The Weekly Briefing:

How likely is an economic soft landing?

A Capital Economics podcast

5th May, 2023

The week began with another US bank failure and ended with hotter-than-expected headline jobs data. In between, Jerome Powell sounded optimistic about the likelihood of a soft economic landing. But how realistic is that? Group Chief Economist Neil Shearing talks to David Wilder about credit conditions, labour markets and why the Fed may have stopped hiking, even as the ECB is set to carry on.

Plus, upcoming Turkish presidential and parliamentary elections are make or break for the country’s crisis-battered economy. Liam Peach, who leads our Turkey coverage, discusses the risks around the election with Chief EM Economist William Jackson – including the tough choices that Kemal Kilicdaroglu would have to make if he defeats President Erdogan when the country goes to the polls.

Analysis referenced in this episode:

Transcript

David Wilder

It's Friday, 5th May and this is your Capital Economics Weekly Briefing. I'm David Wilder. Coming up, we'll be hearing about Turkeys make-or-break elections, but for now I'm joined by Group Chief Economist Neil Shearing. Hi, Neil.

Neil Shearing

Hi, David.

David Wilder

I want to get onto payrolls and the week's big policy decisions. But before I do, what's the latest on the banks? The week began with the failure of First Republic – that's the third US bank to go under this year – and the markets are placing bets on the next institution to fall. Jay Powell said on Wednesday, in his press conference, that the resolution of First Republic “kind of draws a line under that period” of bank turmoil. But it doesn't really look like that from the perspective of the stock market, does it?

Neil Shearing

It doesn't look like that from the perspective of the stock market. And you're right, there are echoes here of 2007-2008 and some have drawn parallels to that period insofar as one institution fails, and the market sniffs around for the next institution that might fail, the next domino to fall. And that seems to be what's playing out at the moment. Now, I mentioned 2007-8 because that's what people have tended to reach to when drawing comparisons. And I think there's some important differences, though. Back then it was about credit quality, it was about asset quality of banks, and really a sense that a lot of the loans that the banks were holding were going to turn bad. This isn't about the credit quality on the asset side of bank balance sheets. It's more about the profitability of banks. And, in particular, the way that higher interest rates have affected banks. We've talked before in this podcast about how as interest rates have increased, returns on money market mutual funds have also increased. And that in turn has meant that it's sucked deposits out of the banking system because deposit rates in banks have not kept pace with returns in those money market mutual funds. The problem for banks is that, on the asset side of their balance sheets, a lot of their assets are long-term loans, fixed rates, and those rates are kind of 3.5-4%. So if they raise interest rates on the deposit side, it squeezes their profits. Now, that's a long way of saying this is a profit issue rather than a solvency issue. But I think the problem is that because interest rates – okay, we'll get on to it, they may have peaked – they're not going to come down very far very soon. I don't think this is an issue that's going to go away quickly for banks. So we're going to see more institutions run into trouble, I suspect.

David Wilder

One data point that we've been focused on since, well, even before this bank turmoil kicked off, is the Fed’s Senior Loan Officer Survey. The next one is due the day that this podcast is going out. The last one, which was released before SVB failed made for pretty grim reading. Presumably so will this next one. So how do data points like this, data points showing that credit availability is tight and getting tighter – how does that stack up against Powell’s optimism on Wednesday when he was talking about the possibility of a soft economic landing for the US?

Neil Shearing

Well I think there are several important things to consider here. One is what's happening in the US labour market. And one is what's happening in the financial sector. And like you say, in the banking sector, and with loan provision and credit demand. On the former, the labour market, there might be some signs of a “soft landing”. In particular, we saw the quits rates has fallen back in the latest JOLTS survey. That's now consistent with wage growth slowing. In particular, the vacancy rate is dropping back without the unemployment rate picking up. So, in the jargon, the Beveridge curve, as economists like to refer to it, is shifting down. That is a precondition, I think, for a soft landing in the real economy. The problem really is about the financial sector. And the extent to which the problems in banks feed through into financial conditions, loan provision, credit provision in the real economy. And that means ultimately, the Fed loses control of the process, that there's a tightening of credit conditions over and above what it thought was warranted and what it has anticipated as a result of the increases in interest rates that it's put through. And I think that's the big issue. And we'll get, as you say, more evidence of the extent to which that's happening when we get the Senior Loan Officer Survey in the coming week. But to my mind, the labour market is critically important, but whether or not this is a soft landing, mild recession, or something more severe, a deeper recession, will depend on how credit conditions and financial conditions evolve over the coming months.

