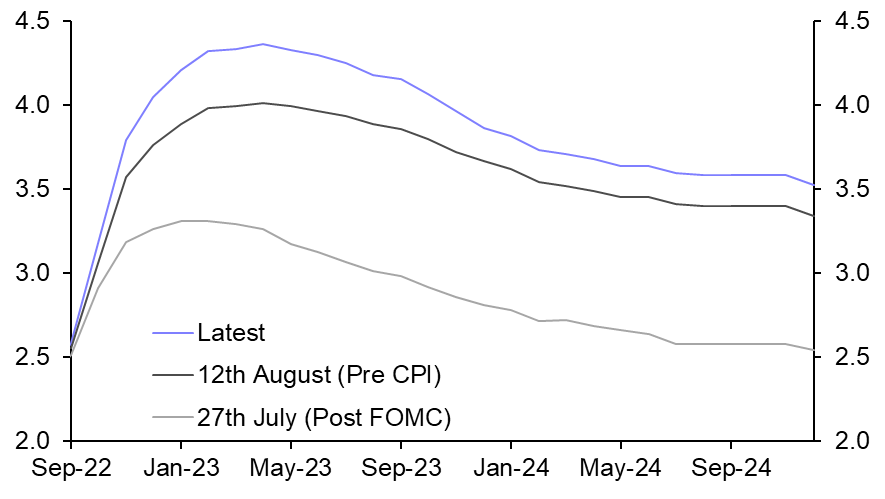

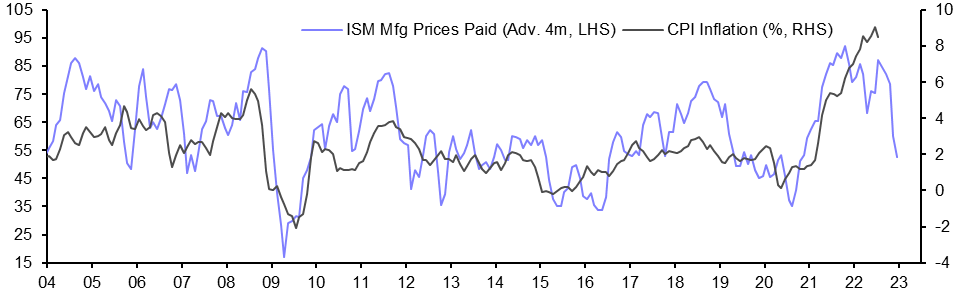

US Fed Watch Peak hawkishness to continue for a little longer The continued strength of core inflation points to another 75bp rate hike at next week’s Fed meeting and rates may now rise slightly higher than we previously thought. But the FOMC’s new projections... 14th September 2022 · 8 mins read

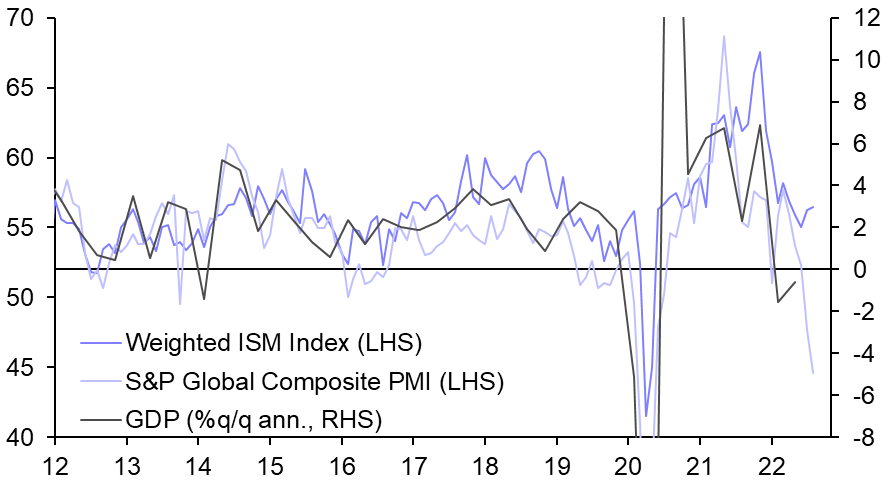

US Economics Update A closer look at the diverging activity surveys We think the S&P Global composite PMI’s prediction of an imminent plunge in GDP will prove well wide of the mark, with the latest hard data pointing to growth of 3% annualised in the third quarter. At... 8th September 2022 · 3 mins read

US Data Response ISM Manufacturing Index (Aug.) The stabilisation in the ISM manufacturing index at 52.8 in August, unchanged from July, provides some further reassurance that the economy is not yet sliding into recession. While the details suggest... 1st September 2022 · 2 mins read

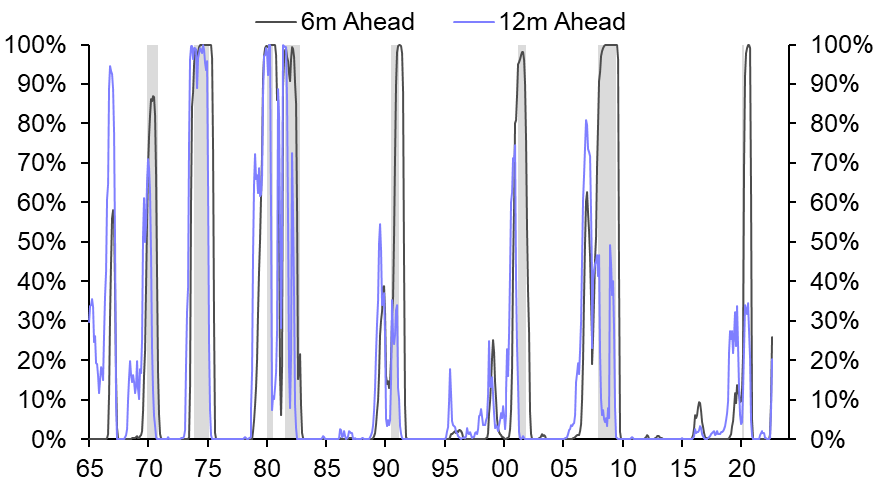

US Economics Update Recession Watch (Aug.) Our composite tracking models suggest that the chances of a recession within the next year have risen markedly. That said, the immediate risks still appear to be low, with the boost to real incomes... 31st August 2022 · 5 mins read

