One certainty of the Iran war is that its consequences will reverberate far beyond the regional conflict. A question that repeatedly comes up in conversations with clients surrounds the geopolitical fallout, above all whether this conflict could mark a breaking point in US-allied relations which splinters the Western bloc, even as global competition with China intensifies.

How the war has changed the world

It is clear that the war has intensified already significant strains in America’s relations with its long-standing partners. These follow a series of confrontations earlier this year, including Washington’s attempt to take control of Greenland – territory belonging to NATO member Denmark – and the controversial US operation to seize Venezuelan President Nicolás Maduro, which many allies viewed as an alarming precedent for the capture of a sitting leader. Against that backdrop, the Iran conflict may prove to be the moment where accumulated strains start to show themselves more clearly.

In particular, it casts a long shadow over the future of NATO. Several European governments have refused to send naval vessels into the region. Others have declined to allow US aircraft to use bases on European soil except for strictly defensive operations. These decisions have provoked fury in Washington. Criticism of NATO is no longer confined to the President. Long-standing defenders of the alliance – notably Secretary of State Marco Rubio – are now openly questioning its purpose and value.

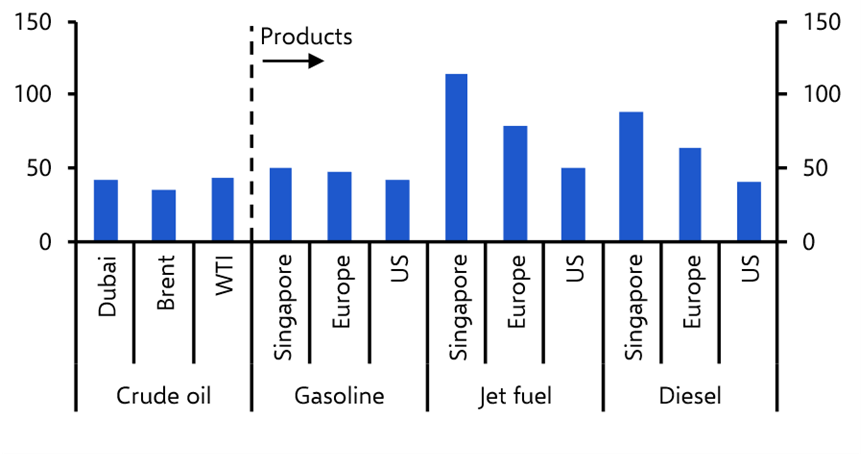

On the other side of the relationship, America’s allies have been hit hardest by the economic consequences of a war they did not want. Nowhere is this clearer than in the Gulf itself, where a deep recession is unfolding. Elsewhere, the effects of the war are already being felt by consumers at the petrol pump, with the largest price increases experienced by households in Asia and Europe, the large majority of which are US allies. (See Chart 1.)

|

Chart 1: % Change in Fuel Prices Since War Began (Latest = 15th Apr.)* |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics *US = Gulf Coast. Europe = Amsterdam, Rotterdam, Antwerp region. |

Even if the ceasefire holds and ultimately gives way to a more durable peace, the shock to energy markets is likely to push inflation higher in the near term, potentially to above 4% in some economies. This will squeeze real incomes and weigh on already sluggish growth.

Mapping the geopolitical fallout

Trying to map the long-term geopolitical implications at this stage is inevitably speculative. Nevertheless, a few points stand out.

First, extreme scenarios can no longer be ruled out. It is no longer impossible to imagine that the United States might pull out of NATO in principle – however constrained Trump is in practice – and even attempt to seize Greenland by force. The result would surely be a definitive and probably fatal rupture in the transatlantic alliance.

Short of such an outcome, however, the bar to a substantial decoupling between the US and its allies remains high.

Still more bipolar than multipolar

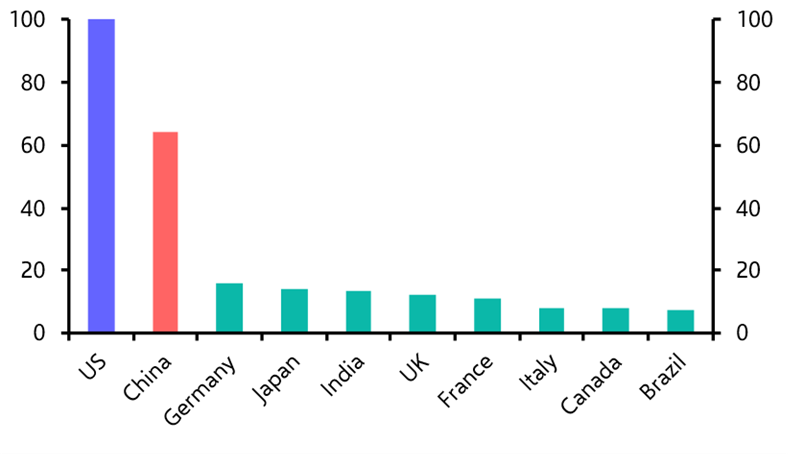

The world today is more bipolar than multipolar. The US and China are, by some distance, the two largest economies. (See Chart 2.)

