The war in the Middle East raises a broad set of macro and market questions. All of our analysis is collected on this page, and our summary views on some of the most pressing issues are outlined below:

- The economic consequences of the conflict will depend on the scale and duration of any disruption to energy supplies, but in most scenarios the impact on overall global GDP and inflation is likely to be modest.

- The impact on regions will be uneven. The euro-zone, UK and Asia are more exposed than the US. In this sense, the conflict is another reason to think that the US will outperform other DMs this year.

- A scenario in which global energy prices remain around recent levels ($80pb Brent crude; €50/MWh for European natural gas) will push up DM inflation by 0.3-0.4%-pts relative to a baseline in which energy prices were unchanged at end-February levels, with larger increases inflation in Europe and Asia and a smaller increase in the US. The impact on GDP will be limited.

- A more extreme scenario in which global energy prices rise much further ($100pb Brent crude; €100/MWh for European natural gas) will push up DM inflation by about 1%-pt relative to a baseline in which energy prices were unchanged at end-February levels. In Europe it could add over 1.5%-pts to inflation. In this scenario, real GDP growth is likely to be 0.25-0.5%-pts lower vs. pre-conflict baselines.

- The impact on the emerging world will vary. The Gulf states will see a hit to activity via disruptions to energy production and other sectors such as tourism. But in general most EMs will prove resilient. We do not anticipate widespread crises. The biggest risks lie in a handful of EMs with extensive energy subsidies and fragile fiscal/BoP positions (Egypt, Turkey).

- Central banks will not rush to hike interest rates in response to higher inflation. But a prolonged rise in oil and natural gas prices would slow the pace of rate cuts in those countries where central banks are still easing policy (notably the UK) and would be another reason to think that the Fed will cut lower interest rates by less than the markets expect.

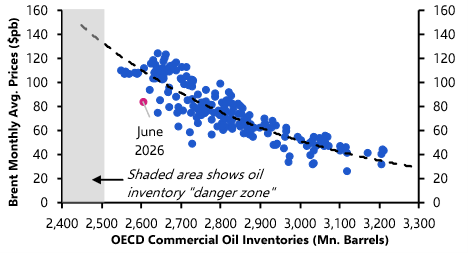

- The key issue for energy markets is the extent and duration of disruption of shipments through the Strait of Hormuz. This is clearly uncertain, but prolonged disruption could send oil prices above $100pb. That said, a greater willingness from India and China to import previously sanctioned Russian oil will help to relieve some of the upward pressure on oil prices. And while competition between Asia and Europe for LNG cargoes may continue to push up natural gas prices in both regions, the fact that the global LNG market is better supplied than it was in 2022 means that prices are unlikely to rise as far as they did back then.

- The uneven macro effects of the conflict have been reflected in moves in financial markets. US equities have outperformed those in Europe and Asia. We expect this to continue for the duration of the conflict. Likewise, the conflict has underlined the fact that the dollar’s status as a safe haven currency has not diminished (consistent with our long-held view). By contrast, government bond yields have risen and the price of gold fallen, highlighting how a stagflationary outcome would leave investors with few places to hide.

We will continue to respond to developments through written analysis, online Drop-In briefings and podcasts. Our Consultancy team is also available to provide additional analysis on the implications for your organisation.