While financial markets have swung on the apparent de-escalation and re-escalation of the Iran war, the bigger structural story is quietly reasserting itself: global imbalances are back, and were a major focus of the IMF’s Spring Meetings last week. But today’s imbalances differ in critical ways from those of the early 2000s.

The concept of ‘global imbalances’ may seem vague, but it reflects a balance of payments reality, referring to disparities in countries’ current account positions spanning trade in goods and services as well as investment income. Because the balance of payments must sum to zero, large surpluses in some economies are mirrored by equally large deficits elsewhere.

Imbalances aren’t inherently problematic. Indeed, some degree of imbalance is both natural and efficient. Capital should flow to countries where the marginal return is highest, causing them to run a current account deficit (and the country from which the capital flows, a surplus). The concern arises when these imbalances become large and persistent, creating vulnerabilities. This is particularly the case for deficit countries, which depend on capital inflows to allow them to consume more than they produce. This leaves them reliant on what economists, borrowing from Blanche DuBois in A Streetcar Named Desire, call “the kindness of strangers”. A pullback in these inflows can cause a painful contraction in domestic demand and problems servicing external liabilities.

History provides stark warning. The build-up of imbalances was a feature of the years leading up to the 2008 global financial crisis, and imbalances within the euro-zone culminated in its crisis in the early 2010s. Large imbalances also underpinned a string of crises across emerging markets in the 1980s and 1990s.

A changing configuration

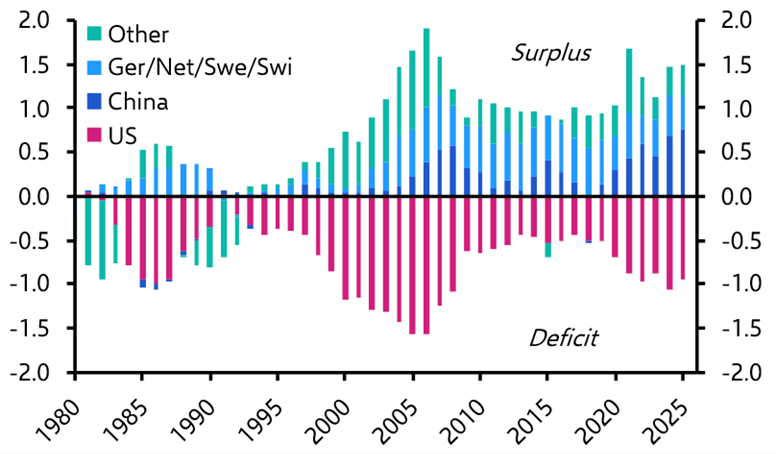

Today’s pattern of imbalances differs in important respects from that seen in the early-2000s. At that time, large surpluses in China, Germany, Japan and major oil exporters were mirrored by substantial deficits in the United States and parts of Europe. (See Chart 1.)

|

Chart 1: Current Account Balances (% of World GDP) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

While the US remains the world’s principal deficit economy, its external shortfall has narrowed relative to global GDP. Its current account deficit peaked at 1.6% of GDP in 2006 but was equivalent to “only” 1.0% of global GDP last year. This is due in part to its transformation from a large net energy importer into a small net energy exporter. In contrast, China’s surplus has grown in global terms and now exceeds its pre-crisis peak relative to world output. According to our adjusted measure, which takes account of changes to methodology and the treatment of contract manufacturing, China’s current account surplus was equivalent to 0.8% of GDP last year, above the 0.7% of GDP it reached in 2008.

