This Weekly Roundup highlights the growing challenge facing central bankers, what the UAE's exit means for OPEC, how long Iran could hold out, why China's debt pile keeps on growing, why AI jobs panic is misplaced and more.

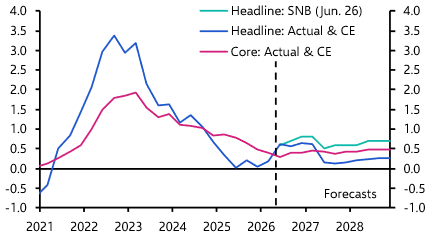

1.

We think markets are overpricing the extent of policy tightening, but each day that the Strait of Hormuz remains closed raises the likelihood of more adverse macro outcomes. We still expect the Fed to remain on hold, with the Bank of England also on the sidelines – albeit with less conviction. In contrast, we see the ECB hiking in June, and possibly again. Next is the RBA, which we expect to raise rates on Tuesday. Watch our latest central bank briefing and explore our Central Bank Hub.

2.

We flagged the risk of the UAE leaving OPEC in our 2025 anniversary report. It’s not the group’s death knell, but it does mark a further erosion of its influence over global oil markets. With the Strait of Hormuz closed, the news matters little for now. Once flows resume, it could mean more volatility and, on balance, lower prices.

3.

It’s one of the most frequent questions we’re being asked: how long can Iran hold out? The rial is in sharp decline, oil exports are down by around 75% and usable forex reserves may cover just three months of imports. Even so, past episodes suggest the regime could prove more resilient to military pressure than these strains alone suggest.

4.

The argument runs as follows: AI isn’t like past technologies; both knowledge and manual work are at risk, and mass unemployment will follow. But this misses the nuance. AI will reshape labour markets, not destroy them, and even severe disruption could leave people better off if gains are redistributed effectively. Read the report and register for our latest Drop-In briefing on this technology’s transformative potential.

5.

Overcapacity in China may be easing in a few sectors, but remains a system-wide problem. One byproduct is a growing trade surplus – now the largest of any country since the Second World War – as Chinese firms continue to gain global market share. These trends point to deeper flaws in China’s growth model, which is reflected in a debt burden that has now pushed above 300% of GDP.

6.

Despite persistent noise around inflation and central banks, the S&P 500 pushed to fresh record highs this week. It’s a recovery we called earlier in the Middle East conflict – and one we think can last for now, though it is driven by giddy expectations for a small group of chip firms to keep delivering on earnings.