepped in.

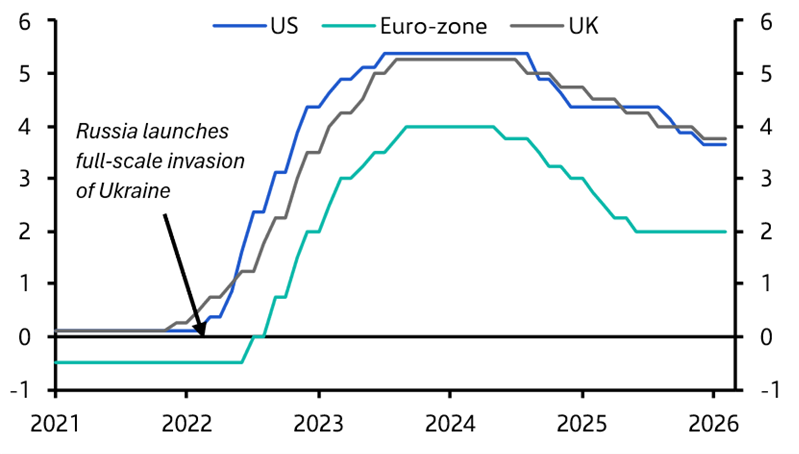

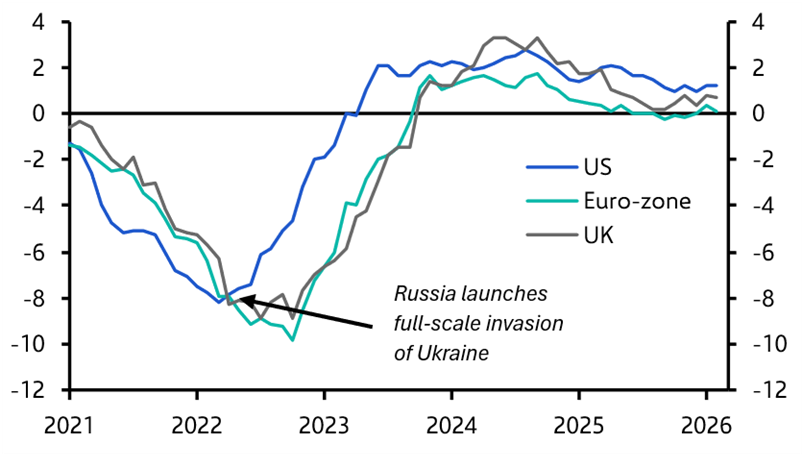

More importantly, monetary policy was extremely accommodative. Interest rates were near zero across advanced economies and negative in the euro-zone. (See Chart 4.) Real interest rates were deeply negative across the board. (See Chart 5.)

|

Chart 4: Policy Interest Rates (%) |

|

|

|

Sources: LSEG Data & Analytics |

|

Chart 5: Real Interest Rates (%, Policy rates less CPI inflation) |

|

|

|

Sources: LSEG Data & Analytics |

The situation today is very different. Policy rates are probably around neutral in the euro-zone and moderately restrictive in the UK and the US. In 2022 central banks were caught on the back foot when the energy shock hit and had to tighten aggressively simply to return policy to something like a neutral setting. That is not the case today.

This time is different

All of this raises the question of how policymakers should respond today. For governments, the key lesson from 2022 is that broad-based energy support is extremely costly and should be reserved for extreme circumstances. That may yet become necessary if the Strait of Hormuz remains closed for a prolonged period. But where possible, support should be tightly targeted toward those most in need.

Another lesson from 2022 is that price signals play a critical role in adjusting to supply shocks. Higher prices encourage households and firms to conserve energy and accelerate the search for alternative sources of supply. To the extent possible, that adjustment mechanism should be allowed to operate. (There are more fundamental lessons about the need to finally address critical chokepoints in our economic infrastructure, particularly around energy – but that’s a discussion for another day.)

Central banks can do little to influence global energy prices directly. Their task instead is to ensure inflation returns to target over the policy horizon and, in the case of the Fed, to meet its dual mandate of maintaining full employment. In practice, this requires weighing the upside risks to inflation from second-round effects against the drag on growth from higher energy costs.

A negative terms-of-trade shock driven by higher oil and gas prices should, in principle, weaken demand in net energy-importing economies. This could argue for looser monetary policy. But central banks must also guard against any drift higher in inflation expectations, which would risk embedding broader price pressures through wage bargaining and firms’ pricing decisions. The degree of labour-market tightness will be crucial in determining how far higher energy prices feed through to wages and core inflation.

Markets have already priced out the interest rate cuts across most advanced economies that had been expected over the coming months. That repricing looks broadly appropriate. But the bar for renewed rate increases remains high. Unlike in 2022, policymakers are not starting from a place in which policy is ultra-loose and labour market conditions are extremely tight. With interest rates already around neutral and labour markets looser, it would take a much larger and more persistent shock – and a clear deterioration in inflation expectations or wage-setting behaviour – to justify a renewed tightening cycle. That could still happen if the Strait were closed for a sustained period. But if the conflict proves short-lived, central banks may ultimately conclude that the best course of action is simply to stand pat for now.

Related content

All of our key analysis of the macro and market implications of the conflict in the Middle East can be found here. We’ll be briefing clients about the latest Bank of Japan meeting at 0800 GMT on 19th March (register here), and about the latest Fed, ECB and Bank of England meetings at 1500 GMT that same day (register here).