David Wilder

We've just had the April non-farm payrolls number: an upside surprise on the headline jobs growth number and on the wage growth data. How does that sit with this idea that that there is a path towards a soft landing?

Neil Shearing

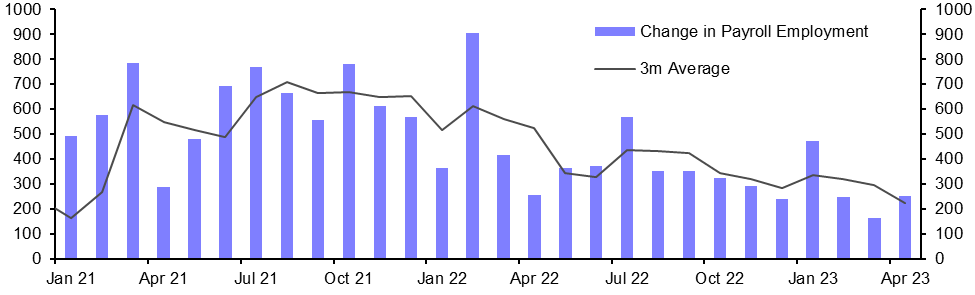

Well, in a way, April's payroll report really illustrates the dangers of reading too much into that headline number. It comes out in particular because, yes, the headline number for April was pretty strong. But the number for jobs added in March and then February was revised down quite heavily. So it's always strange how the market focuses on this headline number for jobs added when the headline number itself is so prone to revision. And we've sort of seen that play out in the latest reports. So if you look at the three month average of jobs added, actually that's edging down. It's now at the lowest rate that it has been since January 2021. But it's edging down gradually – the labour market still looks like it's in pretty robust shape. It’s no longer really super-hot like it was six months ago, but there are signs jobs growth is cooling. But the labour markets is certainly not collapsing. As for the average hourly earnings number, you're right, it's surprised on the upside, but we suspect there's some seasonality in that and to do with the way that the survey has been put together. So expect that to drop back next month.

David Wilder

And can we turn to Europe – that was the other big policy decision of the week 25 basis point hike from the ECB, a dovish statement but then a different tone in the remarks delivered by Christine Lagarde in her press conference. Why is Madame Lagarde insisting they're not done yet with rate hikes where the Fed now seems content to take a breather and, as our US team calls it, “assess the damage”?

Neil Shearing

I think part of it is that the ECB is just a bit further behind the Fed, the Fed is going all the way to five to five and a quarter and policy rates. The ECB is now sitting at 3.25% so it's a bit further behind in terms of the extent of the tightening that's already taken place. I think another factor is that price pressures in the eurozone economy are still uncomfortably high for the ECB. So lots of focus on the fact that headline inflation dropped back in the latest reading but core inflation picked up, as our Chief Europe Economist Andrew Kenningham has noted. So, underlying price pressures still too strong, the ECB is a bit further behind the Fed in this tightening cycle and that explains why Lagarde and others on the Governing Council think they've got a bit more work to do. Now, with that being said, we had previously thought that rates might go to 4% in this cycle. It's probably likely now I suspect that we get two more 25 basis point increases, including one at the next meeting in June, so we think perhaps 3.75% is a more likely peak for rates. But you're right, the ECB is further behind with a bit more work to do. The big picture is that most major central banks now are either at the end or getting to the end of the tightening cycles, though.

David Wilder

Does that include the Bank of England. The big event for the coming week is the Bank of England's May decision. We've been forecasting a rise in Bank Rates to 4.5% since last year. It looks like the markets are finally coming around to our view. So what's the big message that we can expect from the MPC on Thursday? Is it going to be a Fed-style “taking stock”? Or will it be the ECB’s sort of “we're not done yet” message?

