Filtered by Topic: Monetary Policy Region: G10 Use setting G10 Use setting Monetary Policy

Bank of England to keep interest rates unchanged at 5.25% but retain its hawkish bias It won’t risk fuelling bets on earlier rate cuts by watering down its forward guidance We expect Bank Rate to be cut later, but by more than most expect With the Bank …

7th December 2023

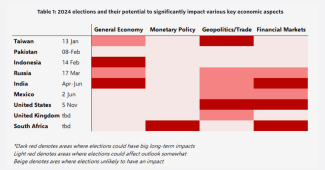

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

Even though we expect the economy to be weaker than the consensus in 2024, we think that lingering constraints on domestic supply will prevent wage growth and services CPI inflation from falling quite as fast as is widely expected. As a result, we think …

We think that sovereign bond yields in most major economies will generally reach their troughs around the same time over the next year or so. But with the Bank of Japan seemingly set to buck the trend once again, yields there may be an exception. The …

The Bank of Canada is clinging on to the idea that restrictive policy is still needed to get inflation back to 2%. Nonetheless, with core inflation pressures muted, GDP and house prices falling, and labour market conditions loosening rapidly, it won’t be …

6th December 2023

Overview – As core inflation is on track to return to the 2% target by the middle of next year, we expect the Fed to cut interest rates by 25bp at every meeting next year from March onwards, with rates eventually falling to between 3.00% and 3.25% in …

Bank maintains tightening bias, but next move likely to be a cut The policy statement from the Bank of Canada was a bit more hawkish than we expected, with the Bank reiterating that it is still concerned about the outlook for inflation and “remains …

Officials not yet willing to fully endorse rate cut bets; tightening bias could be retained New SEP should confirm rates are at the peak but significant downgrades unlikely We expect the first rate cut in March and 175bp of easing in total next year With …

Overview – With higher interest rates taking longer to percolate through the economy, we now think the recession will be shallower and GDP growth will stay weak throughout all of 2024. It’s a softer landing for the economy, but the runway is longer. And …

5th December 2023

Given the high bar for further rate hikes, we’re more confident than ever that the Reserve Bank of Australia is done tightening policy. That said, there is a good chance that the cash rate will remain at its cyclical peak for longer than we currently …

RBA is done hiking rates Although the RBA won’t tighten policy any further, there is a good chance that the Bank will hold the cash rate at its current peak for longer than we anticipate. The RBA’s decision to leave rates unchanged at its meeting today …

Overview – Following a strong 2023, GDP growth is set to slow towards potential next year and the labour market will tread water for now. However, with the virtuous cycle between consumer prices and inflation set to gain momentum, we expect the Bank …

4th December 2023

The prospect of earlier interest rate cuts in the US and the euro-zone has led to a sharp fall in US and euro-zone government bond yields this week. 10-year US Treasury and German Bund yields have fallen by 15 and 22 basis points (bps), to 4.32% and 2.43% …

1st December 2023

Consumption falling but labour market tightening The October activity data were a mixed bag. While industrial production rose by 1% m/m, firms’ forecasts for the next couple of months were weak and point to a stagnation in output across Q4 following …

GDP contracted in the third quarter and there are downside risks to the outlook. As house prices are falling again, household debt is elevated and high interest rates are still feeding through, the key risk is that the mild recession we forecast could …

30th November 2023

The key indicators that have usually convinced the Bank of England to cut interest rates suggest the first cut could come in Q1 2024. That said, rates have risen to a lower peak than most models suggest, which implies they need to stay higher for longer …

Economic growth and inflation both weaker than Bank expected Bank likely to tone down, or even drop, its tightening bias Policy rate to be cut by much more than markets expect in 2024 The second consecutive month of muted core inflation pressures in …

29th November 2023

Bullock has continued to sound hawkish, leaving the door open for another rate hike Trimmed mean inflation still stubbornly high, but set to slow further Bank’s next move will be a rate cut, perhaps as early as Q2 next year We expect the Reserve Bank …

This page has been updated with additional analysis since first publication. RBNZ will cut rates in the second half of next year While the RBNZ signaled that it could hike rates further, we still think that the tightening cycle is now over and that the …

The rebound in the activity data in November has convinced investors that the first interest rate cut will happen later, in August next year instead of June. Our view that core inflation will ease only slowly explains why we think interest rates won’t be …

28th November 2023

The recent period of high inflation in Japan has kick-started a virtuous cycle between wages and prices. If inflation expectations remain elevated and structural forces push up the neutral rate of interest over the coming years, monetary policy will …

27th November 2023

The S&P Global PMIs have provided misleading signals about the strength of activity in the US and Europe this year. But, for what it’s worth, the flash surveys for November suggest that DMs are ending 2023 on a weak note, with activity stagnating or …

24th November 2023

It would be a stretch to say the government showed fiscal restraint in the Fall Economic Statement , but the announcement of only a few billion dollars in extra spending measures means that Finance Minister Chrystia Freeland did not pour much more fuel on …

