The Central Bank of Egypt (CBE) kept its policy rate on hold on Thursday, and we continue to hold a non-consensus view that a fall in inflation later in the year will allow the CBE to resume its easing cycle in Q4. The decision to keep the benchmark …

6th August 2021

The Reserve Bank kept the repo rate on hold at a record low today and announced plans to ramp up government bond purchases on the secondary market, underlining its commitment to supporting the economic recovery. We don’t expect policy normalisation to …

The Reserve Bank of Australia signalled today that it’s unlikely to reverse the tapering of its bond purchases even as Sydney’s virus outbreak is getting worse. We still expect the tight labour market to deliver stronger wage growth and inflation than the …

The Czech National Bank (CNB) raised its two-week repo rate by 25bp to 0.75% at today’s meeting, and its communications signalled that policymakers will raise rates more quickly than they had previously signalled to tackle above-target inflation. We …

5th August 2021

Whether President Joe Biden chooses to reappoint Jerome Powell or to nominate Lael Brainard to be the next Fed Chair, it is unlikely in itself to have much impact on the near-term outlook for monetary policy. With up to three other vacancies for Biden to …

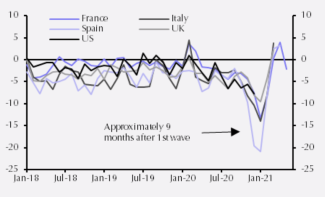

Although the headline data show bank loans stagnant (see Chart 1), that is mostly due to the forgiveness of Paycheck Protection Program loans and mortgage securitisations, with the broader evidence pointing to an acceleration in credit growth. Narrow …

The Monetary Policy Committee’s (MPC) policy statement sent a clear signal that higher interest rates are on the horizon. But there were few signs that it is preparing to hike rates soon. What’s more, we continue to envisage inflation dropping back more …

A decision by the Biden administration to increase US biofuel mandates in 2021 and 2022 has the potential to be a gamechanger for corn demand. However, we think that this is unlikely, which is one reason why we think that corn prices will fall over the …

The hawkish statement accompanying yesterday’s 100bp rate hike by the Brazilian central bank (to 5.25%) means that the Selic rate will increase further than we had anticipated. We now expect it to be raised to 7.50% by year-end (previously 6.50%). The …

While the unemployment rate is now back at its pre-virus low, a range of indicators suggest that there is still some slack in the labour market. We think the unemployment rate may eventually fall to 3.5%. However, mounting staff shortages will act as a …

The further slowdown we expect in China would probably be a headwind for some “risky” assets that are particularly sensitive to its economic cycle. It also informs our view that China’s sovereign bonds will outperform those of developed markets (DMs), and …

4th August 2021

If labour earnings growth took a decisive leg up, this would force central banks to rethink how long this year’s bout of higher inflation in advanced economies will last. The challenge is that the headline earnings data are affected by distortions that …

With demand slowly recovering and supply being pushed back, we no longer expect prime office rental falls in the Italian markets this year. However, the outlook is less encouraging, with a slowdown in office-based employment growth, more remote working …

Our expectations for GDP growth and inflation this year are close to the consensus but, beyond then, we think both will be weaker than most expect. This is likely to feed through to a fall in the loonie and we have recently toned down our expectations for …

We think that the upside risks to our US dollar view have increased. On a trade-weighted basis, we forecast a ~4% rise from its current level by the end of 2022; this Update considers what factors might deliver a more significant (10%+) rally in the …

The rapid spread of the Delta variant of the coronavirus adds to reasons to think that lacklustre economic recoveries lie in store for tourism-dependent economies in Africa, parts of the Middle East and South-East Asia. The weakness of tourism also …

The Bank of Thailand (BoT) left its policy rate on hold at 0.5% today as expected. Given the deteriorating outlook for the economy and with two of the six MPC members voting for a rate cut, we now think the central bank will loosen policy further this …

Surging demand for single-family homes has revived institutional investor interest in the single-family rental (SFR) market. With few homes available to buy, interest in build-for-rent (BFR) investment is growing. But given constraints in the home …

3rd August 2021

A bumper rise in utilities prices in October could contribute to CPI inflation climbing to a 10-year high of 4.4% in November. But as we don’t expect higher CPI inflation to feed through into higher inflation expectations or faster underlying pay growth, …

The widening of Romania’s current account deficit to a 10-year high partly reflects a rise in foreign firms’ reinvested earnings which is not a concern. But the trade balance has also worsened and the share of the deficit financed by stable forms of …

The $650bn allocation of IMF Special Drawing Rights (SDRs) that was finally signed off by the IMF yesterday should provide welcome relief to some frontier markets such as Ghana and Kenya that still face very high foreign borrowing costs. But it won’t …

The postponement of the planned privatisation of two state-owned banks to next year has dealt an all-too-familiar blow to the Finance Ministry’s hopes of raising significant revenues from asset sales in FY21/22. Rather than relaxing the overall fiscal …

The Reserve Bank of Australia delivered a hawkish surprise by not delaying the tapering of its bond purchases. And by predicting that it will hit its full employment mandate and make further progress towards its inflation target, it has opened the door …

The main takeaway from today’s batch of manufacturing PMIs is that industrial output growth looks to have peaked. Output indices have generally stopped rising, and new orders indices have come off the boil. Even so, with supply unable to keep up with …

