Capital Daily We think the rally in the S&P 500 has a lot further to run Judging by the latest rally in some ‘big-tech’ sectors, renewed hype around Artificial Intelligence (AI) seems to explain why the S&P 500 has just racked up a new record high despite a recent rebound... 22nd January 2024 · 4 mins read

FX Markets Weekly Wrap Dollar grinds higher alongside rising equities and UST yields The US dollar’s rebound has gained momentum this week amid hawkish rhetoric from Fed officials and more evidence out of the US – notably retail sales and jobless claims – of continued resilience in... 19th January 2024 · 5 mins read

Capital Daily US and UK equities are more alike than it seems US large cap equities have vastly outperformed UK ones over the past year or so, but that is skewed by the performance of the biggest names on both sides of the Atlantic. Indeed, there is little... 19th January 2024 · 4 mins read

Asset Allocation Update The impact of AI on non-US stock markets While we think that enthusiasm around Artificial Intelligence (AI) will mean that equities in the US keep outperforming this year, we see scope for equities in the rest of the world to fare quite well... 19th January 2024 · 4 mins read

Global Markets Update We don’t expect China’s markets to stay under pressure for long We project decent near-term gains in China’s equities, think long-dated CGB yields will finish the year around their current levels, and expect the renminbi to rally against the US dollar. In view of... 19th January 2024 · 4 mins read

Capital Daily Rebound in Gilt yields and sterling may not last Although Gilt yields remain elevated and sterling resilient, we expect both to fall over the course of 2024 as disinflationary pressures build in the UK. 18th January 2024 · 4 mins read

Australia & New Zealand Chart Pack Australia & New Zealand Chart Pack (Jan. 2024) Our Australia and New Zealand Chart Pack has been updated with the latest data and our analysis of recent developments. Central banks in both Australia and New Zealand are likely to remain in “wait... 18th January 2024 · 1 min read

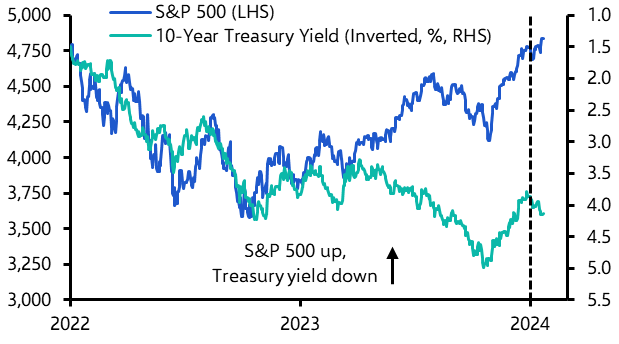

Global Markets Focus Why we expect the S&P 500 to soar in 2024 This Global Markets Focus explains why we expect the S&P 500 to soar in 2024, in contrast to those who anticipate a much tougher year for the index after a banner 2023. In view of the wider interest... 17th January 2024 · 16 mins read

Capital Daily China’s faltering economy need not mean a weaker renminbi We still forecast the renminbi to make ground against the US dollar by the end of this year, despite the seemingly stiff headwinds it faces. 17th January 2024 · 5 mins read

Japan Chart Pack Japan Chart Pack (Jan. 2024) Our Japan Chart Pack has been updated with the latest data and our analysis of recent developments. We expect GDP growth to slow to a crawl this year, weighed down by weak consumption growth and... 17th January 2024 · 1 min read

Capital Daily The hawks are ruling 2024 so far… but not really A hawkish mood has prevailed in markets this year, and comments from the Fed’s Waller today seemed to add fuel to that fire, at least initially. But given how aggressively rate cuts were priced in... 16th January 2024 · 4 mins read

FX Markets Update We think sterling has further to fall against the US dollar While sterling has outperformed other G10 currencies amid the dollar sell-off over the past couple of months, we expect it to reverse its gains against the greenback as short-term Gilt yields edge... 16th January 2024 · 2 mins read

Capital Daily We expect yield curves to normalise this year Government bond yield curves in the US, Germany, and the UK seem to be once again on the path towards “normalisation”, or “disinversion”, as short-term yields are close to breaking below long-term... 15th January 2024 · 4 mins read

Event ANZ Drop-In: Australia Q4 CPI and the case for an early RBA cut 31st January 2024, 3:00AM GMT There’s a popular view that the RBA won’t start cutting interest rates until later in the second half of this year.

Event Drop-In: What to expect from financial markets in 2024 24th January 2024, 3:00PM GMT Will US equities continue to lead the pack in 2024? How will monetary policymaking affect the level of yields? What will this mean for FX markets?

Capital Daily We think UK equities will turn the corner in 2024 In contrast to 2023, we expect a strong showing from UK equities this year, helped by a weaker pound and enthusiasm around AI technology. 12th January 2024 · 5 mins read