Beyond the core: Navigating property's structural revolution

Beyond the core: Navigating property's structural revolution

New analysis highlights the shifts in commercial real estate markets.

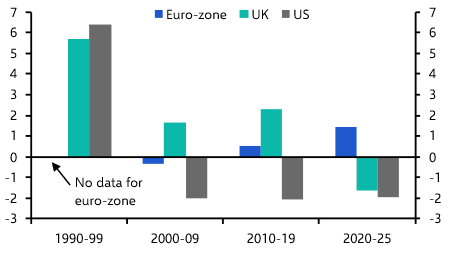

Structural changes in our economies have been the primary drivers of sector performance over the last 25 years. Online shopping has grown from a niche business at the turn of the century to accounting for a third of retail sales in some markets, while the extent of remote work was turbocharged by the pandemic. These factors have fundamentally altered the risks and opportunities in the traditional sectors.

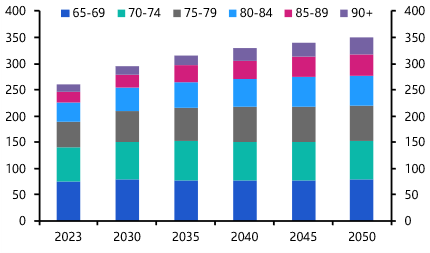

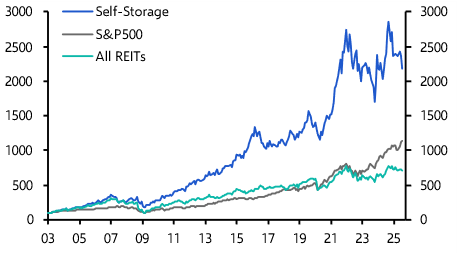

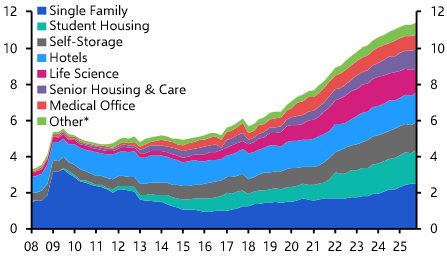

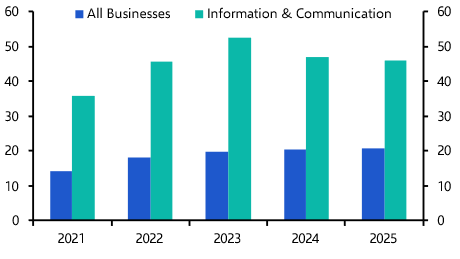

Now, with prospective returns looking less appealing, investors are increasingly turning to a range of alternative sectors with a view to generating higher risk-adjusted returns, improving diversification and keying into the trends that will shape our economies over the next 25 years. Demographic megatrends such as ageing populations and immigration flows, AI's growing importance in all areas of life, and the higher interest rate environment provide structural support for sectors such as senior living, data centres, self-storage, and co-living. When combined, these sectors are no longer fringe and are instead becoming the pillars of a resilient portfolio.

This page lays out how those themes will underpin winning and losing sectors over the coming years, incorporating a new body of work from Q2 2026 as well as the most important pieces from earlier analysis prompted by the pandemic.

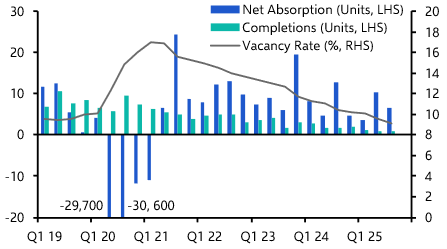

Alternatives

More investors are looking at an increasingly broad range of alternative sectors, driven by a poor outlook for some traditional sectors and high pricing in others. But not all alternatives are created equal, with some sectors and markets suffering from cyclical oversupply or demand deficiency and others with exceptionally strong structural drivers.