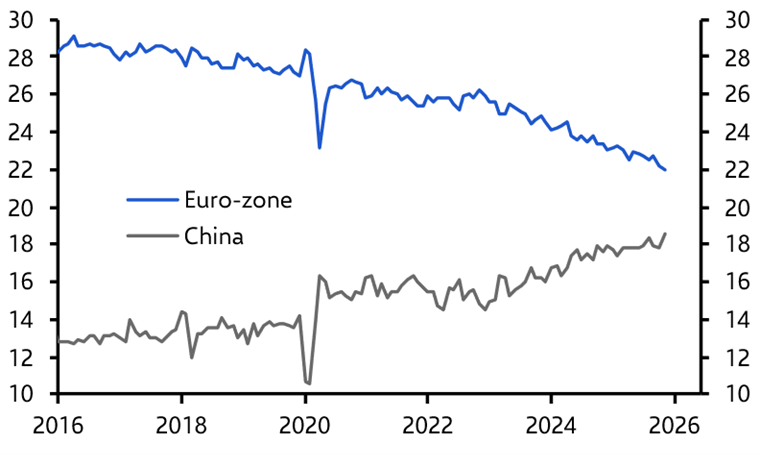

This raises an obvious question: how can the world’s largest surplus (China) increase as a share of global GDP compared to the mid-2000s while the world’s largest deficit (the US) has fallen? The answer lies in what has happened in other surplus economies. The surplus of the oil producers is now much lower than in the mid-2000s, thanks in part to a shift in the US’s net energy balance. Perhaps more importantly, though, China has moved decisively up the value chain, capturing market share from other export-oriented economies, most notably Germany and the rest of the euro-zone, but also Japan and Korea. (See Chart 2.) As a result, their surpluses have diminished compared to the mid-2000s.

|

Chart 2: Share of Global Real Goods Exports (%) |

|

|

|

Sources: CPB, LSEG Data & Analytics, Capital Economics |

Why it matters

The risks associated with imbalances have also changed in subtle ways since the mid-2000s. For deficit economies, the classic concern – a sudden stop in capital inflows – appears less acute than in the past. Deficits are generally smaller and there are fewer signs of domestic financial excesses.

Instead, attention has shifted towards surplus economies and the broader implications of China’s export strength. Two issues stand out. First, intensifying competition from Chinese firms is weighing on growth in other surplus economies. This is particularly the case for Europe, and the challenges are especially acute for its largest economy, Germany.

The second issue relates to the geopolitical and strategic dimensions of imbalances. The backdrop today is very different from that in the 1990s and 2000s: that era of multilateralism and integration has been replaced by one of increasing geopolitical rivalry between the US – and by extension what we think of as “the West” – and China. China’s growing dominance in sectors such as electric vehicles, batteries and other advanced manufacturing raises questions that extend beyond economics into national security and industrial resilience. This is an area where traditional economic frameworks have little to say. Efficiency gains from trade must now be weighed against concerns over supply-chain security and technological dependence.

Prospects for adjustment

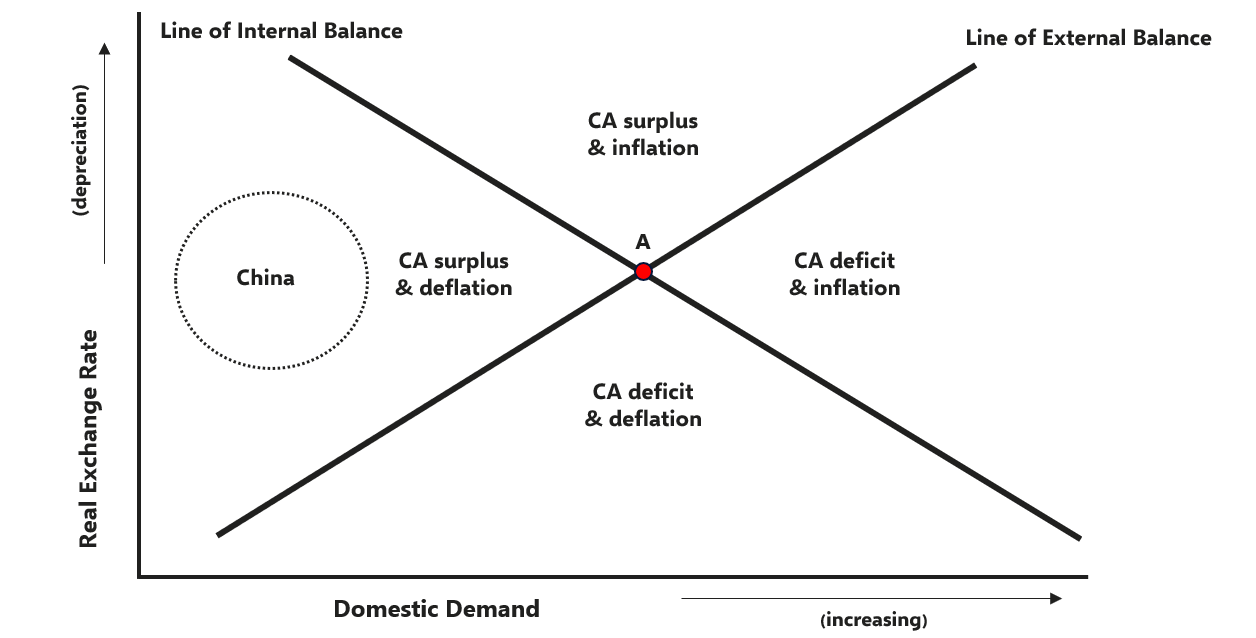

Market mechanisms for correcting imbalances – most notably exchange rate adjustments – may play a role. China’s real exchange rate is undervalued, perhaps by around 10%. However, currency movements alone are unlikely to deliver meaningful rebalancing without deeper structural changes.

