This Weekly Roundup highlights our analysis of Kevin Warsh's reform plans, your FAQ about private credit, a look at how earnings expectations are driving US equities, insight into the challenges and opportunities for Israel from AI and more.

1.

The coming week’s Fed meeting may be Jerome Powell’s last as Chair, but the focus is already turning to likely successor Kevin Warsh. His Senate testimony this week pointed to the biggest Fed reforms in years, including switching up its preferred inflation measure. That wouldn’t simply be a way to justify rate cuts, despite what some critics maintain. Our regular post-Fed, ECB and Bank of England decision Drop-In is on Thursday at 1000 ET/1500 BST. Register here.

2.

This FAQ from our packed-out briefing this week on private credit’s macro and market risks explains why we think the systemic threat is low, but also entertains what an adverse scenario would look like and how the authorities might respond. Problems in the sector are generating their fair share of headlines, but there’s few signs of spillovers to what is still a fairly robust US credit environment.

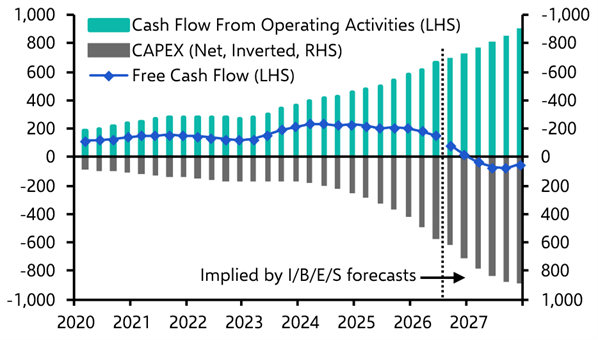

3.

Roughly 20% of the S&P 500’s lofty expected earnings growth is implied by Nvidia alone, a reminder of how heavily the market is leaning on the AI chip giant – and big tech more broadly – to deliver this season and keep US equities so buoyant. Ahead of a packed week of reports from big tech, Senior Markets Economist James Reilly flags the risks.

4.

For Israel, where cyber software exports account for about 3% of GDP, Mythos, a vulnerability-hunting AI, represents both the risk and opportunity from this technology. It could life harder for firms focused on finding bugs, but help those that stop attacks as they happen and provide always-on security. Liam Peach draws on our AI Economic Impact Index to assess what it means.

5.

The Iran conflict is reshaping global economics in unexpected ways. This time is different for Argentina: its booming oil and gas production offers a buffer against the energy shock, strengthening its external position, though the overvalued peso remains a problem. Meanwhile, the 50% surge in urea prices reflects a surge in fertiliser prices that will drive up food inflation worldwide, with lower-income economies in Africa and South Asia facing the hardest hit. All of our key analysis can be found here.