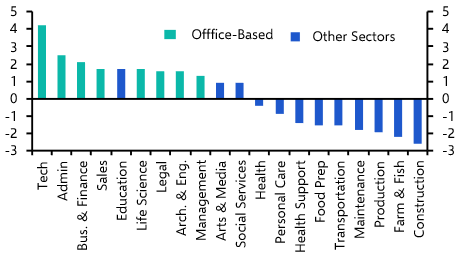

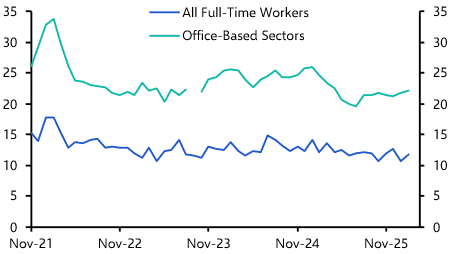

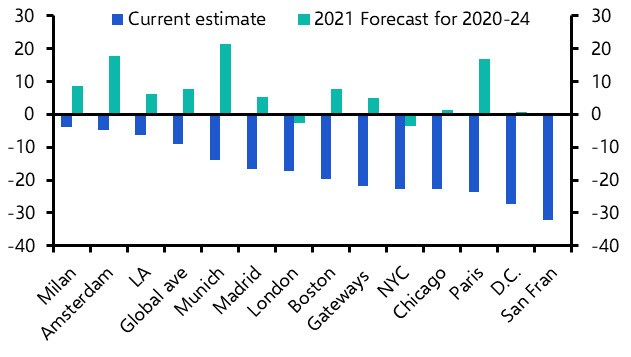

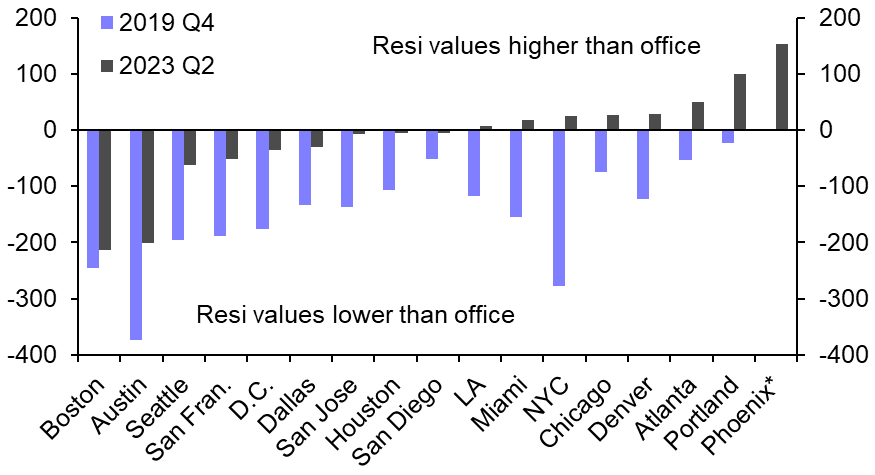

What will the office market look like by 2030?

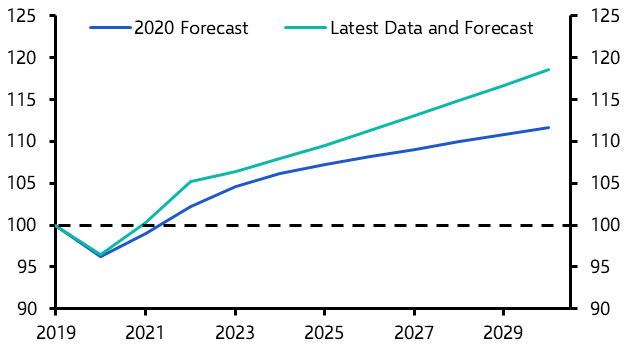

The office sector faces dual headwinds from remote work and the AI transition, both of which will keep demand in the doldrums over the coming years. Conversions from office to other use are going strong, but older, poorly located stock will continue to suffer.

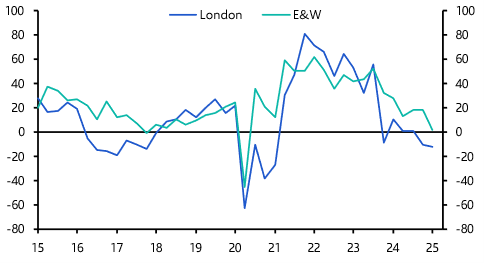

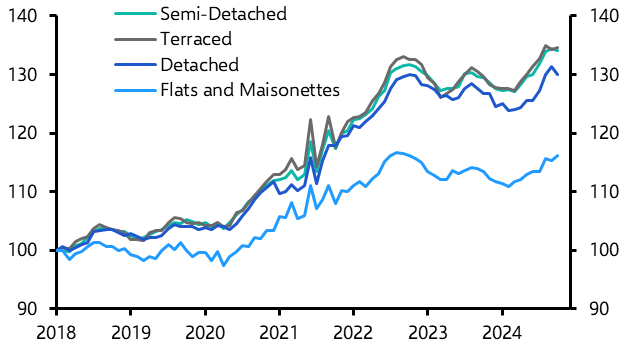

What next for the residential sector in a post-pandemic world?

