Filtered by Subscriptions: Global Economics Use setting Global Economics

Overview – Global headline inflation has fallen sharply from its peak a year ago and, despite a temporary setback due to higher fuel inflation, we expect it to fall a lot further over the coming year. The huge drag from energy inflation is now largely in …

24th October 2023

The full report is available to download from the button at the top right to Global Economics, Global Markets, Asset Allocation and The Long Run subscribers, as well as to CE Advance clients. If this is outside of your current subscription and you would …

17th October 2023

Chapter 4: Financial market implications …

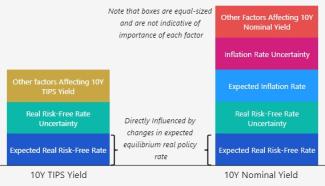

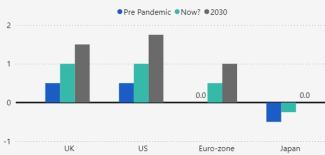

Chapter 3: Where will inflation (and nominal rates) settle? …

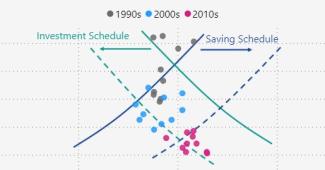

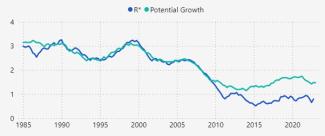

Chapter 2: How will the savings/investment balance affect r*? …

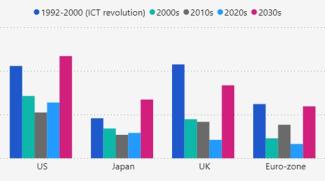

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

Perceptions matter at least as much as actual policies in determining fiscal stability. Accordingly, the surge in bond yields over the past month poses the greatest risk to those countries where the government’s commitment to fiscal rectitude over the …

16th October 2023

The latest activity and survey data have provided even more evidence that the resilience in activity in advanced economies over the first half of 2023 is now fading. High interest rates are clearly weighing on credit growth, and a further rise in debt …

13th October 2023

The government bond sell-off over the past three months raises uncomfortable questions around the risks of financial instability and the outlook for fiscal policy. This note takes stock of what has driven the rise in long-term sovereign bond yields and …

6th October 2023

The ‘higher for longer’ narrative on interest rates that is baked into market pricing is at odds with evidence of widespread falls in inflation. Higher oil prices mean that fuel inflation will be a bit higher than seemed likely a few months ago. But the …

5th October 2023

The sell-off in bond markets has taken a breather today, helped in part by softer data on the US labour market. However, the scale of the moves over the past week has invoked comparisons to previous financial crises that have been caused by sharp moves in …

4th October 2023

Note: We discussed the key takeaways from our Q4 Global Economic and Markets Outlooks in a Drop-In on Wednesday, 11 th October. To view the recording Click here . Table of Key Forecasts Global Overview – We think that the now popular assumption that …

3rd October 2023

September’s manufacturing PMIs suggest that global industrial activity stagnated at the end of Q3, and forward-looking indicators point to further weakness ahead. The recent rise in oil prices seemed to push up the prices of manufactured goods. But …

2nd October 2023

Global goods trade fell at its fastest pace since the pandemic in July and the timelier trade and survey data point to further declines in August and September. What’s more, given that we still expect several advanced economies to fall into mild …

28th September 2023

The September Flash PMIs add to evidence that economic activity in the US and Europe is weakening. This supports our view that the Fed, ECB, and Bank of England have finished hiking interest rates. Our estimate of the DM average composite PMI edged down …

22nd September 2023

We held a Drop-In yesterday to discuss the latest policy meetings of the Fed, ECB, and Bank of England and what they might mean for the future path of policy and financial markets. (See the recording here .) This Update answers several of the questions …

Despite all the talk of “higher for longer”, we believe that the global monetary policy tightening cycle is drawing to a close. In Q4, any final rate hikes in advanced economies will coincide with a number of cuts in emerging markets. And as we head into …

21st September 2023

On Tuesday 19th September, our Energy and Global Economics teams discussed the oil market outlook and its implications for inflation and monetary policy in an online briefing for clients. Watch the recording here . We are not convinced that the increase …

19th September 2023

While economic activity was generally more resilient than feared in the first half of 2023, there are growing signs that many major economies are losing momentum. We expect most advanced economies to experience mild recessions in the quarters ahead as …

14th September 2023

Although wage growth is clearly falling in the US, the same cannot be said for the UK and euro-zone despite some evidence of labour markets cooling there too. A further fall in inflation expectations and an easing in worker mismatches is probably needed …

13th September 2023

The G20 summit which concluded yesterday in New Delhi supported our view that the global economy is fracturing into US and China-led blocs, and that India still leans to the former. While the statement was light on explicit policies, calls to increase …

11th September 2023

Developments in the past few weeks have moved the dial somewhat on the global story. In major DMs, there have been more signs of activity softening either in terms of output or employment, evidence of disinflation continues to mount, and it has become …

7th September 2023

Although a rise in Chinese manufacturing output meant that the decline in global manufacturing activity eased slightly in August, the outlook for industry in advanced economies in particular remains weak. Meanwhile, although the PMIs also pointed to a …

