Fresh conflict in the Middle East has understandably consumed the global macro news cycle – after all, a sharp and sustained rise in energy prices risks an inflationary resurgence which could, in the very least, force central banks to abandon any plans they may have had to ease policy.

But while the war with Iran is immediate and consuming, another critical story will develop in Beijing from Thursday. The start of this year’s National People’s Congress should include, not only policy goals for the coming year, but also key priorities from the 15th Five-Year Plan, a development blueprint to run through 2030. After many false dawns, those priorities could determine how serious China’s leadership is about finally confronting its central – and worsening – economic problem: a persistent imbalance between supply and demand.

A question of balance

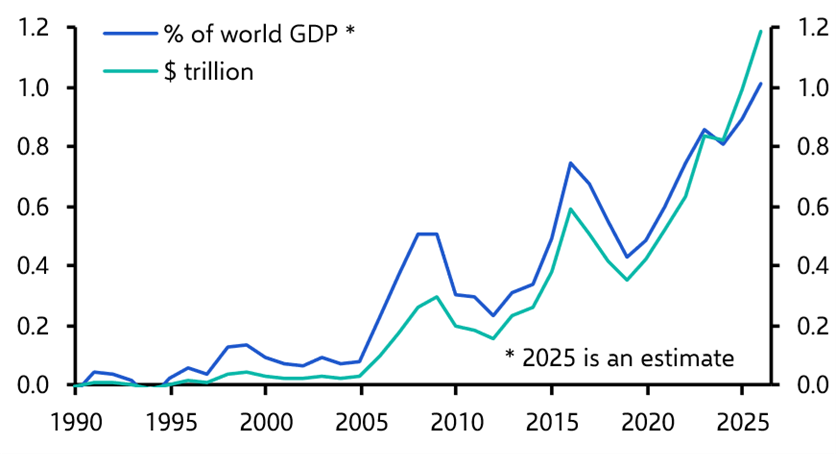

This imbalance is most visible in China’s trade surplus, which hit a stunning $1.2 trillion in 2025. (See Chart 1.) This surplus is not evidence, as Donald Trump has argued when justifying his tariff policy, that China holds the upper hand in its trade relationship with the US. Gains from trade are not measured by surpluses and deficits. China’s extraordinary ability to supply goods at low prices – and its willingness to recycle surpluses into dollar-denominated assets – has been a boon for US consumers. The flip side of overcapacity in China is an excess of consumption over production in America.

|

Chart 1: China’s Trade Surplus |

|

|

|

Sources: LSEG Data & Analytics, Capital Economics |

But while Trump’s analysis misses the mark there are as I’ve noted before valid reasons to be concerned about the US deficit – and by China’s surplus. The imbalance can be narrowed in two ways: reduced US imports through protectionist measures or weaker aggregate demand, or stronger Chinese domestic demand, which would absorb a greater amount of domestic production and thus compress China’s surplus.

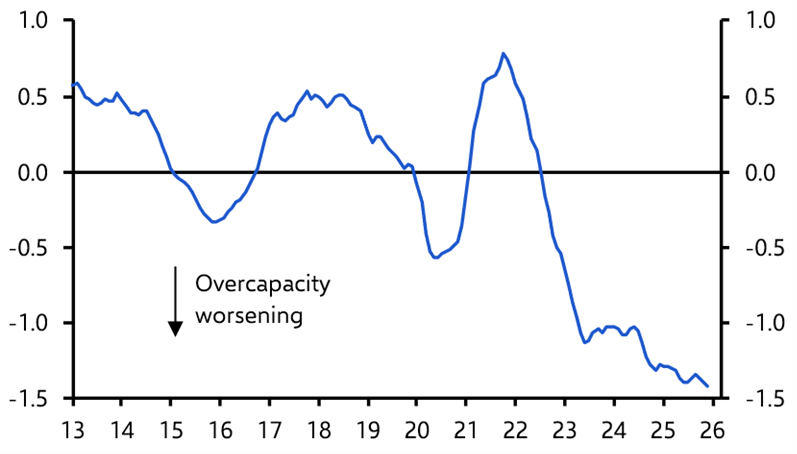

Our new Overcapacity Index lays bare the scale of this challenge and the urgency in meeting it. At an aggregate level, the Index suggests that excess capacity has reached its worst level on record, surpassing the trough during the last round of supply-side reforms in 2015. (See Chart 2.)