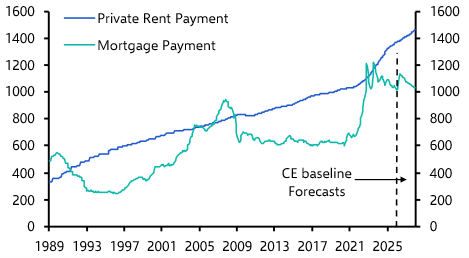

The pandemic and remote work has structurally increased the amount of their incomes that households are willing to spend on their homes, as well as bringing forward moves to the suburbs. Cheaper locations also benefited, but those moves have since slowed. The major driver of residential markets now is the divergence between purchase and rental affordability in a high interest rate world.

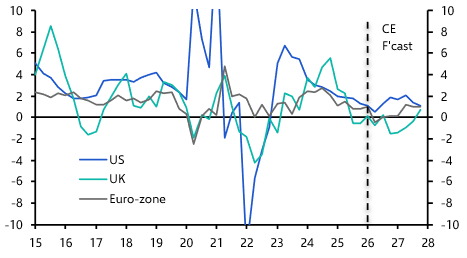

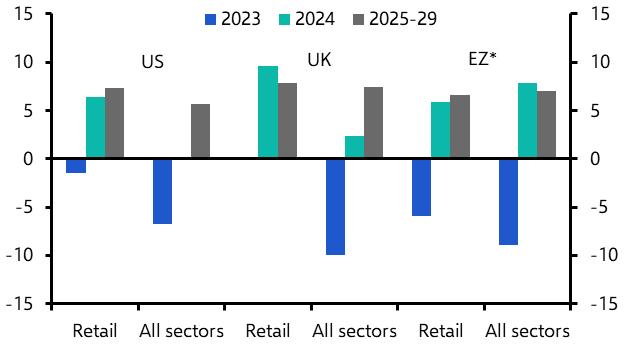

The impact of changing spending habits on retail, hospitality and warehousing

Online spending re-based at a higher level during the pandemic but will continue to account for a larger share of retail sales into the 2030s, supporting out-of-town performance. But warehousing's pandemic-era boom is over and we expect absorption closer to "normal" levels in the next 5-10 years, with slower rental growth in turn.

Meanwhile, rising spend on "experiences" will support occupancy in shopping centres and leisure assets, with luxury hotels also faring well. Business travel will remain a drag due to changed working patterns.

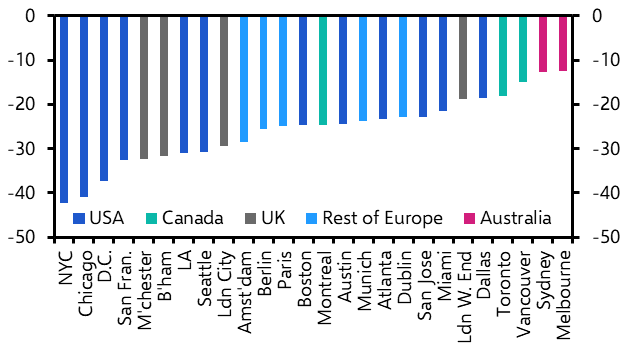

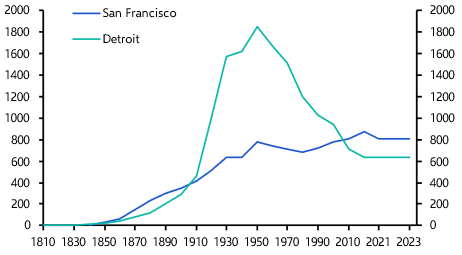

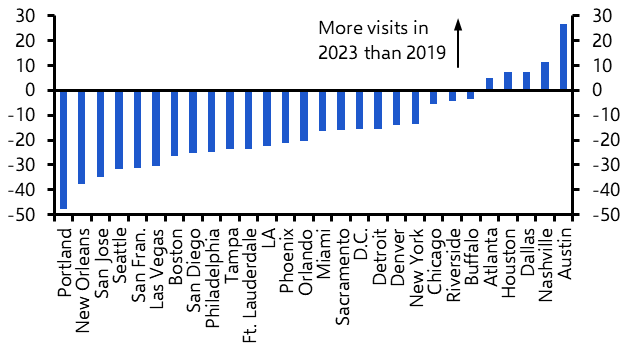

Can cities recover?

Cities will recover, but the largest will underperform over the coming years.

Table of Contents