2nd August 2021

June’s PMIs show that virus outbreaks have weighed on manufacturing in Southeast Asia while supply bottlenecks and weaker demand created headwinds for industry in China. In contrast, Indian industry rebounded sharply and manufacturing recoveries continue …

China’s July survey data suggest that manufacturing and construction activity have continued to cool, which supports our view that a slowdown in China will weigh heavily on industrial metals prices . The Caixin and official manufacturing PMIs both …

With the Delta variant lifting new infections to a record-high, calls for a “hard” lockdown are growing. If that happened, services activity would fall further but we doubt that the government would shut down industry. And with households and firms now …

The success of reduced working hour trials in Iceland was largely founded on adopting better working practices which, if embraced elsewhere, might offer no-cost ways of achieving better work-life balances. However, given that Iceland’s trials were centred …

30th July 2021

Saudi Arabia’s economic recovery appears to have been quite strong in Q2 and the further easing of virus restrictions and rising oil production means that GDP growth will continue to gather steam over the rest of this year and into 2022. The economy …

29th July 2021

The Q2 data showed that pan-European (excl. UK) transactions improved after their Q1 lows. But international travel restrictions, structural shifts in the office and retail sectors and tougher credit conditions mean that the recovery in investment …

The surge in input prices caused by supply shortages is starting to show signs of filtering through into higher output prices. Combined with upwards pressure on services inflation from a “vaccine bounce” later in the year, we now expect underlying …

The Fed took a small step toward the eventual tapering of its asset purchases by altering the language in the statement released today, but officials appear to be in no rush. We still expect an announcement in August or September, with the taper itself …

28th July 2021

The second quarter Housing Vacancies and Homeownership survey showed market conditions tightening in both the homeowner and rental markets, with vacancy rates at 56-year and 37-year lows respectively. In the homeowner market that will act to constrain …

In the early 2000s, a ‘glut’ of global saving may have helped restrain rises in long-term US bond yields, even as investors began to discount tighter monetary policy. We don’t think that similar factors explain the latest fall in yields, nor do we expect …

Policymakers in Nigeria kept their benchmark rate on hold at 11.50% at today’s MPC meeting and, if we’re right in expecting the economic recovery to disappoint, policy settings are likely to remain unchanged for some time. Meanwhile, the announcement on …

27th July 2021

The larger-than-expected 30bp interest rate hike by Hungary’s central bank (MNB) today was accompanied by hawkish comments that send a strong message about its intention to bring inflation back to its target. The tightening cycle is likely to be sharper …

We believe that the slump in net migration is holding back supply more than demand. Unless the government allows net migration to overshoot its pre-virus level for a prolonged period once the border reopens next year, we think that staff shortages will …

The recent gains in lender sentiment showed the real estate recovery is heading in the right direction. As lenders gain confidence, standards should start to loosen, and industrial and multifamily borrowers will continue to benefit. But uncertainty around …

26th July 2021

The decision by Tunisia’s President Kais Saied to sack the prime minister and freeze parliament has raised serious concerns about the future of democracy in the country and couldn’t come at a worse time for the economy, which is already reeling from the …

The slowdown that we anticipate in China over the next 6-12 months is best viewed as a return to normality following a period of above-trend output. While it will be a headwind to growth in some industrial commodity producers, we do not think it will …

23rd July 2021

While we no longer expect peripheral spreads to narrow this year, we still think that they will remain close to their current levels, which are close to the lowest since the Global Financial Crisis. Around a year ago, we argued that the spreads of 10-year …

The overarching message from today’s batch of flash PMIs was that higher inflation isn’t going away anytime soon in major advanced economies. Some of the inflation indicators edged away from their recent record highs, but that leaves them at historically …

Russia’s central bank (CBR) opted for a larger 100bp interest rate hike, to 6.50%, at today’s meeting and the accompanying communications provided clear guidance that the tightening cycle is nearing an end. With inflation likely to rise further and …

Birth rates have fallen in several advanced economies during the pandemic. Although we think that fertility rates will bounce back and there won’t be material long-term impacts, this presents a small downside risk to some of our long run forecasts for …

A rise in virus cases in Israel has prompted the government to re-impose restrictions on activity, including mask mandates and vaccine certification for large events. There are signs that the Pfizer vaccine may be much less effective at preventing …

We have revised down our forecasts for many of the G10 “high-beta” currencies and several currencies in EM Asia and LatAm. This update sets out the rationale behind those revisions and updates our key calls. Since the June FOMC meeting, currency markets …

The supermarket yield spread to “all-retail” has grown to almost the level it reached in 2009. However, we think there are good reasons for this. Admittedly there are risks ahead for the sector that could dent future prospects, but for now, supermarkets …

22nd July 2021

Though we think that the recent decline in the 10-year Bund yield is an overreaction, we expect it to rise only a little over the next couple of years, and by less than yields in many other developed markets . To recap, after rising for most of this year, …

The ECB followed through on its strategy review today by raising the bar for interest rate hikes in language which was probably a touch more dovish than expected. The Bank made no change to its guidance on asset purchases, but we think it will continue …

Policymakers in South Africa kept their benchmark rate unchanged at 3.50% today and the dovish tone of the communications supports our view that interest rates won’t rise until the middle of next year. Today’s decision by the South African Reserve Bank …