Surveys point to renewed slowdown in inflation Following a rather hawkish speech by Reserve Bank of Australia Michele Bullock, the financial markets now price in a 60% chance of another 25bp rate hike at the Bank’s February’s meeting, up from 40% before …

A year of the most aggressive monetary tightening in a generation is expected to end with the major DM banks leaving rates on hold at their December meetings. Following our briefings on the world in 2024 , our senior economists will be held a special …

23rd November 2023

Fed offers something for everyone There is something for everyone in the minutes of the Fed’s early November policy meeting. The FOMC still just about maintained a tightening bias, but the overwhelming impression is that officials thought rates had …

21st November 2023

The economy’s third-quarter strength was not the start of a renewed acceleration and we continue to expect GDP growth to weaken. Regardless, resilient economic growth has not prevented a continued easing in wage and price inflation, and we still think the …

While the US economy considerably outperformed its DM peers in Q3, we think that all advanced economies will suffer a weak Q4. High interest rates are weighing on credit growth, and a further rise in debt servicing costs in the coming quarters is likely …

17th November 2023

The Bank of Canada’s latest Summary of Deliberations was more hawkish than most probably expected, with some members of the Governing Council still seemingly arguing for further rate hikes. That said, the weak GDP data released since the Bank’s last …

10th November 2023

Edging away from ultra-loose policy The “Summary of Opinions” from last week’s Bank of Japan Monetary Policy Meeting released yesterday show a Policy Board increasingly confident that the long-term 2% target is coming into sight. The likelihood of …

One and done for the RBA The main event this week was the RBA delivering a widely-anticipated 25bp rate hike at its meeting on Tuesday. Our assessment is that the increase in the cash rate is essentially something of an insurance policy, aimed at ensuring …

Shortly after the release of the October CPI report, our US Economics team held a client briefing all about the October report and the inflation and growth outlooks and how they’ll shape Fed policy. They answered client questions and addressed key issues, …

9th November 2023

GDP growth appears to have all but stalled in Q3 but that was after a very strong first half. There are mounting signs that a virtuous cycle is forming between wages and prices. This is making the Bank of Japan increasingly confident that it can steer …

Bank lending data from the major advanced economies confirmed that lending was very subdued in September and the latest bank lending surveys show that banks have since tightened their lending criteria further. With demand for loans also falling, the drag …

The recent weakening in employment, easing in wage growth and signs that households are saving more and spending less have provided more confidence that higher interest rates are working. But we think that the restraints on UK labour supply and sticky …

8th November 2023

As had been widely expected, the RBA handed down a 25bp rate hike at its meeting today. With the cash rate now at 4.35%, we believe the Bank’s tightening cycle is over. If we’re right that the Australian economy will soon take a turn for the worse, rate …

7th November 2023

RBA’s next move will be down With today’s widely anticipated rate rise now behind us, we believe the RBA’s tightening cycle is at an end. The RBA’s decision to lift its cash rate by 25bp at today’s meeting came as a surprise to few. Indeed, 35 out of 39 …

Group Chief Economist Neil Shearing is back to discuss what the recent data say about the global economic outlook – including October US payrolls and China PMIs – and what to expect from the Fed, ECB and Bank of England following their decisions to keep …

3rd November 2023

There is now mounting evidence that the economy is set for a renewed slowdown in the fourth quarter and that inflationary pressures from the labour market continue to ease. Although markets have already moved to price out any real chance of further rate …

We can understand if the phase “the lady doth protest too much” sprang to mind when listening to the Bank of England after it left interest rates at 5.25% for the second meeting in a row on Thursday. Indeed, the Old Lady of Threadneedle Street stressed so …

Threat of yen intervention remains As we had expected, the Bank of Japan retained its 1% cap for 10-year yields at this week’s meeting . However, by downgrading that cap to a “reference” and by stopping its daily fixed-rate operations offering to buy an …

We’ll be discussing the latest Fed, ECB and Bank of England policy decisions in a 20-minute Drop-In webinar at 3pm GMT today. (Register here .) The Bank’s decision to leave interest rates at 5.25% for the second time in a row and to double down on the …

2nd November 2023

Bank doubles-down on rates staying high for long The Bank’s decision to leave interest rates at 5.25% for the second time in a row and the doubling down on the message that rates cuts are a long way away supports our view that Bank Rate will stay at 5.25% …

By leaving rates unchanged while continuing to flag the possibility of further tightening to come, the Fed indicated today that it remains in ‘wait and see’ mode. But Chair Jerome Powell appeared to strike a more dovish tone in his press conference and we …

1st November 2023

Fed’s tightening bias likely to be dropped soon By leaving rates unchanged while continuing to flag the possibility of further tightening to come, the Fed indicated today that it remains in ‘wait and see’ mode. But we suspect the data over the coming …