Europe Rapid Response Euro-zone HICP (June 2026) The substantial fall in headline inflation in the euro-zone in June left it below the ECB’s forecast, and if energy prices remain around current levels it will fall again in July. This makes us more... 1st July 2026 · 2 mins read

Japan Economics Update Weaker yen should lift inflation before long While any boost from higher energy costs to consumer prices will be short-lived, the continued weakening of the yen will provide a more longer lasting boost to consumer prices in Japan. Accordingly... 1st July 2026 · 3 mins read

Australia & New Zealand Economics Update RBNZ set to hike, but it will be a close-run thing We expect the RBNZ to begin its tightening cycle next week with a 25bp hike. With firms’ pricing intentions elevated, the Bank will want to guard against higher near-term inflation becoming embedded... 1st July 2026 · 6 mins read

Global Economic Outlook US strength points to renewed policy divergence With risks surrounding the Iran conflict receding, the focus is shifting back to domestic economic fundamentals, which point to widening growth and policy divergence across the major economies. The US... 30th June 2026 · 45 mins read

Africa Chart Pack Africa Chart Pack (Jun. 26) The US-Iran deal has triggered a slump in energy prices providing relief to Africa’s energy importers, particularly those in East Africa. Energy exporters such as Angola and Nigeria will see their... 30th June 2026 · 0 mins read

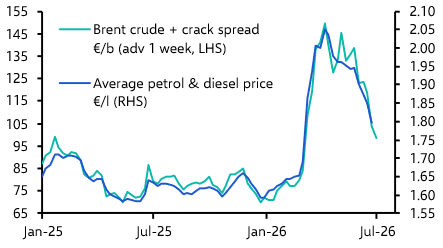

Europe Rapid Response Euro-zone national inflation data (June 2026) The national HICP data for June suggest that euro-zone headline inflation fell from 3.2% in May to 2.8% in June. That would leave it below the ECB’s forecast, making it less likely that the Bank will... 30th June 2026 · 2 mins read

India Chart Pack India Chart Pack (June 2026) The energy shock has weighed on India’s economy but GDP growth should still average 6.5% in 2026-27, an enviable rate by global standards. Rainfall in the early stages of the monsoon has been weak... 30th June 2026 · 1 min read

Canada Economic Outlook CUSMA uncertainty to slow recovery, delay rate hikes Uncertainty over CUSMA and lower immigration will slow the recovery, with average annual GDP growth a below-consensus 0.5% this year. A return to firmer growth of 1.7% in 2027 should see core price... 29th June 2026 · 14 mins read

Middle East & North Africa Chart Pack Middle East and North Africa Chart Pack (June '26) The US-Iran deal will allow the Gulf economies to begin a recovery. But it will take time for oil production and other sectors, such as tourism, to recover to pre-war levels. Most growth forecasts for... 29th June 2026 · 1 min read

Asia Economic Outlook AI boom rolls on, as falling oil prices provide relief Booming exports of AI-related products have helped offset the drag from higher energy prices and should continue to be an important driver of growth in Asia in the near term. The drop in oil prices... 26th June 2026 · 24 mins read

US Economics Weekly AI boom supporting growth and pushing up prices The fall in WTI to below $70pb has reduced the urgency for the Fed to raise rates, with futures shifting to pricing in a 70% chance of a 25bp hike by the September meeting, down from 95% last week... 26th June 2026 · 5 mins read

Africa Economics Weekly South Africa’s PPI surprise, Ebola response South Africa’s PPI surprised to the upside this week, but with crude oil back to pre-war prices and domestic harvests strong, we think the SARB rate hiking cycle is nearly done. Elsewhere, the Ebola... 26th June 2026 · 5 mins read

Europe Economics Weekly Energy prices normalising; digital euro coming (in 2029) ECB Executive Board member Isabel Schnabel said this week the Bank would need to raise interest rates further, in part because energy prices were still “measurably higher” than before the Iran war... 26th June 2026 · 7 mins read

India Economics Weekly Inflation and rates to rise by more than consensus expects This week we published our Q3 India Economic Outlook, which contains all of our latest forecasts and analysis of India’s economy and financial markets. The key points of difference between our views... 26th June 2026 · 3 mins read