They say sequels are rarely as compelling as the original. That is not the prevailing view in Brussels, where I spent last week and where discussion was dominated by "China Shock 2.0" – the prospect of a new wave of Chinese exports that could hollow out European industry. Yet there is little consensus about either the scale of the threat, or how best to respond to it.

This shock is different

China Shock 2.0 riffs on the original China shock of the early 2000s. Back then, China's emergence as a manufacturing powerhouse reshaped global trade and production. A series of influential academic papers published in the 2010s argued that rising imports from China had inflicted deeper and more geographically concentrated manufacturing job losses in the US than many economists had previously assumed.

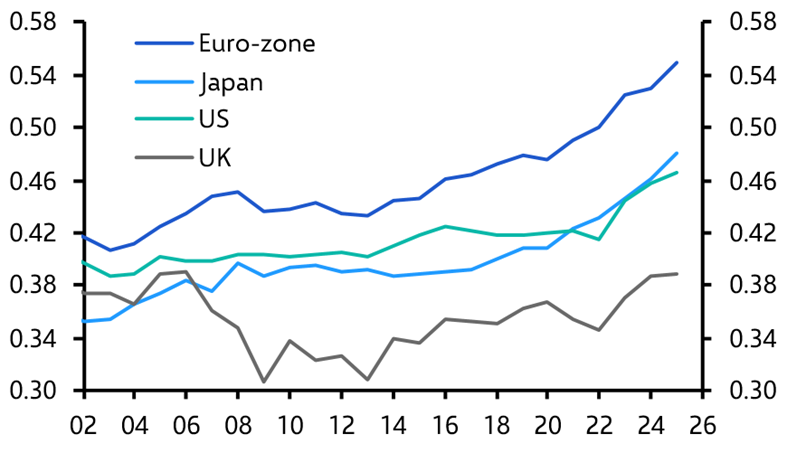

The current concerns are somewhat different. While the first shock was concentrated in lower-value manufacturing, China’s factories have moved up the value chain and are increasingly competing directly with advanced manufacturers, particularly those in the euro-zone. As Chart 1 shows, China’s export profile shows increasing similarities with Europe’s, to a much greater degree than it does with Japan, the US or the UK.

|

Chart 1: China Export Similarity Index (1 = maximum; 0 = minimum) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

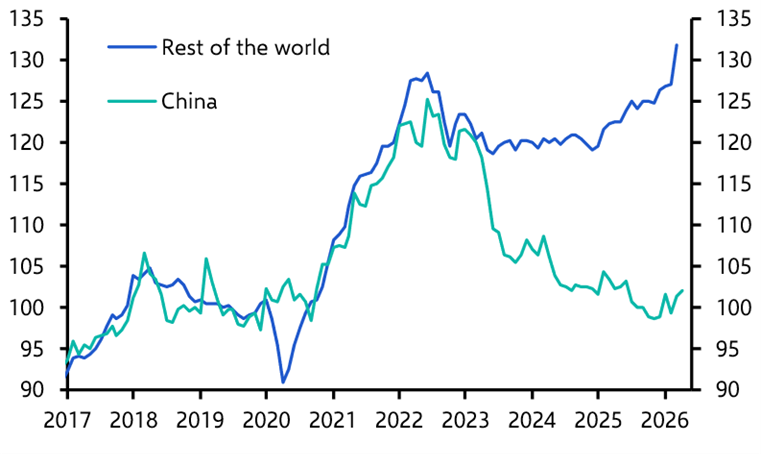

At the same time, Chinese exporters have been cutting prices aggressively. (See Chart 2.) As we have argued before, this reflects the characteristics of China's economic model: high savings, high investment, and a focus on building industrial capacity helped by extensive state support. The result is growing pressure on producers in the rest of the world, including Europe.