Neil Shearing

I think it's incredibly difficult for central banks. If they think they've basically got to the end of their tightening cycle, how do you message that to the markets, because if you send the message that you're essentially done, then what will happen is the market will quite quickly turn its attention to when you might start to cut interest rates. And, paradoxically, having just increased interest rates, you end up by actually loosening financial conditions, because the bond market rallies, yields come down in anticipation of cuts to come. So it's a really difficult communications game at the end of cycles. And we’ve seen this play out in previous cycles when, if you look back, it's very difficult for central banks to signal to the markets “We're done – but don't price in those cuts that you might be thinking is coming in a few months’ time”. And of course, the Bank of England itself has had its own communications challenges over the past several years. So I suspect it could get quite messy. I suspect that the most likely outcome is a 25 basis point increase that takes you, as you say, to 4.5%, they'll I suspect be some language in the communication to the effect that now maybe it's time to stop, take stock evaluate and I suspect, put emphasis on the amount of tightening that's already taking place, and yet to feed through. So the main message is to focus less on the 25-basis point increase that seems pretty likely to happen and more on the communications from the Bank in terms of what will happen going forward. Our best guess is that, having increased interest rates by 25 basis points at the coming meeting, they will then pause and that will be the end of the tightening cycle.

David Wilder

That was Neil Shearing on the main policy decisions and the economic outlook. And watch out for our UK team’s online briefing on the MPC decision on Thursday. Details on the podcast page. Our Emerging Markets team is also holding a briefing this week to explain the risks around Turkey's election. It's happening this coming Sunday and The Economist this week called it this year's most important election. Obviously there are huge geopolitical implications surrounding the outcome of the election. But it could also mean a seismic change for Turkey's economic outlook as well, as Liam Peach, who covers Turkey for our EM team, discusses with Chief EM Economist William Jackson. Liam starts with the state of play on the race explaining why President Erdogan may be heading for the exit after nearly nine increasingly crisis-fuelled years in power.

Liam Peach

The opinion polls are really really tight. I think, looking at a range of range of polling from a range of providers, opposition candidate Kilicdaroglu who has a very narrow lead over Erdogan for the presidency. I think, in general, it looks like he's polling in about 48% versus Erdogan for about 44%. No candidate looks like they're going to get the 50% vote share needed to avoid a second round runoff later in May. But polls suggest that Kilicdaroglu will win that voate. The parliamentary race is also quite tight, the National Alliance, which is headed by Kilicdaroglu, CHP party and six other parties, are polling just over 50%, the People's Alliance which is headed by Erdogan’s dominant AKP is polling around 42% or so. Obviously, that will translate into a different number of seats in parliament based on the way the proportional allocation of votes to seats works out in Turkey. But I think in in general, the current state of play is that Kilicdaroglu will be Turkey's next president this month, and his party will have a working majority in parliament. I think there's a there's a lot of risks around this, though. I think just looking at the polling in Turkey. Yeah, it really could swing either way. The polls are very tight. A lot depends, I think, on the pro-Kurdish party, the People's Democratic Party, their vote, they’re the biggest players in Turkish politics and no party can really gain a majority without power sharing from them. So there's loads of ways that things could play out – things are going to be very tight before the vote.

William Jackson

Another question that always seems to come up is whether Erdogan will actually allow an opposition victory, particularly if the actual vote results are as tight as the opinion polls are suggesting.

Liam Peach

Yeah, it is a big risk. I think Erdogan probably won't go down easily. I think it depends in large part on how tight the vote is. If the opposition victory is quite slim, I think we're probably going to see a lot of political uncertainty with Erdogan contesting the result. Potentially, there might be a rerun, but this is quite speculative at the moment. A lot of people comment on the Istanbul mayoral election in 2019, when Erdogan uncontested that vote and there was a rerun, a secondary run. So I think this is all possible. It's really unclear. But I think what's likely is that there will be a lot of political uncertainty after the vote and Erdogan probably would contest a very small victory for the opposition.

William Jackson

I mean, it presents a big fork in the road for the economy, doesn't it? The economic policymaking over the past decade in particular in Turkey under Erdogan has caused all kinds of damage for the economy, and investors seem to be looking for some change. I used to feel it was quite a predictable cycle: you got political pressure for the central bank to cut interest rates, you then had a credit boom, current account deficit widened and you inevitably then had a currency crisis, which then the central bank had to drag rates up and there was a deep economic downturn and that cycle repeated itself many times. But it feels like the situation has become more complex and possibly more economically dangerous over the last few years.