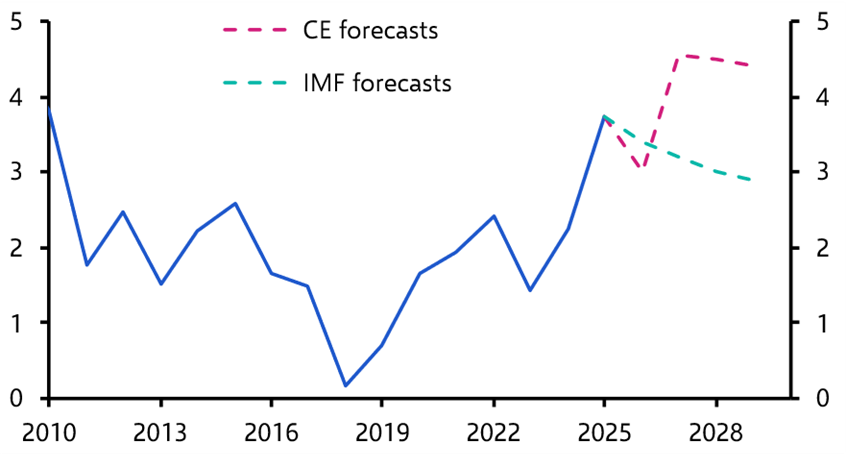

In China’s case, that would require a shift away from high savings and investment towards stronger household consumption. At present, there is little evidence of such a transition. Policy priorities, as articulated in the latest Five-Year Plan, remain focused on increasing industrial capacity and technological self-sufficiency. While the IMF forecasts that China’s surplus will start to fall over the coming years, we are more skeptical. (See Chart 3.)

|

Chart 3: China Current Account Balance (% of GDP) |

|

|

|

Sources: CEIC, IMF, Capital Economics |

However, it is wrong to place the burden of the adjustment on the surplus country. Deficit countries must also adjust. In particular, they must rein in domestic demand – in effect, bringing spending closer to productive potential. For the US, this means shrinking the federal budget deficit through a period of fiscal consolidation. (This is another important way in which the situation today is different from the mid-2000s, when the roots of “overspending” in the US lay in the private sector.)

A coordinated global adjustment – in which the US reduces its fiscal deficit while China boosts domestic demand – remains theoretically plausible. In practice, it appears highly unlikely given the current geopolitical climate.

A geopolitical challenge

Past episodes in which imbalances have been narrowed via policy adjustments have often relied on cooperation among allied economies. The clearest example of this was the 1985 Plaza Accord, in which the US agreed to measures to reduce its deficit, while Japan and Germany took steps to reduce their surpluses. Today, the principal actors – the US and China – are strategic competitors.

Donald Trump’s planned visit to Beijing next month will likely culminate in a deal that the president will tout as a major win, with China agreeing to buy more US goods and narrow its bilateral surplus with America.

The reality is that this will do nothing to address the root causes of imbalances, meaning they are likely to persist. This in turn suggests that trade frictions between the world’s two largest economies are likely to continue throughout this administration and beyond.

What it all means

For investors and businesses, there are three conclusions. First, a crisis similar to 2008’s does not appear imminent. Rather, global imbalances are set to remain a source of friction in the international system over the years to come.

Second, this will manifest in recurring episodes of market volatility and policy intervention – particularly in the context of US-China relations. Any apparent “deals” are unlikely to address the underlying drivers and may therefore prove temporary.

Finally, China will remain a source of growing export competition for other traditional surplus economies, particularly Germany. This will compound the growth challenges facing Europe’s largest economy and over time draw policymakers in the region into greater conflict with those in China.

Join our economists this Thursday for an online Drop-In briefing on China’s impact on Europe’s economy. Register here to join the discussion.