|

Chart 2: CE China Overcapacity Index (12m rolling average, Z Score) |

|

|

|

Sources: CEIC, Capital Economics. |

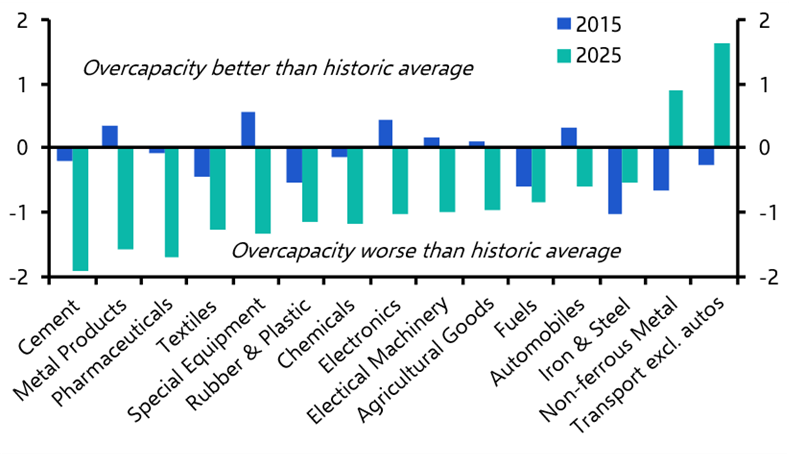

What’s more, while the problem is often framed around specific sectors like automobiles and solar panels, the sectoral breakdown of our index shows that overcapacity has worsened across almost all parts of the manufacturing sector. Overcapacity is now worse than its historic average in 27 of the 29 industrial sectors that we track. (See Chart 3.)

|

Chart 3: CE China Overcapacity Index (12m rolling average, Z Score) |

|

|

|

Sources: CEIC, Capital Economics |

The official response so far – including the so-called “anti-involution” campaign – echoes the supply-side reforms of a decade ago. Tighter pricing discipline, higher product standards, production caps and encouraging industrial consolidation may help at the margin, but these are unlikely to resolve overcapacity. Bringing supply and demand into alignment primarily by restraining output risks weaker growth and job losses, giving local officials strong incentives to move cautiously given the primacy of maintaining social stability.

An alternative solution would be large-scale macro stimulus, allowing authorities to withdraw support from inefficient firms. Yet Beijing appears reluctant, wary of further debt accumulation and sceptical about the durability of such support.

Competing priorities

Ultimately, a lasting fix requires a reflation of domestic demand and a rebalancing away from investment toward consumption. Recent policy meetings suggest that this latest Five-Year Plan will signal progress on this front. The Communist Party’s Fourth Plenum, which concluded in October and set the priorities for the Plan, indicated that for the first time an explicit target could be set to raise the share of GDP accounted for by consumption.

But this target would appear to be subordinate to – and in direct tension with – other priorities.

The primary goals set by the Fourth Plenum are "technological self-reliance” and “economic security”, both of which require state-led investment and a continued focus on the supply-side of the economy, rather than demand-side policies to stimulate consumption.

What’s more, to the extent that the Five-Year Plan does pave the way for a shift away from investment and towards consumption, any transition will be gradual and could initially worsen excess capacity: investment is goods-intensive, whereas nearly half of household spending falls on services. Accordingly, any shift in the drivers of demand could worsen the imbalance between supply and demand in the goods sector.

A concerted attempt at rebalancing would also require a stronger currency alongside efforts to stimulate domestic consumption as part of a broader plan to increase domestic demand. But as things stand there appears to be little appetite for a large appreciation of the renminbi in trade-weighted terms.

No quick fix

China’s overcapacity problem is therefore unlikely to be resolved quickly. Domestically, sustained excess supply will create persistent deflationary pressure, complicating debt dynamics and prompting the People’s Bank of China to loosen policy further. We expect additional cuts to policy interest rates, which in turn should feed through to lower bond yields – we think the 10-year government bond yield will drift below 1.5% over the next year or so from around 1.8% now.

For the rest of the world, and the US in particular, the implication is that China’s large trade surplus will persist. Indeed, while the consensus expects it to narrow over 2026-27, we think it is more likely to widen.

This imbalance will therefore remain an acute source of tension between China and the rest of the world, and the US in particular.

The war in the Middle East will continue to command attention, but some focus will shift to President Trump’s visit to Beijing scheduled for the end of this month. The signals from both sides suggest the priority is to maintain the recent stabilisation in the bilateral relationship. This sense of stability has been helped by the fact that China has been a relative “winner” of the Supreme Court’s recent ruling on the illegality of some of Trump’s tariffs.

But the structural tensions – not least around trade – remain firmly in place. The direction of travel over the next six months or so is likely to be towards a further thawing in relations – but beyond this there’s little reason to expect a fundamental reset in US-China relations.

Related content

Read our NPC preview here and this 2024 analysis on the lack of progress in rebalancing. Our most recent China Activity Proxy reading highlights the persistent gap between the government’s growth story and our lower estimate.

China’s energy relationship with Iran has made it a focus of the current conflict in the Middle East. This analysis shows how the depth of that relationship has been overstated, but also why Beijing has a vested interest in keeping the Strait or Hormuz open. All of our key analysis on the conflict in the Middle East can be read here.