Europe Economics Weekly Wage growth falling, consumers gloomy, EC optimistic Data published this week confirmed that wage growth is slowing and consumers are downbeat. As a result, household spending growth is likely to remain subdued. Next week, we expect to learn that... 21st November 2025 · 7 mins read

Asia Economics Weekly BI independence concerns resurface, Philippines corruption The invitation extended to Indonesia’s finance minister this week to attend monetary policy meetings is not unheard of among global central banks, but the move will reinforce concerns that BI’s... 21st November 2025 · 6 mins read

UK Economics Rapid Response UK S&P Global Flash PMIs (Nov. 2025) November’s flash PMIs suggest that GDP growth is unlikely to snapback in Q4 and showed that services price pressures eased sharply. With what is set to be a big tax-raising Budget on Wednesday next... 21st November 2025 · 3 mins read

Europe Rapid Response Euro-zone Flash PMIs (November 2025) November’s flash PMI for the euro-zone was little changed from the reading in October and suggests that the economy has continued to expand only slowly in the fourth quarter, while inflationary... 21st November 2025 · 2 mins read

UK Economics Rapid Response UK Public Finances & Retail Sales (Oct. 2025) The last major economic releases before the Budget next Wednesday paint a pretty grim picture with the government borrowing more than expected in October and retail sales falling sharply at the start... 21st November 2025 · 3 mins read

Middle East & North Africa Chart Pack Middle East & North Africa Chart Pack (Nov. '25) Our Middle East & North Africa Chart Pack has been updated with our latest forecasts and calls to reflect key developments across the region. We expect the Middle East and North Africa to record very... 20th November 2025 · 1 min read

Europe Economics Focus Has France’s RN turned moderate? As it has dropped plans for “Frexit”, scaled back its tax and spending promises and made overtures to business, the RN is worrying investors less than it did in the past. However, it is no more likely... 20th November 2025 · 16 mins read

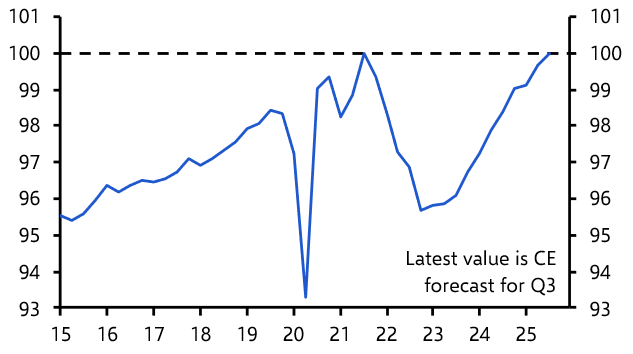

Latin America Chart Pack Latin America Chart Pack (Nov. 2025) Our Latin America Economics Chart Pack has been updated with the latest data and our analysis of recent developments. Aggregate Latin American growth slowed in Q3 and we doubt that there will be a... 20th November 2025 · 1 min read

Emerging Europe Economics Update Thinking through a potential end to the war in Ukraine Media reports suggest that the US and Russia are drafting a peace plan to end the war in Ukraine, seemingly on terms favourable to Russia. Were this to materialise, a lack of sufficient security... 20th November 2025 · 6 mins read

Emerging Europe Chart Pack Emerging Europe Chart Pack (Nov. 2025) Our Emerging Europe Chart Pack has been updated with the latest data and our analysis of recent developments. The Q3 GDP data out of Emerging Europe confirmed a growing divergence in the region, with... 19th November 2025 · 1 min read

Emerging Markets Economics Chart Pack Emerging Markets Chart Pack (November 2025) Our Emerging Markets Chart Pack has been updated with the latest data and our analysis of recent developments. EM growth held up well in Q3, although headwinds from fiscal tightening, softer labour... 19th November 2025 · 1 min read

Africa Economics Update South Africa’s economy lost momentum in Q3 The latest activity data suggest that South Africa’s GDP growth slowed a touch in Q3, to around 0.5% q/q, and we expect it to remain around this rate over the coming quarters, helped by improved terms... 19th November 2025 · 3 mins read

Asia Economics Update Taiwan: why aren’t consumers joining the party? Taiwan’s economy is booming and this has been driven almost entirely by exports, whereas domestic demand, and especially consumer spending, has been sluggish. That’s because faster wage increases in... 19th November 2025 · 4 mins read

Australia & New Zealand Economics Update RBNZ: One last cut for the road We expect the Reserve Bank of New Zealand to close out its easing cycle with a 25bp cut at its meeting ending on 26th November. Our sense is that the Bank will want to take out a final bit of... 19th November 2025 · 6 mins read

Latin America Rapid Response Colombia GDP (Q3 2025) The stronger-than-expected 1.2% q/q expansion in Colombia’s GDP in Q3 reflects continued strength in domestic demand and adds to reasons to expect the central bank to hold off resuming its easing... 18th November 2025 · 2 mins read