|

Chart 2: Goods Export Prices (US$, 2019 = 100) |

|

|

|

Sources: CEIC, CPB, Capital Economics |

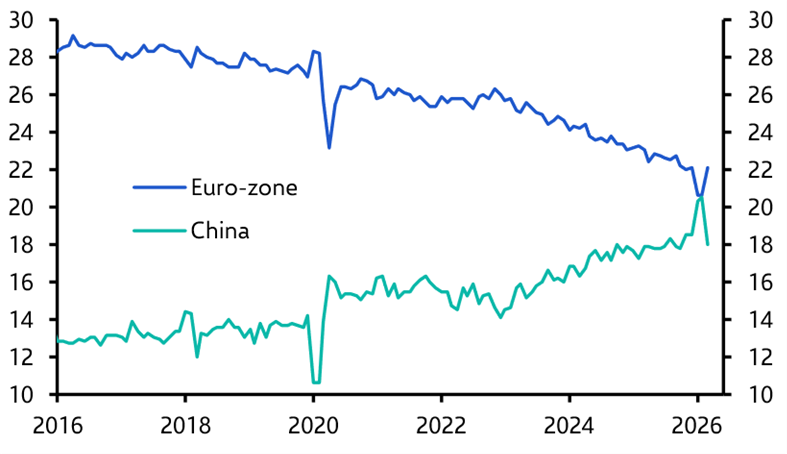

There is growing evidence of this squeeze. Exports from the euro-zone to China have fallen by around 30% since 2019, while Europe’s imports from China have risen by a similar amount over the same period. European firms are also losing ground against China in third markets. As Chart 3 shows, China's share of global exports has risen steadily over the past decade, while the euro-zone's share has declined by a similar amount. The loss of market share is broad-based, spanning sectors from machinery and industrial equipment to vehicles.

|

Chart 3: Share of Real Global Exports (%) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

A sense of perspective

There is much breathless commentary around the implications of China Shock 2.0. For a start, it often overlooks the benefits that lower-cost Chinese goods bring to consumers elsewhere, including in Europe. We estimate that export price deflation from China has reduced the level of headline CPI in advanced economies by 0.3-0.5%-pts since 2023. That is not a huge amount but in a world in which inflation is tending to overshoot rather than undershoot central bank targets, every little helps.

The economic impact on Europe may also be smaller than is sometimes assumed. Exposure varies considerably across countries. Economies with large manufacturing sectors are naturally more vulnerable than those where services dominate. Germany is therefore much more exposed than Spain or Ireland.

Overall, we estimate that increased competition from China may be reducing euro-zone GDP growth by up to 0.2%-pts a year. The impact is probably somewhat larger in Germany and much smaller in countries with less manufacturing exposure. But it is clear that Europe's economic challenges extend well beyond competition from China. Weak productivity growth, low rates of innovation, large “legacy” industries (traditional autos, chemicals etc), demographic headwinds and expensive welfare states are arguably more important constraints on long-term growth.

Cause for concern

Even so, there are reasons for concern. First, slow-growing economies have less room to absorb additional headwinds. The China shock may not explain Europe's broader economic malaise but, given that trend GDP growth is already less than 1% a year, every extra drag risks turning a problem of low growth into one of outright stagnation.

Second, the aggregate economy-wide effect can often mask a much larger impact on specific sectors. The vehicle industry is the most high-profile case. Chinese competition poses a particularly significant challenge to European carmakers. Moreover, the automotive sector accounts directly or indirectly for as much as 5% of the German economy (see here), and it carries economic and political importance that extends well beyond its contribution to output.

Third, and perhaps most importantly, growing dependence on Chinese producers raises geostrategic concerns that were largely absent during the first China shock. Back then, China specialised primarily in lower-value goods and was not widely viewed as a geopolitical rival. That has changed. To be clear, Europe does not yet view China as a strategic adversary in the same way that the US does. But the threat by Beijing to cut off supplies of rare earth minerals during last year’s trade war with the US also had implications for Europe, and has made clear China’s willingness to use economic leverage when it serves its interests.

This highlights the risks associated with dependence on China for critical inputs and technologies. In the automotive sector, for example, concerns extend beyond economics. Modern vehicles contain large numbers of sensors, cameras and connected technologies. As Chinese firms gain market share, questions about resilience, security and strategic dependence are becoming increasingly difficult for policymakers to ignore.

A muddled response

So how are policymakers likely to respond? This is the key question for investors and businesses. The answer, as is often the case in Europe, is "gradually and unevenly".

Part of their hesitation reflects uncertainty about the nature and scale of the challenge and part of it reflects concerns about retaliation. But it also reflects a difference in views between and within EU member states about how best to respond – partly reflecting their differing commercial interests. Moreover, many European policymakers are eager to retain what remains of the rules-based global trading system. Any response is therefore likely to be incremental and consistent with WTO principles.