|

Chart 2: Ten Largest Economies in 2024 (US = 100, market exchange rates) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

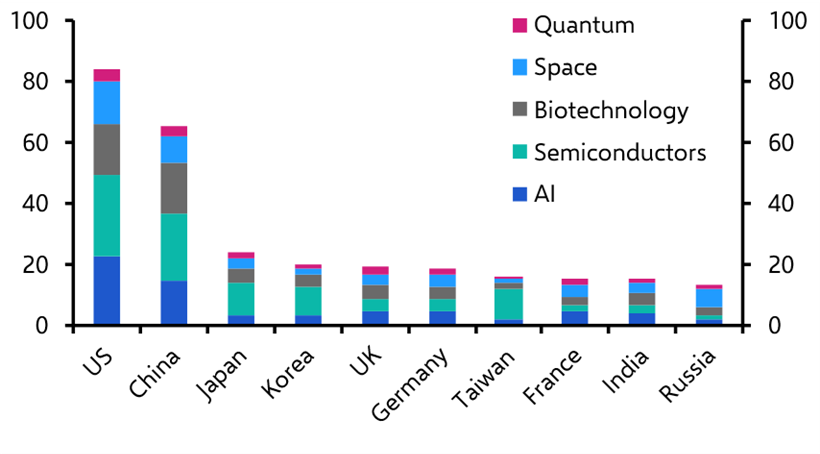

They also dominate many of the critical technologies that underpin modern economic and military power. (See Chart 3.)

|

Chart 3: Critical & Emerging Technologies Index |

|

|

|

Sources: “Critical and Emerging Technologies Index.” by E. Rosenbach at al. (2025), Capital Economics |

Accordingly, while several European countries may attempt to pursue the idea of “strategic autonomy” championed by France’s Emmanuel Macron, reducing dependence on both Washington and Beijing, this will be difficult to realise in practice.

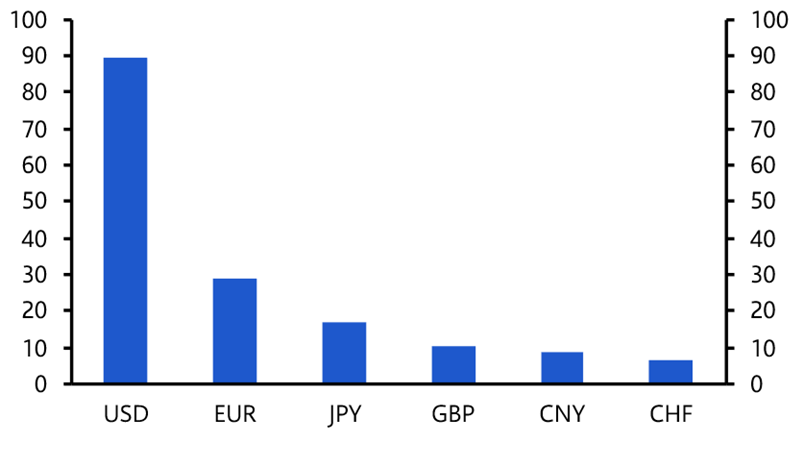

For example, unlike China, Europe and other American allies have no domestic alternatives to US digital infrastructure, payment systems or internet platforms. In AI, the choice is essentially between American and Chinese systems. The dollar continues to dominate the global financial system: according to the Bank for International Settlements’ latest survey of foreign exchange activity, it was involved in 90% of currency transactions in 2025. (See Chart 4.)

|

Chart 4: Foreign Exchange Turnover by Currency (2025, % of total) |

|

|

|

Sources: BIS Triennial Central Bank Survey, Capital Economics |

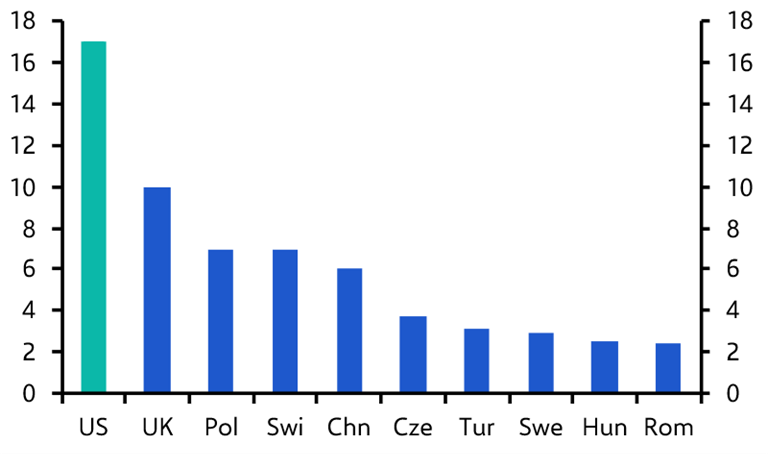

And from a more fundamental economic perspective, the US remains by far the world’s largest consumer market. Even if US allies could curb their dependence on US tech and the dollar, they would still be heavily reliant on US demand for their exports. (See Chart 5.)