US Chart Pack Rebounding real incomes to support consumption After a year-long contraction in real disposable incomes, the sharp declines in energy prices over recent weeks are finally providing some relief. Alongside continued strong employment growth, we... 22nd August 2022 · 10 mins read

US Economics Weekly Better news for the Fed going into Jackson Hole With the rebound in activity growth in July coming against a backdrop of easing inflation, we still think the Fed will hike rates by a smaller 50bp next month. 19th August 2022 · 7 mins read

US Data Response Industrial Production (Jul.) The 0.6% m/m rise in industrial production in July was much stronger than we expected and provides another clear sign that the economy is still in expansionary territory. That said, the likely drag on... 16th August 2022 · 2 mins read

US Economics Update Is there really such thing as a ‘jobful’ recession? While history shows that recessions can begin even while employment is still rising, the current rate of payroll employment growth is far too strong to be consistent with an economic downturn. By the... 11th August 2022 · 4 mins read

US Data Response International Trade (June) The fall in the trade deficit to an eight-month low of $79.6bn in June, from $84.9bn, leaves net trade well placed to support a rebound in GDP in the third quarter. But with the surveys consistent... 4th August 2022 · 2 mins read

US Data Response ISM Manufacturing Index (Jul.) Although the ISM manufacturing index fell again in July, to 52.8 from 53.0, the rate of decline does at least appear to be slowing and, for now, it remains consistent with GDP growth of roughly 1.5%... 1st August 2022 · 2 mins read

US Data Response GDP (Q2) The 0.9% annualised fall in GDP in the second quarter is disappointing but doesn’t mean the economy is in recession. The decline was partly due to a huge drag from inventories, while most other... 28th July 2022 · 2 mins read

US Economics Update Recession Watch (Jul.) While the deterioration in the survey data and renewed inversion of the Treasury yield curve imply that the risks are rising, our composite models suggest that the economy is still more likely than... 27th July 2022 · 4 mins read

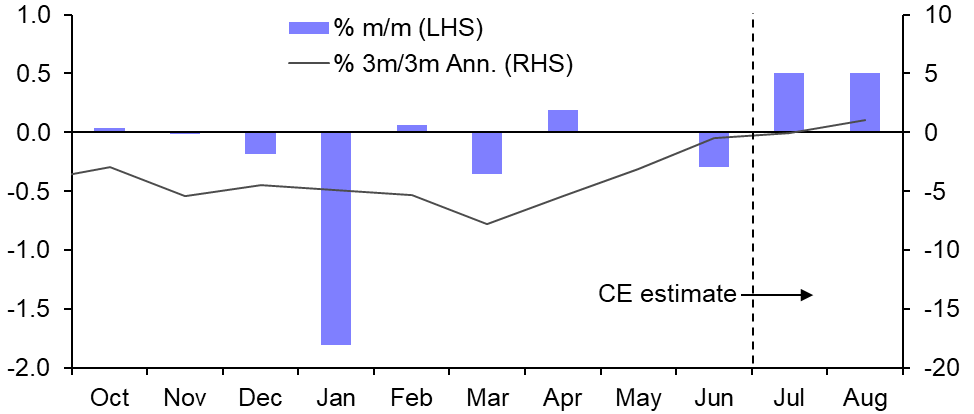

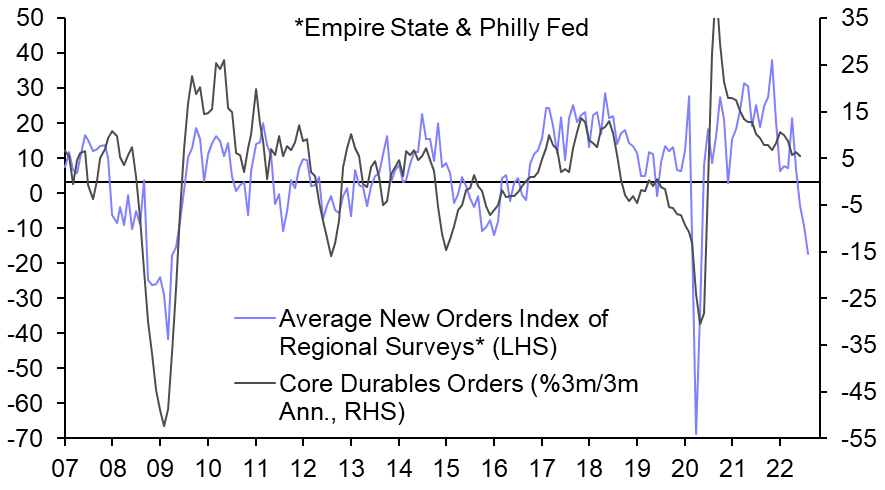

US Data Response Durable Goods (Jun.) The jump in durable goods orders in June mainly reflected a surge in defence aircraft orders. Private equipment investment growth still looks to have slowed in the second quarter, although the latest... 27th July 2022 · 2 mins read

US Chart Pack Economic growth to remain muted in H2 The incoming activity data now show clearer signs of weakness, particularly in the most interest-rate sensitive components of spending. But there are still few signs of that moderation morphing into a... 21st July 2022 · 8 mins read