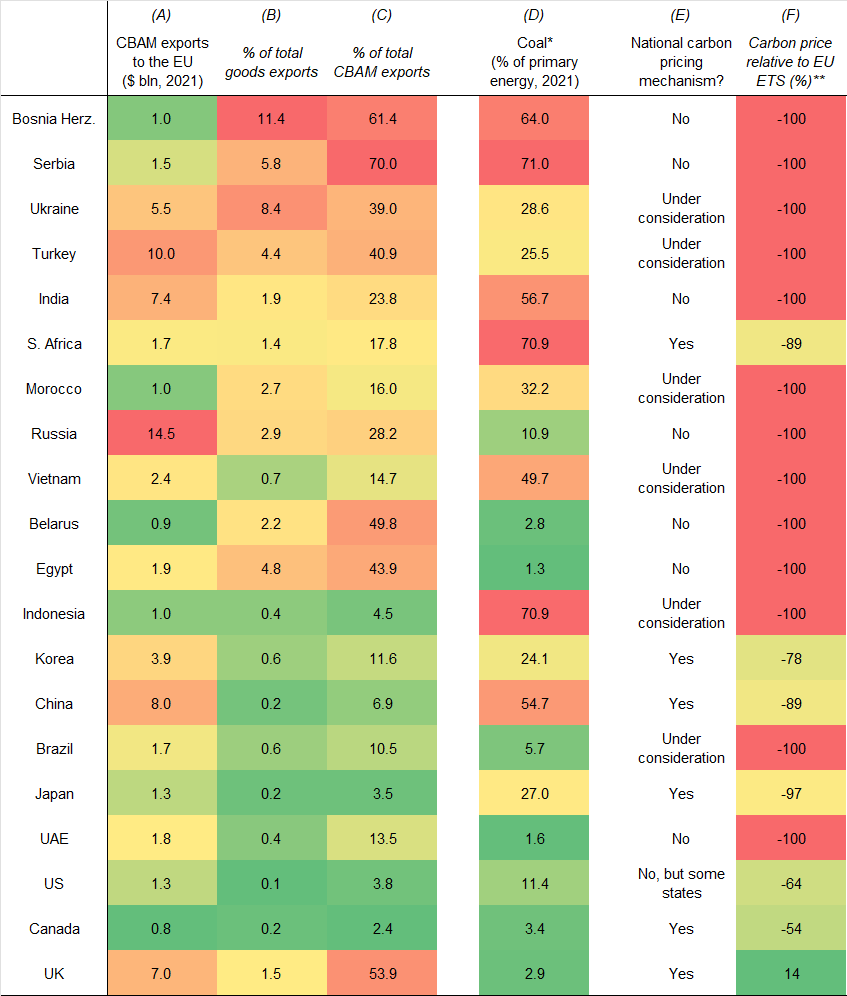

Climate Economics Update Assessing the knock-on impacts of the EU’s “CBAM” Following on from our recent background note on the EU’s Carbon Border Adjustment Mechanism (CBAM) and the signing off on the tool by EU Ministers over the weekend, this Update examines which... 20th December 2022 · 4 mins read

UK Commercial Property Chart Pack Surge in yields has further to run While we had expected the rise in risk-free rates and upcoming recession to boost yields, the speed at which they have increased has been surprising. All-property equivalent yields rose by a total of... 20th December 2022 · 8 mins read

Event The World in 2023 - What to Expect in Advanced and Emerging Economies 10th January 2023, 8:00AM GMT Chief Global Economist Jennifer McKeown and colleagues from across our macro services held a special briefing on what to expect from major DMs and EMs in 2023.

UK Housing Market Chart Pack Jump in interest rates takes its toll The return of inflation for the first time in the inflation-targeting era has led to the biggest jump in Bank Rate and mortgage rates since the late 1980s. The steady downward trend in mortgage rates... 19th December 2022 · 10 mins read

Europe Economic Outlook Recession will do little to dampen price pressures We think the euro-zone is now at the start of a recession, driven by high inflation, tightening financial conditions and weak external demand, and anticipate two quarters of contraction followed by a... 19th December 2022 · 2 mins read

Global Economic Outlook 2023 marked by recession and disinflation We continue to expect the world to slip into recession in 2023 as the effects of high inflation and rising interest rates are felt. Our forecasts are below the consensus across the board but... 19th December 2022 · 3 mins read

Europe Data Response EZ Hourly Labour Costs (Q3) Euro-zone wage growth has accelerated this year and we expect it to stay strong. In turn, this will contribute to core inflation remaining above 2% in 2023. 19th December 2022 · 3 mins read

Europe Data Response German Ifo Survey (Dec.) The further increase in the Ifo Business Climate Index in December and the general improvement in the surveys over the past two months suggests the outlook for the German economy has improved. But we... 19th December 2022 · 2 mins read

Europe Rapid Response German Ifo Business Climate Indicator (December) 19th December 2022 · 2 mins read

FX Markets Weekly Wrap ECB steals the show, but the dollar rebounds After a choppy few days in financial markets, the US dollar is ending the week a touch stronger against most other major currencies as risk sentiment has worsened sharply in the wake of the latest... 16th December 2022 · 10 mins read

Capital Daily We think that the BTP/ Bund spread will widen a bit more After rising sharply after Thursday’s ECB meeting, we think the 10-year BTP/ Bund spread will widen a bit more in the coming months. But we don’t think that the recent divergence between 10-year... 16th December 2022 · 7 mins read

Emerging Europe Economics Weekly Hungary’s EU fund deal, further dovish tilt at the CNB? The EU’s approval of Hungary’s COVID-19 recovery plan this week is a welcome development for Hungary’s economy and financial markets, but it won’t immediately transform the near-term outlook. 16th December 2022 · 9 mins read

Non-Euro Europe Commercial Property Outlook Scandi & Swiss: Sharper value falls to come in 2023 Property values in Scandinavia and Switzerland have taken a hit as yields jumped in recent quarters. With valuations still stretched, we are forecasting a further 50bps and 30bps of rises at the all... 16th December 2022 · 2 mins read

Europe Economics Weekly Hawkish ECB, survey rebound continues Thursday’s ECB meeting confirmed that the Bank is a long way away from pivoting to looser policy. And the strong inflation print in November and rebound in activity surveys in December are only likely... 16th December 2022 · 6 mins read

UK Economics Weekly 2023 – Key themes and possible surprises The three main economic themes of 2023 will be falling inflation, peaking interest rates and a recession. Together they add up to a tough year. Things would be much tougher if inflation surprised... 16th December 2022 · 7 mins read

Emerging Europe Rapid Response Russia Interest Rate Announcement (Dec. 22) 16th December 2022 · 2 mins read