Filtered by Topic: Monetary Policy Use setting Monetary Policy

The South African Reserve Bank finally joined the EM easing cycle today, lowering its repo rate by 25bp to 8.00%. While the MPC clearly has some lingering concerns about the inflation outlook, we think sluggish growth and at-target inflation will provide …

19th September 2024

While UK Gilt yields might rise a bit further in the near term, we think that they will fall back before long, as the Bank of England eventually delivers more rate cuts than most anticipate. After delivering a first cut in August, the Bank of England left …

We’ll be discussing the differences in the policy outlook for the Bank, the ECB and the Fed in a 20-minute online briefing at 3pm BST today. (Register here .) By leaving interest rates at 5.00% the Bank of England showed it is more like the ECB than the …

The Norges Bank left rates unchanged today and shifted its guidance only very slightly in a dovish direction. Whereas the Bank does not expect to cut rates until Q1 next year, we think it is likely to do so in December and to then cut rates fairly rapidly …

The Fed did cut its policy rate by a bigger 50bp today, to between 4.75% and 5.00%, but the vote was not unanimous and the new rate projections point to smaller 25bp cuts at the remaining two FOMC meetings this year. Accordingly, today’s announcement is …

18th September 2024

Unlike their counterparts in the Fed, policymakers at the Riksbank have ruled out making a bumper 50bp rate cut anytime soon. Instead, they are likely to cut their key policy rate by 25bp at next week’s meeting. Further ahead, we think the Riksbank will …

South Africa’s mixed recovery South Africa’s economy is enduring a clear divergence in its economic recovery. Consumer-facing sectors appear to be performing better but industry, particularly mining, continues to struggle. We think interest rate cuts will …

The US Federal Reserve looks certain to start its loosening cycle this evening and, by virtue of their dollar pegs and open capital accounts, central banks across the Gulf will follow suit. Lower interest rates may provide relief to firms and households …

We now think the RBNZ will be one of the few central banks to cut rates below neutral this cycle, which would be bad news for the New Zealand dollar. New Zealand markets have so far shrugged off the RBNZ’s dovish tilt – and rate cut – last month. While …

13th September 2024

Inflation keeps falling more quickly than Norges Bank’s forecasts but policymakers will be uneasy about the renewed weakening of the krone. We expect them to repeat that the policy rate will be unchanged “for some time ahead”, but we think they will opt …

12th September 2024

There was never any doubt that the ECB would cut its deposit rate by 25bp today, to 3.5%. Meanwhile, the policy statement and press conference were largely as expected and do not change our view that the next rate cut is most likely to be in December – …

The Fed’s upcoming monetary easing cycle will probably provide less of a tailwind to EMs than is widely thought. While it’s likely to give some central banks (such as in the Gulf, Mexico and Indonesia) a green light to lower interest rates, EM rate …

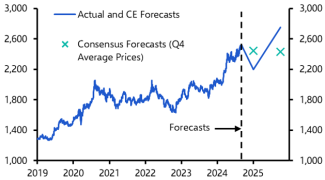

Note: we will be hosting an online Drop-in on Wednesday 11th September at 3pm BST to discuss the outlook for gold prices. Sign up here . With a long and varied list of supportive drivers to choose from, we have raised our end-2025 gold price forecast to …

10th September 2024

The tightening of Brazil’s labour market and pick-up in wage growth over the first half of the year has supported a consumer boom. We expect conditions to cool over the coming quarters but, for now, the buoyant labour market is adding to the central …

5th September 2024

We held online Drop-In sessions earlier this week to discuss the outlook for major DM and EM economies and the risks that they face as we look forward to 2025. (See a recording here .) This Update answers some of the questions that we received, including …

Following its third consecutive 25bp interest rate cut today, the communications from the Bank of Canada reiterated that further cuts are likely. We expect 25 bp cuts at the final two meetings this year. While Governor Tiff Macklem left the door open to a …

4th September 2024

Attention in Egypt is turning to the timing of the first interest rate cut. The lessons from the start of the last easing cycle in 2018 suggest that this is likely to begin in April, which is a little later than most expect. But the more important point …

3rd September 2024

Inflation in Korea fell back sharply last month, supporting our view that the central bank will cut interest rates at its next meeting in October. Inflation data published today showed that the headline rate fell from 2.6% y/y in July to 2.0% in August. …

The PBOC appears poised to step up its efforts to prevent bond yields from falling, even though lower borrowing costs would help the economy right now. The inconsistencies in its policy approach are linked to the shifting whims of the Party leadership, …

29th August 2024

The pick-up in Nigerian GDP growth seen in Q2 will probably be followed by a renewed slowdown this quarter. But we think the backdrop of rising oil production, falling inflation and possible interest rate cuts should set the stage for a more sustained …

28th August 2024

Rates left on hold, easing cycle will be more “stop-start” from here The Hungarian central bank (MNB) suggested that its decision to leave the policy rate on hold today, at 6.75%, was likely to mark a temporary pause in the easing cycle, rather than an …

27th August 2024

The Bank of Korea left rates on hold again today but sounded very dovish. With policymakers now more confident about achieving their inflation target and domestic demand set to remain weak, we think the BoK will start to cut rates in October and that the …

22nd August 2024

Central bankers are unlikely to offer much forward guidance at this weekend’s Jackson Hole symposium, preferring to stress their “data dependence”. Since most economies are expanding, inflation is easing back to target and financial markets have …

21st August 2024

We don’t think the slew of inflation-busting public sector pay deals that have been agreed by the new government will prevent wage growth from slowing next year to the rates of 3.0-3.5% we think are consistent with the 2.0% inflation target. But the big …

