There's a good chance that this week's meeting between Donald Trump and Xi Jinping in Beijing will generate far more attention than substance. The optics of the leaders of the world's two biggest economies meeting face to face are powerful. But the reality is likely to be rather more modest: an attempt by both sides to stabilise a relationship without addressing the deeper forces that are pulling them apart.

Setting a low bar

The immediate objectives on both sides appear relatively modest. Beijing reportedly wants an extension of the trade truce that was agreed when Trump and Xi last met in October – perhaps by a year – alongside assurances that Washington will refrain from imposing fresh tariffs or export controls. It would also like some rollback of existing restrictions, especially those affecting advanced semiconductors, memory chips and chipmaking equipment. China may also seek subtle changes in US language over Taiwan, nudging Washington from “not supporting independence” towards explicitly “opposing independence”. This may be a step too far for the US. When it comes to Taiwan, continuity remains the most probable outcome.

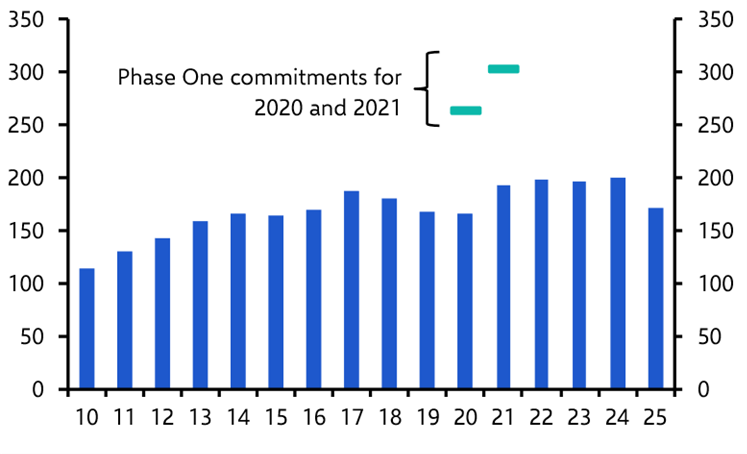

Washington’s goals are even narrower. It wants China to commit to increased purchases of US goods – particularly agricultural products, aircraft and energy – and to maintain flows of strategically important rare earth minerals. Beijing is likely to agree to these requests, although it is worth keeping in mind that it fell well short of the purchase targets set in the so-called ‘Phase One’ deal that was agreed during President Trump’s first term. (See Chart 1.)

|

Chart 1: China’s Imports from the US and its Phase One Commitments ($bn) |

|

|

|

Sources: BEA, Capital Economics |

The US would also like China to increase diplomatic pressure on Iran to end the war and reopen the Strait of Hormuz. Beijing may also agree to this, although we doubt it will expend significant geopolitical capital to bring to an end a war that has so far inflicted relatively little pain on its own economy.

A managed truce suits both sides

Neither side is therefore aiming for a major reconfiguration in the bilateral relationship. The immediate objectives are more modest. This reflects the fact that deep strains continue to lurk beneath the surface.

China’s latest Five-Year Plan lists national self-reliance – particularly in areas of technology – as a core priority. This is motivated in part by a desire to reduce its dependence on Western technology. But while China wants to decouple from the US in strategically important areas, it wants to do so on its own terms. A managed truce would allow China the time to increase self-sufficiency gradually and in a managed way.

The dynamics on the US side are more complicated. Last year’s trade war between America and China exposed economic vulnerabilities on both sides. In particular, China’s restrictions on rare earth exports were an important reminder that economic interdependence cuts both ways. President Trump discovered that the US did not, in fact, “hold all the cards”.

This appears to have prompted a shift in approach in Washington. The Trump administration has toned down some of its more aggressive anti-China rhetoric. It has also softened parts of its investment restrictions on China. And President Trump has played up the strength of his personal relationship with President Xi. Yet it would be a mistake to interpret this as a structural reorientation of US policy. Politicians on both sides of the aisle continue to view China as the key geostrategic threat facing the US. Despite the change in tone over the past six months, the US has continued to pass legislation that accelerates decoupling. In December it banned the purchase of foreign drones (a move clearly aimed at China); last month it banned testing labs located in China and Hong Kong from certifying electronics for the US market due to national security risks.

The geopolitics-balance of payments feedback loop

One point that is often overlooked is that geopolitical and global macro strains are developing in a way that over time are becoming self-reinforcing.