Liam Peach

Yeah, I think that's absolutely right. You know, a lot of Turkey's problems are structural, but a lot of them also are a function of the policymaking environment, and at the heart is an inflation problem. And that I think stems from a lack of central bank independence, very loose monetary policy. You know, Turkey suffered a very severe currency crisis in 2021, inflation hit over 80% last year, but the central bank cut interest rates and they’re now at 8.5% so it's a really distortive monetary policy stance in Turkey. Inflation expectations are wildly unanchored. There's a lot of dollarization in Turkey. The government responded to the inflation shock last year with a lot of indexation. Raising pensions, the minimum wage, public sector salaries, all of this is added to the strength of inflation – it’s become entrenched at quite high levels. I think Turkey is also dealing with quite severe macro imbalances in other areas as well, at the moment. The current account deficit is very large, it's at about 6% of GDP on a 12-month sum basis. Current account deficits across Emerging Europe seem to be narrowing. Well, they have been narrowing in recent months. But Turkey, it's just deteriorating even further. It's being financed through quite precarious means and the central bank has low reserve coverage. So all of this sort of gives a sense of Turkey's economy has been pretty poorly managed. There's a lot of imbalances. I think the election really is quite a big chance for a reset.

William Jackson

I think that point about responding to high inflation with policies like indexation is really interesting one. Across the emerging world over the last few years we saw central banks act really aggressively to try and stamp inflation out. Turkey seemed to be the real exception where they sought to accommodate it. If we're thinking then that this election might offer a chance for improved macro policymaking what kind of policies are the opposition offering?

Liam Peach

The opposition haven't actually set out any clear policies, I think they've mostly set out clear goals and objectives. I think once they come into power, we'll probably know a bit more clearly what their policies will be. But their main priorities that they set out in their manifesto are lowering inflation to single digits in a few years, and restoring exchange rate stability. I think the central view among observers, including ourselves is that there's likely to be a return to more orthodox policymaking in Turkey with an opposition victory. I think central bank independence will improve. There's going to be a firmer commitment to inflation targeting. At the very least, there will need to be a shake-up at the central bank and removal of some of the policymakers there. The opposition hasn’t talked about raising interest rates to tackle inflation but I think it's a key part of the remedy that Turkey needs. Much higher interest rates are needed to cool inflation and bring down inflation sustainably. They'll likely need to stay at quite high levels for some time. The opposition have talked about rolling back some of the central bank’s lira-ization measures. These policies that have been put in place over the past year to reverse the dollarization trend in Turkey. But the opposition have come out and said they want to scrap a lot of those, including the lira-protected deposit scheme, which is quite a costly scheme for the Treasury in the event of sharp falls in the currency. There's also been a commitment to greater exchange rate flexibility and removing some of the FX restrictions and the central bank FX intervention that we've become used to in Turkey. I think comments on tighter fiscal policy generally have been quite limited. But I think that's one area that we're going to need to see some measures after the election.

William Jackson

So it sounds like the their intentions are in the right place. I think there's an important question about whether they'd actually be able to do that. I thought you made an interesting point in your response to the latest inflation release, where you identified the strength that while inflation in most categories, and CPI basket, is coming down, services inflation remains very strong. That seems to be related to the domestically generated inflation pressures. There must be a lot that's coming through momentum for indexation. And sense do you have about the opposition's likelihood of actually being able to pull off a return to macro stability,

Liam Peach

I think it's gonna be really challenging. I think the size of the task is huge. Turkey's inflation problem is entrenched. It has very large macro imbalances. I think simply restoring central bank independence and raising interest rates won't be enough. Turkey needs a period of very high real interest rates, very tight fiscal policy for quite some time, in order to bring inflation down sustainably. And that's going to result in quite large economic costs. It's going to probably result in quite a deep recession. But that's part of the adjustment that Turkey needs. At the moment, it’s not clear that there's appetite for that. And I think that's partly why the opposition haven't talked about concrete policies that they'll put in place yet. It's mostly goals and objectives. But I think I think we need to wait and see how these policies evolve. You know, the timescale over which Turkey needs to implement these policies is probably over five years so it's gonna take a while. So I think we just need to wait and see.

