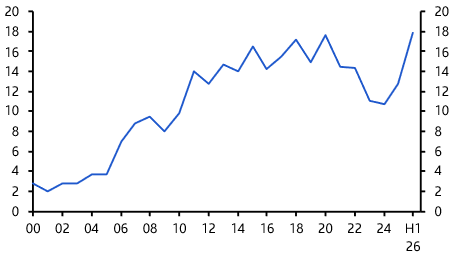

APAC Commercial Property

Asia-Pacific market set for weakest recovery on record

Explore the analysis and forecasts in our inaugural APAC Commercial Property Outlook

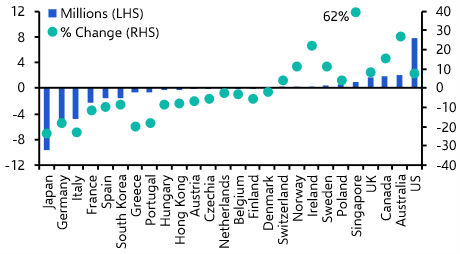

APAC commercial property in data

Explore our five-year forecasts across major regional markets and sectors in this interactive dashboard

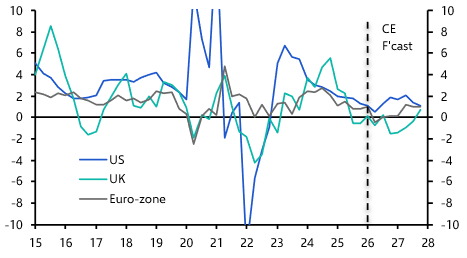

Key Regular Reports

The latest editions of our Outlook, Valuation Monitor & Chart Pack

Our Economists Recommend

The latest key insight, in-depth analysis and thematic research collections

Featured Economists

-

Kiran Raichura

Chief Commercial Real Estate Economist

Kiran heads up Capital Economics’ commercial real estate team, having spent 20 years analysing and forecasting global real estate markets, including 11 years forecasting European and US markets at Capital Economics. Kiran started his career at Colliers International in London, leading its UK Commercial Property forecasts. He then spent four years at AXA Real Assets, where he was the team’s economic expert, and led the firm’s Nordic and Central European research & strategy coverage. Kiran holds a Bachelor’s degree in Economics from The University of Warwick and a Masters in Real Estate Investment & Finance from Henley Business School & Reading University. He is an IPF member and former chair of the Society of Property Researchers.

-

Henry Chan

Commercial Real Estate Economist

Henry Chan joined Capital Economics as a Commercial Real Estate Economist in February 2025, currently covering Asia-Pacific and US Commercial Property. Before joining Capital Economics, he was a Manager of Asia Pacific Research at CBRE. Prior to that, Henry worked for a major Hong Kong developer and a family office real estate firm, as an economist and an investment analyst respectively. Henry holds a Master’s degree in Economics from The Chinese University of Hong Kong and a Bachelor’s degree in Economics and Finance from The University of Hong Kong.