1st September 2023

Not only did global goods trade fall in June, but timelier trade and survey data for July and August point to further declines. Meanwhile, with the lagged impact of high interest rates likely to weigh more heavily on demand for certain goods, it could be …

31st August 2023

August’s flash PMIs support our view that both the euro-zone and UK will slip into recession in Q3 and imply that the US is now barely growing. And with output prices still easing gradually, the surveys strongly suggest that we are at or close to the peak …

23rd August 2023

China’s push to develop the BRICS bloc into a geo-political counterweight to the G7 is likely to be thwarted by the competing interests and priorities of other member states. Nonetheless, positioning ahead of this week’s BRICS summit will provide some …

21st August 2023

Interest rate-sensitive activity in advanced economies has fallen, but is still holding up rather well given how much interest rates have risen. This is partly due to the rebound in auto sales and more recently mortgage approvals. But we still think …

15th August 2023

While economic activity was generally more resilient than feared in the first half of 2023, we expect global growth to disappoint in the coming quarters. We doubt that another bout of policy stimulus will radically improve the outlook for China’s economy, …

14th August 2023

The immediate global economic and market fallout from troubles at Chinese property developer Country Garden seems likely to be limited. Foreign exposure to China’s property sector has fallen sharply over recent years and policymakers should step in to …

With lingering pandemic and energy support measures coming to a close and governments returning one eye to previous fiscal targets, fiscal policy will tighten a little in advanced economies over the coming years. This will contribute to slower growth. But …

10th August 2023

Even though the financial strains that emerged after SVB’s collapse have dissipated, interest rate hikes have left overall financial conditions in major advanced economies close to their tightest since the GFC, posing downside risks to activity. As …

9th August 2023

The latest PMIs suggest that the decline in global manufacturing activity has further to run. At least weak activity is weighing on price pressures, which should lead to further falls in core goods inflation globally. The output component of the global …

1st August 2023

Global goods trade rose slightly in May, but timelier data point to a renewed fall in June. And as spending patterns continue to normalise away from goods towards services at the same time as higher interest rates start to bite, it will probably be …

28th July 2023

Overview – Global inflation has almost halved since September last year and this trend has further to run. Admittedly, the fall in headline inflation so far mainly reflects the drag from lower energy price inflation, which has almost run its course. But …

25th July 2023

July’s flash PMIs suggest that activity slowed further at the start of Q3. Industry remains the weak spot, but the outlook for the services sector has also deteriorated noticeably. And while this seems to be weighing somewhat on employment growth and …

24th July 2023

While the resilience in economic activity looks to have continued in May, the latest surveys point to GDP growth slowing in June. And in China, the post-reopening rebound appears to have already fizzled out. Meanwhile, the significant tightening in …

14th July 2023

The likelihood of an El Niño event in the second half of this year adds to upside risks to global inflation and downside risks to activity. For the advanced economies, higher prices of agricultural commodities could slow the decline in food inflation. But …

12th July 2023

The Fed’s new FCI does a better job of illustrating the tightness of US financial conditions than various other measures. But our own FCI has had a better record at capturing turning points in real activity in recent decades, is timelier, more versatile, …

6th July 2023

The latest PMIs suggest that not only did global manufacturing activity contract at the end of Q2, but the outlook for the manufacturing sector also seems to have deteriorated further. At least the improved supply-demand imbalance seems to be having an …

3rd July 2023

World trade fell in April and timelier data point to a further fall in May, partly due to a sharp drop in Chinese exports which reversed all of their rebound from earlier this year. And weak demand looks set to weigh on trade in the months ahead. …

29th June 2023

Note: We discussed the economic and policy risks around the ‘greedflation’ debate in a 20-minute online briefing on Thursday, 6 th July. Watch the recording here . The surge in inflation in advanced economies has not been driven by a widening of firms’ …

Central bankers have struck a hawkish tone at the ECB’s forum in Sintra this week, suggesting that rates haven’t yet peaked and cuts are not on the cards for some time. But there were some interesting differences in tone. Most notably, the ECB and BoE …

28th June 2023

Global Overview – Most advanced economies have so far dodged the recessions that we, and many others, had expected to start in the first half of this year. The relative resilience of activity can be pinned on several supply- and demand-side props to …

27th June 2023

June’s flash PMIs suggest that not only has activity in advanced economies slowed at the end of Q2, but the outlook has also deteriorated further. This is particularly true in the manufacturing sector, where orders have fallen sharply. Meanwhile, …

23rd June 2023

A series of high-level diplomatic meetings this week have raised hopes that strains in US-China relations will start to ease. But the politics of fragmentation was never likely to proceed in a linear direction. And even if there is a thaw in political …

20th June 2023

The recent resilience of labour markets partly reflects a lag before higher interest rates feed through fully to economic activity. But employment has also been supported by the industry-led nature of the economic slowdown and by the fact that firms are …

15th June 2023

While headline CPI prints have been encouraging in recent months, policymakers will be nervous about the stickiness of core inflation. Average headline inflation in major advanced economies had dropped from 8.5% late last year to below 6% in April, and …

14th June 2023

According to our proprietary interest rate-sensitive indicators, activity in advanced economies has so far proven remarkably resilient to higher interest rates. A lot of this has been due to a rebound in auto sales related to pandemic distortions, whereas …

7th June 2023