With the Fed set to finally start loosening policy and a soft landing still looking like the most probable outcome for the US economy, we think unfavourable rate differentials and continued robust risk appetite will lead to some further weakness in the US …

The South African Reserve Bank’s (SARB’s) new “supercore” inflation measure adds yet another piece of evidence that price pressures are being brought under control. We think the SARB should now be confident that it can start its interest rate cutting …

20th August 2024

We think the Riksbank will follow today’s 25bp rate cut with a cut at each of the three remaining meetings this year to take the policy rate to 2.75%. But we expect the terminal rate to be 2.5% which will be reached in early 2025. This is higher than the …

The global macroeconomic risks surrounding a possible ceasefire deal between Israel and Hamas are asymmetric. An agreement – while having significant economic consequences for countries in the region – would probably not itself be a game-changer for …

19th August 2024

Norges Bank’s decision to leave its policy rate unchanged at today’s meeting, at 4.5%, was never in doubt. However, we still suspect that continued declines in inflation will allow it to start cutting before the end of the year, which would be earlier …

15th August 2024

Since the Riksbank’s last meeting in June, Swedish inflation and activity data have been weaker than policymakers expected. We think this will encourage them to cut the key policy rate from 3.75% to 3.5% next week and to indicate at least a further 50bp …

14th August 2024

The RBNZ began its easing cycle with a 25bp rate cut at its meeting today. Although the Bank appeared to strike a cautious tone about further policy easing, we think it will cut rates more aggressively than many are anticipating. We were among the 12 …

Inflation in Norway has continued to fall more quickly than policymakers expected. But with the krone coming under renewed pressure recently, we think they will maintain a hawkish tone next week. At the last meeting, in June, Norges Bank left its policy …

9th August 2024

Recent safe haven flows into the franc may have prompted limited FX interventions by the SNB. But we think that the policy rate will remain its main policy tool, even for dampening the franc’s strength. Indeed, we now expect the SNB to cut its policy rate …

8th August 2024

The recent market turmoil didn’t move the needle for the MPC today: it continued to strike a hawkish tone as the majority of members voted to keep the repo rate unchanged at 6.50%. But with inflation set to fall back towards the RBI’s 4% target over the …

We are in the minority of forecasters who expect the Reserve Bank of New Zealand to hand down a 25bp rate cut at its meeting next week. Moreover, with excess capacity in the economy rising rapidly, we think the Bank will embark on a more aggressive easing …

7th August 2024

Although the UK has clearly been caught up in the recent turmoil in global financial markets, we do not think a double-dip recession is on the cards. Nonetheless, the disorderly market reaction, if sustained, raises the downside risks to our GDP forecast …

6th August 2024

The minutes to last week’s central bank meeting in Brazil raised the possibility that policymakers will respond to the worsening inflation outlook by hiking interest rates. And despite the sharp shift down in US interest rate expectations since that …

Although the RBA left rates on hold today, it poured cold water on market expectations that it will loosen policy later this year. With the economy still running above its speed limit, we continue to believe that rate cuts won’t be on the agenda until Q2 …

Japan’s government has intervened in the FX markets to weaken the yen far more often than to strengthen it. But FX interventions have become very rare over the past two decades and our sense is that the government is welcoming a stronger exchange rate in …

Fears of a US recession have rattled EM equity markets at a time when EM economies themselves are showing more pronounced signs of weakness. Most EM currencies have held up well, suggesting a dovish tilt may come from EM central banks – particularly those …

5th August 2024

The Bank of England kick-started a loosening cycle today by cutting interest rates from 5.25% to 5.00%, but the accompanying guidance and forecasts suggest it will proceed cautiously. Accordingly, we suspect the Bank will keep rates on hold in September …

1st August 2024

CNB slows easing cycle, but rates will still fall further than many expect Czech National Bank (CNB) Governor Michl sounded fairly cautious in his guidance about the future course of the easing cycle in the post-meeting press conference. But the …

Fed lays the groundwork for September rate cut There was no surprise rate cut from the Fed today, with the fed funds target range left unchanged at between 5.25% and 5.50%, but the changes in the accompanying statement – which included a shift from a …

31st July 2024

The fading drag from load-shedding was widely expected to allow a recovery in South Africa’s economy this year, but this hasn’t materialised. We think that weak demand is to blame, itself a symptom of tight fiscal and monetary policy and a challenging …

The Bank of Japan outlined a plan for reducing its bond purchases and hiked its policy rate by 20bp today. We think it will follow up with another 20bp hike at its October meeting . Only one-third of analysts polled by Reuters, ourselves included, had …

We think the yen’s rally will continue, but suspect that won’t stop the Australian and New Zealand dollars – alleged victims of the carry trade’s unwind – from making some ground over the next year or two. Australia’s Q2 inflation data took a bit of a …

In detailed analysis last year, we concluded that equilibrium nominal interest rates would settle at between 3% and 4% in advanced economies in the next ten years. We maintain that opinion and in fact some of the forces boosting equilibrium rates seem to …

30th July 2024

Donald Trump’s comments on the Fed have brought the issue of central bank independence into the spotlight. This is not just a concern in the US but an issue that is rearing its head in a number of EMs too. In general, these fears look overdone. But …

29th July 2024

Alongside its decision to cut interest rates today, the Bank of Canada struck a more dovish tone than in June, supporting our forecast that another cut is coming at the next meeting in September. The Bank’s second 25 bp cut, taking the policy rate to …

24th July 2024

The latest flash PMIs suggest that while GDP growth probably slowed in Europe at the start of Q3, it continued to recover in Japan. Although the rise in shipping costs has caused manufacturers’ input prices to rise, central banks may take comfort from the …