What will happen to global trade now that the contours of Donald Trump’s tariffs regime are starting to take shape? It’s a question that kept cropping up in talks with clients in Copenhagen last week – for the shipping companies which are so central to the Danish economy, it’s a critical issue. But it’s also a question of much wider importance, with ramifications that will reach into financial markets and across the world economy.

Back to the future

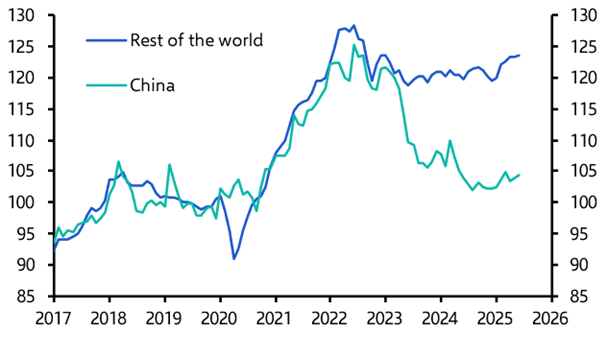

During Trump’s first tariff salvo that began in 2018, two things stood out. First, there was no collapse in global trade. In fact, as a share of world GDP, trade actually increased up until the pandemic struck in 2020 and is today still close to its all-time high. (See Chart 1.)

|

Chart 1: Global Goods Trade (% of world GDP, seasonally-adjusted) |

|

|

|

Sources: CEIC, Capital Economics |

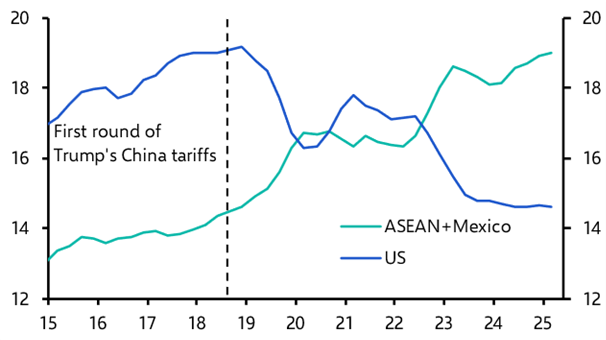

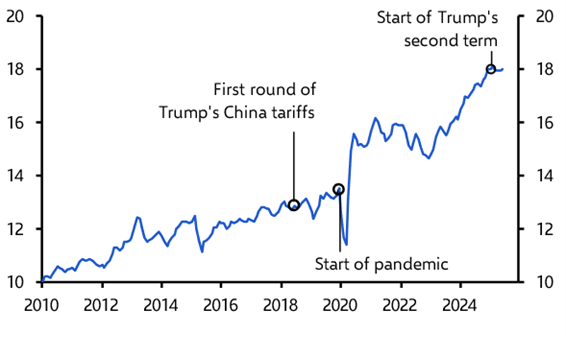

Second, exporters moved quickly to blunt the impact of Trump’s tariffs, leading to a notable rerouting of trade flows. This was particularly true of those in China, which were the focus of Trump’s first round of tariffs. From 2018 onwards, the share of Chinese exports going directly to the US fell sharply, while those to countries such as Mexico and South East Asia rose. (See Chart 2.) This wasn’t because those countries suddenly developed an insatiable appetite for Chinese goods. Instead, they became staging posts for Chinese producers, whose goods were effectively reboxed and shipped on to the US in order to avoid tariffs.

|

Chart 2: China Exports by Destination (% of total, rolling 12m) |

|

|

|

Sources: LSEG, Capital Economics |

Rerouting yet to get going

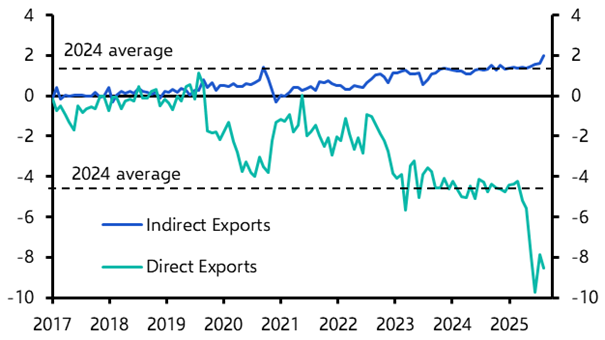

This time, things look a little different. So far, there has been much less rerouting. Our estimates suggest that the share of China’s exports going to the US has fallen by about 4%-pts this year, whereas the share of China’s exports being shipped indirectly to the US has increased by only 0.5%-pts. In other words, only around one-eighth of the decline in China’s exports to the US has been offset by rerouting through third countries. (See Chart 3.) Contrast that with 2017–18, when perhaps a third or more of the fall in direct exports from China to the US found their way back through indirect routes.

