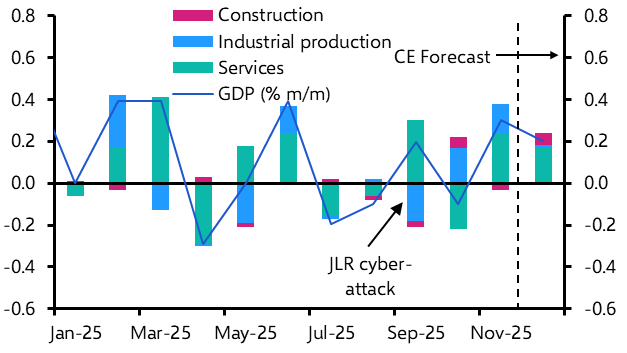

UK Economics Rapid Response UK GDP (Nov. 2025) The 0.3% m/m rebound in real GDP in November (consensus and CE forecast 0.1% m/m) suggests the economy is heading into 2026 with a bit more momentum than we thought. But with the economy still... 15th January 2026 · 3 mins read

UK Housing Market Update UK RICS Residential Market Survey (Dec. 2025) The continued weakness in buyer sentiment, the further rise in the supply of homes for sale and the softening in rental demand recorded by the RICS survey in December implies that the risks to our... 15th January 2026 · 3 mins read

Climate Economics Update A closer look at the UK’s renewable auction “success” The ~8GW of renewable generating capacity procured at the UK government’s latest energy auction could help to lift renewables’ share in the UK’s energy mix to over 70% by 2030, and underlines the UK’s... 14th January 2026 · 4 mins read

Emerging Europe Economics Focus Bulgaria’s slow euro-zone convergence to continue Bulgaria has become the latest but also the poorest member of the single currency area following its euro adoption at the start of the year. GDP per capita should continue to converge with Western... 14th January 2026 · 17 mins read

Emerging Europe Rapid Response Poland Interest Rate Announcement (Jan.) The decision by the National Bank of Poland to leave its policy rate on hold today, at 4.00%, is likely to mark a temporary pause in the easing cycle, and we expect two further 25bp cuts over the... 14th January 2026 · 2 mins read

Europe Economics Focus Pensions & public finances: not just a French problem Far from being only a French problem, pensions will be a growing fiscal headache in all the major euro-zone countries in the coming decade as populations age. In France and Italy, this will add to the... 14th January 2026 · 24 mins read

Europe Commercial Property Update High valuations challenge the Paris prime office market A weak overall office market in Paris has pushed investor demand to prime assets, leaving valuations highly stretched. Nevertheless, our relatively positive prime rental forecast means that Paris... 13th January 2026 · 3 mins read

UK Economics Update Get ready for a big fall in UK inflation to 2.0% We think April’s inflation data (released on 20th May) will reveal that, after spending almost five years above target, CPI inflation has finally fallen to 2.0%. This would be below the consensus... 12th January 2026 · 3 mins read

Europe Chart Pack Europe Chart Pack (January 2026) We expect euro-zone GDP to increase at a moderate pace this year and next. Germany’s fiscal stimulus is likely to be smaller, slower and less effective than many expect, while growth will be stronger... 12th January 2026 · 1 min read

Emerging Europe Economics Weekly Ukraine’s security, Venezuela spillovers, CPI data The US and Europe appeared to move closer to an agreement on providing security guarantees to post-war Ukraine this week, but Russia is unlikely to be on board with the terms of the proposed... 9th January 2026 · 7 mins read

UK Economics Weekly Public sector pay not an obstacle to further BoE rate cuts We expect the striking gap between public and private sector pay growth in October to narrow in the coming months. But even if political pressure on the government means public sector pay growth is... 9th January 2026 · 7 mins read

Europe Economics Weekly On EU relations with the Western Hemisphere We suspect that European governments will prioritise their relationship with the US over concerns about Greenland’s sovereignty, not least because they are more focused on Nato and Ukraine. Meanwhile... 9th January 2026 · 5 mins read

Commodities Weekly Greenland’s mineral potential; metal price mayhem Despite Greenland’s undoubted resource potential, the significant technical challenges and high costs associated operating on the island will surely limit the potential for sizeable production... 9th January 2026 · 4 mins read

Europe Rapid Response German Industrial Production (November) The rise in output in November confirmed that conditions in German industry improved towards the end of last year. But given the significant structural headwinds facing the sector, we doubt this is... 9th January 2026 · 2 mins read

Commodities Update 5 key questions on the “shadow fleet” The seizure of the Marinera oil tanker by the US has put the “shadow fleet” under the spotlight, with some estimates suggesting it now accounts for ~20% of global tanker capacity. While a concerted... 8th January 2026 · 4 mins read

Emerging Europe Rapid Response CEE Economic Sentiment Indicators (Dec. 2025) The European Commission’s Economic Sentiment Indicators for Central and Eastern Europe (CEE) suggest that regional GDP growth held steady at around 2.5% y/y in December, and we think that growth will... 8th January 2026 · 2 mins read