|

Chart 5: Euro-zone exports by Destination (% of total, 2025) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics. |

The same argument applies to defence and security. Even if NATO were to fragment – or, perhaps more plausibly, be gradually hollowed out by Washington – European and Asian allies would still depend heavily on US military equipment and systems. A complete rupture in these relationships is therefore difficult to envisage.

The China question

None of this means governments will not attempt to reduce their dependence on the US. But the uncomfortable reality is that the only practical alternative in several areas is closer engagement with China – and that carries its own economic and national security risks.

How this balancing act evolves will therefore depend in large part on how countries assess China itself. Some are likely to shift closer to China. This could include parts of Asia such as Malaysia, Vietnam and – most importantly – India. Yet even here the outcome is unlikely to be a wholesale realignment towards Beijing. A more likely outcome is a form of pragmatic neutrality, with governments seeking to preserve room for manoeuvre between the two superpowers rather than tying themselves firmly to either camp.

In Europe and other countries in Asia, the calculation is different. Despite growing tensions with Washington, there remains no credible alternative security partner. Much of Europe is therefore likely to remain aligned with the United States – not only for defence reasons but also because of rising concern about economic competition from China. (One of the most important economic developments that has been overshadowed by the war has been a continued surge in China’s exports and trade surplus – a topic to which I’ll return in future notes.) Similar dynamics are visible across parts of Asia, including Japan, Korea and the Philippines, where Beijing’s expanding military presence is viewed with increasing unease.

For these countries, while more extreme outcomes can no longer be ruled out, the more likely result is not a hard break with the US but a shift in the nature of the relationship. In particular, for the remainder of the Trump administration at least, relations between the US and its traditional allies in Europe and Asia are likely to become more transactional and less grounded in shared political values. Beyond this, governments and corporate leaders in both regions will be looking beyond the current administration for a return to greater stability and predictability in US policy.

What it all means

From a macro and markets perspective, the implications of this shift in relations under Trump may be more limited than is often assumed. It may become harder for the US to enlist support from Europe and Asia in efforts to reduce dependence on Chinese technology or to decouple more broadly from China. Where it does succeed, it is likely to rely less on appeals to shared values and more on economic leverage, including the threat of tariffs and other forms of coercion. Likewise, in cases where Europe does move to decouple from China, this is more likely to reflect narrow economic self-interest than participation in a wider geopolitical realignment.

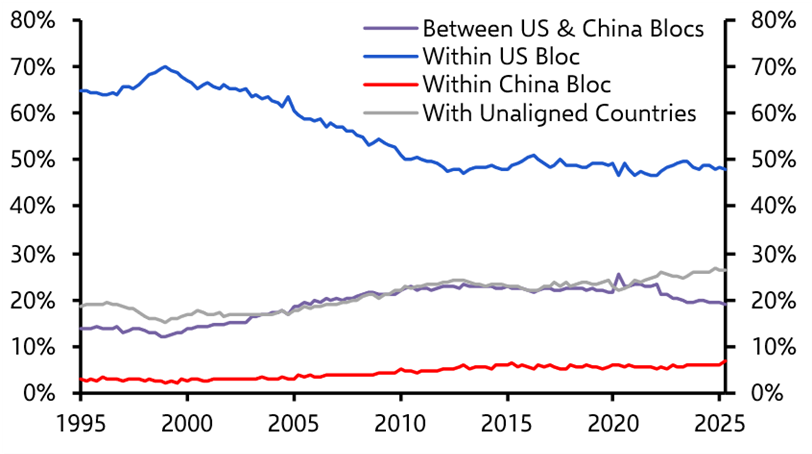

Even so, these developments are unlikely to alter fundamentally the structure of the global economy. The most likely outcome is that the web of economic, financial and institutional ties between the US and its traditional allies in Europe and Asia remains largely intact. In practical terms, this means that the majority of global trade will continue to take place between countries within the current US-bloc, and that the majority of global capital flows will continue to be concentrated within the bloc too. (See Chart 6.)

|

Chart 6: Share of Global Goods Trade (%) |

|

|

|

Sources: USITC, IMF, Capital Economics |

Further reading

We’re continuing to follow the conflict’s global macro and market implications, including most recently the blockade’s impact on the Iranian economy, alternatives to the Strait of Hormuz and the initial hit to world trade. All of our coverage of the conflict can be found here. Our fracturing framework explores the emergence and shape of competing US and China-led economic blocs.