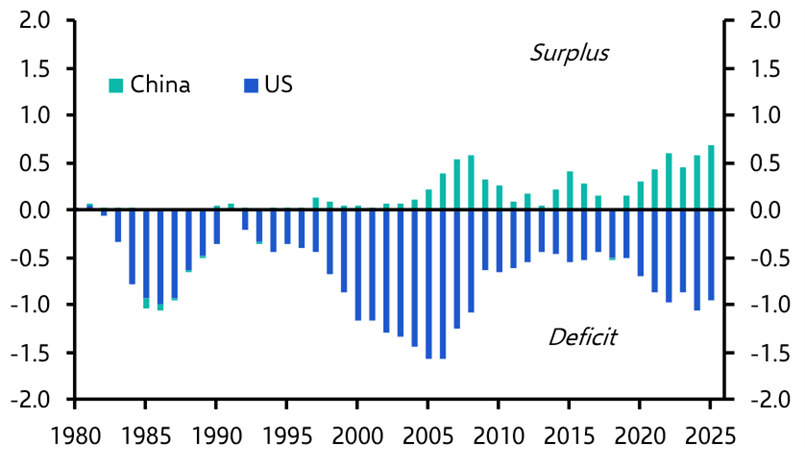

For all the noise around tariffs, the US continues to run a large current account deficit. At the same time, China continues to run large surpluses. (See Chart 2.)

|

Chart 2: Current Account Balances (% of World GDP) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

That should not come as a surprise – tariffs were never likely to alter the wider trade balances.

China’s surplus reflects chronically weak domestic consumption and exceptionally high savings, channelled into investment and export capacity. America’s deficit reflects the opposite: strong consumption, low savings and large fiscal deficits. These imbalances reflect structural macroeconomic fundamentals that cannot be solved through the imposition of tariffs.

Indeed, solving them would require precisely the kind of international policy coordination that is currently absent. The US would need credible fiscal consolidation. China would need a sustained shift toward household consumption, lower savings and a stronger social safety net. Currencies would also need to adjust, with China in particular allowing a significant appreciation of its real exchange rate. None of this is remotely on the agenda.

Instead, geopolitics is reinforcing the imbalances. China’s emphasis on self-sufficiency – driven in part by a sense of growing strategic competition with the US – pushes resources towards building the supply-side rather than strengthening household consumption. That sustains excess supply and export dependence. In turn, rising Chinese surpluses intensify the political backlash abroad. It is a negative feedback loop: geopolitics worsens imbalances, and imbalances worsen geopolitical tensions.

Jaw-jaw better than war-war

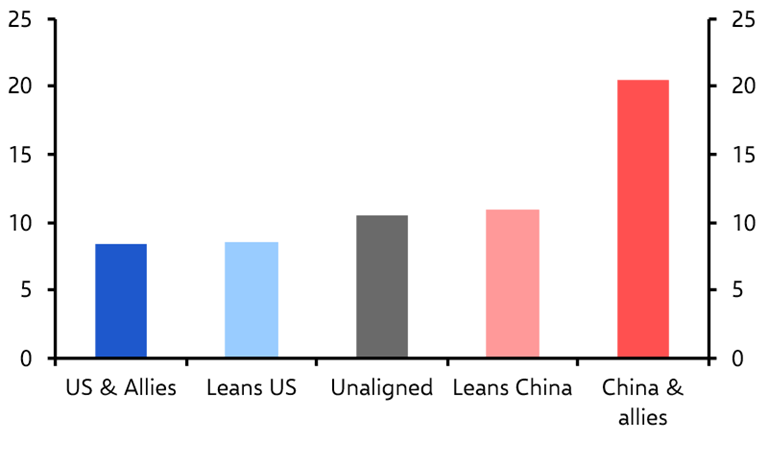

The upshot is that while both sides will proclaim this week’s summit a success, the practical outcomes are likely to be more limited. China is likely to agree to step up purchases of US products, but in reality may fall short of the targets that are set. The trade truce that was agreed between Xi and Trump last year is likely to be extended, but US tariffs on China (and its allies) are likely to remain high relative to other countries. (See Chart 3.)

|

Chart 3: Effective US Tariff Rate by Geopolitical Bloc |

|

|

|

Sources: US Census Bureau, Capital Economics |

Both sides may also agree to renewed dialogue on areas such as AI governance, but previous such efforts have also run into the sand at early stages.

Efforts to stabilise the US-China relationship are clearly positive – but investors should not confuse this as evidence that both sides are addressing the underlying forces that are pulling them apart.

In case you missed it

- The latest episode of our weekly podcast addresses the geoeconomic backdrop to this summit, as well as its potential deliverables.

- How much is the energy shock driving exports of Chinese green tech, and what will that mean for the green transition? Our China and Climate & Commodities economists will address this critical trend in a special online Drop-In briefing on Tuesday, 12th May. Register here.