Accordingly, we doubt that Europe will adopt the sort of broad-based tariffs used by the US anytime soon. A more likely outcome is a series of targeted measures focused on specific sectors. Consistent with this, the EU Industry Commissioner Stéphane Séjourné last month said the bloc should deploy import quotas and tariffs against China more widely than in the past, but also that the focus should shift from firm to sector-level responses, rather than to across-the-board measures.

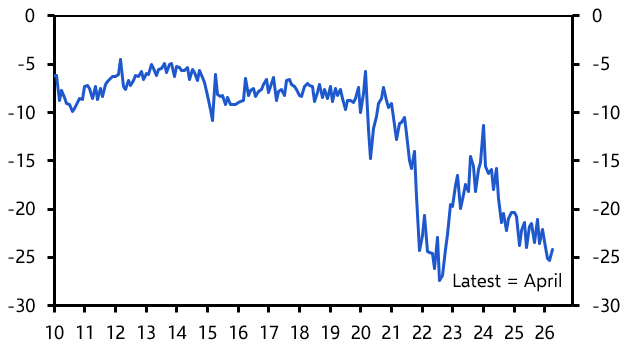

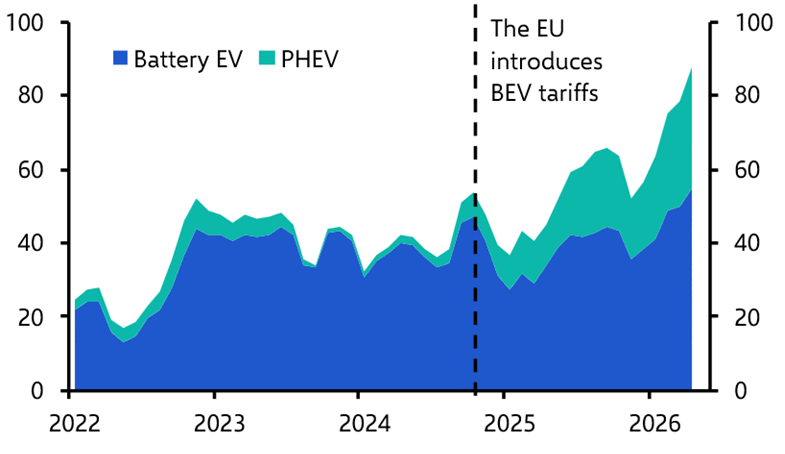

What all this amounts to in practice is still unclear but experience suggests that such policies are unlikely to reverse China's manufacturing gains or significantly slow the growth of its export sector. This is again illustrated by the recent experience of the auto sector. The introduction of EU tariffs on Chinese battery EVs in 2024 has not only failed to reduce China’s exports of those cars to Europe, it has also encouraged a shift towards plug-in hybrid vehicles that are not currently subject to such tariffs. (See Chart 4.)

|

Chart 4: China EV Exports to the EU (000s, 3m MA) |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

As a result, tensions between Brussels and Beijing are likely to intensify over the coming years. That is not to say that they will become as pronounced as those between the US and China. But the direction of travel over the past year is likely to continue and fits into a broader pattern of a steady deterioration in economic relations between China and the West, fuelled in part by China’s growing export dominance.

The full implications of China Shock 2.0 are not yet clear. But it is already apparent that they will shape the global economy in important ways over the rest of this decade. We are likely to see a return of more active industrial policy and the greater use of trade and investment restrictions. We will probably also see a greater focus by governments on policies that promote economic resilience rather than just economic efficiency. And we may even see long-established orthodoxies – such as a commitment to floating exchange rates – come under pressure. These themes will become increasingly important for investors, businesses and policymakers. We will explore them in more detail in a research series about China Shock 2.0 over the summer, followed by events in the autumn. Stay tuned.

In case you missed it

In a packed week of central bank meetings, the ECB is almost certainly going to raise interest rates – but the BoE is not yet ready to follow suit. Meanwhile, our US team now expects the Fed to hike this year.

We are holding an event in London on Thursday, in which we’ll set out our latest analysis of the macro and market effects of AI. There are still a couple of places left – register here.

Turmoil in Indonesian markets is about more than a recent run of soft economic data. Our Asia economists are briefing on whether the country is becoming uninvestable in an online Drop-In briefing on Tuesday at 1600 SGT / 0900 BST.