|

Chart 3: Change in US share of China’s Exports since Jan 2017 (%-pts, seasonally adjusted) |

|

|

|

Sources: LSEG, Capital Economics |

Timing matters, of course. It took firms a while to adjust supply chains in the first trade war, and the same is likely to happen again. Given time, Chinese exporters will almost certainly find ways of shipping goods into the US via third parties. But there are limits. Countries like Mexico are increasingly reluctant to serve as middlemen. After all, there is little economic value in merely repackaging Chinese goods for the US market – no jobs are created and no real value is added – and it risks incurring Trump’s wrath and potentially higher tariffs as bilateral trade surpluses with the US inevitably increase. With the USMCA regional trade deal up for renegotiation next year, Mexico in particular is treading carefully. It is planning punitive tariffs on Chinese imports, partly to curry favour with Washington, but also to discourage such rerouting in the first place.

A sense of perspective

So where does this leave world trade? Perspective is needed. The US may be the world’s biggest consumer market, but it still accounts for only about 8% of global imports. That means 92% of world trade is untouched by Trump’s tariffs. If you strip out USMCA-compliant goods, which are currently tariff-free, the unaffected share rises to almost 95%.

Another way to view matters is through the lens of US-China fracturing – the splintering of the global economy into two blocs centred on its largest economies, which we think will be the central force reshaping the world over the next decade. The scale of the threat to trade here is also relatively low. As things stand, only 15% of global trade takes place between the US and China blocs. Moreover, if efforts to reduce ties between the blocs are contained to strategically important areas, the share of global trade that is potentially affected by fracturing falls further, to well below 10%. The point here is that both Trump’s tariffs and US-China fracturing will affect only a small share of global trade.

Global trade now shaped by China

There is also a tendency to see global trade entirely through a Western lens. Yet many of the biggest forces reshaping trade today stem not from Washington but from Beijing. China continues to overinvest in production capacity, churning out more goods than its domestic market can absorb and sending the surplus abroad. To shift this glut, Chinese firms have been slashing export prices. They have fallen by roughly 25% since 2022, while export prices elsewhere have been broadly flat. (See Chart 4.) To take market share, Chinese firms are using the same aggressive pricing strategies that have fuelled Beijing’s worries about deflation in China’s economy.

|

Chart 4: Goods Export Prices (2019 = 100) |

|

|

|

Sources: LSEG, Capital Economics |

The result has been a surge in exports from China to the rest of the world. Between 2018, when Trump first introduced tariffs on China, and the start of this year, China’s share of global exports increased from about 13% to 18%. (See Chart 5.) And it has remained steady since the start of this year, despite the huge increase in US tariffs on China during Trump’s second term in office.

|

Chart 5: China’s Share of World Trade (%, volumes) |

|

|

|

Sources: LSEG, Capital Economics |

This strategy has adverse economic consequences. Almost one in three Chinese manufacturers are now loss-making, fuelling a structural slowdown in productivity growth. In response, Beijing has stepped up efforts to tackle overcapacity via its so-called “anti-involution” campaign. But structural forces – in particular high domestic savings and investment rates – mean this will have to overcome significant hurdles. The chances of a meaningful reset to China’s economic model are low.

Put it all together, and the immediate trade picture is one of stagnation rather than collapse. Unlike the first trade war, when trade volumes actually rose, this round is likely to lead to global trade as a share of GDP edging down a little over the next few quarters before flattening out in 2026. Rerouting will pick up, but probably not to the same degree as before.

Tariffs may have dominated the headlines, but over the next five years the greater risk lies not in Trump’s trade agenda itself, but in the mounting international backlash against China’s excess capacity spilling into global markets.

In Case You Missed It

- Track how much Chinese firms are rerouting goods to avoid tariffs in our interactive China Rerouting Dashboard.

- Our LatAm team will be exploring Brazil’s economic outlook in an online Drop-In briefing on Tuesday, to be followed by our Asia team on Thursday for an online briefing about big policy moments in China, India and Indonesia.

- Franziska Palmas wades through the details of Germany’s new budget to explain why Berlin’s widely celebrated decision to remove the country’s debt brake will have less of an economic bang than most expect.