William Jackson

So there’s a massive challenge ahead but even so it seems pretty clear that markets would welcome an opposition victory. One debate that seems to be out there is what would happen to Turkey’s financial markets, and the currency in particular, if the opposition wins. Do you think it's a positive environment for the lira, that we might see a bit of a rebound?

Liam Peach

Yeah, I think Turkey's financial markets are gonna move quite sharply after the election, particularly if there’s an opposition victory. I think we know what would happen in the bond market. There'd be big rise in central bank interest rates and long term bond yields in Turkey now look unsustainably low so those are likely to rise quite sharply. There’s a bit of a heated debate about exactly what's gonna happen to the lira. A lot of people think that it might rally might appreciate quite a bit after the election, because there'd be a lot of optimism about economic reform. There'd be a lot of capital inflows coming into Turkey. I think that's possible, I think over a short time period the lira may benefit from that optimism but I think it really is a question over the time period during which the lira might move. Our view is that Turkey needs quite a large exchange rate depreciation to address some of the macro imbalances that have built up, including the large current account deficit and some of these other FX restrictions that have been put in place. So, by the end of this year, we think with an opposition victory and greater exchange rate flexibility, there will be a large depreciation in the currency. But looking forward even further, you could argue that if the opposition is successful in reducing Turkey's risk premium and bringing inflation differentials down quite sharply, then that could reverse the long term, downward trend we've seen in Turkey's real exchange rate over the past decade. So I think it really is a question over time period: short term, I think there's probably going to be quite a big currency depreciation. Longer term, that might put in place some more sort of sustainable footing for the lira.

William Jackson

So some optimism then, particularly for the longer term if the opposition win. But we haven't talked about a potential Erdogan victory – what happens if he wins another term? Is it more of the same? Or do you think he might moderate his economic policymaking?

Liam Peach

I think it probably will be more of the same. I think we know what Erdoganomics means. We've been used to it for a few years now. It means very low interest rates, very restrictive foreign currency and banking regulations and high inflation. I don't think there's any reason to expect that to change. Erodogan is opposed to high interest rates. We don't think he'll moderate his views on that. I think the problem is that current policy in Turkey is just unsustainable. Turkey is losing a lot of export competitiveness, because the central bank is managing the lira. Turkey's balance of payments are a mess, you know, the current account deficit is really large. And it's been financed through central bank reserves. So all of this is quite worrying. At the same time, there's also the lira-ization measures which are helping to prop up the lira but they just don't look sustainable. So I think, you know, if Erdogan were to remain in power, I think we're most likely to see central bank interest rates stay quite low. I think they probably would move to sort of more exchange rate flexibility and let the lira weaken a little bit going forward, or they probably might want to stem the pace of depreciation.

William Jackson

Okay. I mean, one thing that's come across a lot when you're talking about that is everything's looking unsustainable under the current policy settings. And I agree that I don't really see things moderating. Over the past decade or so, economic policymaking has simply been going in one direction. But if we're thinking this is all looking at sustainable, what's the nightmare scenario for Turkey, though?

Yeah, I think

Liam Peach

The bad scenario for Turkey is that this distortive monetary policy framework continues and the central bank holds on to the lira for too long. Ultimately, that's going to store up bigger problems in the economy, and it's just going to increase the chance of a bigger adjustment in the currency in the future, I think we would see the risk of another severe currency crisis increase increase quite sharply. And I think the spillovers from that to the rest of the economy could be quite large as well. The banking sector is one that usually comes up in Turkey as vulnerable to a weaker currency because of FX mismatches and large external debts in the banking sector. The sovereign debt position is also one that's become more precarious over time. There's a lot of FX borrowing. And also this this new lira protected deposit scheme that was introduced after the 2021 currency crisis has left the government on the hook for quite a large bill in the event of sharp currency falls. So how we've characterised it is that there's a risk of a severe currency crisis in Turkey and this then could spill over into simultaneous banking and sovereign debt problems too. I think that's probably the nightmare scenario.

David Wilder

And that's it for this week. All the analysis and client briefings referenced in this episode can be found on the podcast page on our website, capitaleconomics.com. And for complete access to all our content, including powerful data and charting tools, check out CE Advance, our premium platform. If you like this podcast, you can subscribe from Spotify, Apple or wherever you listen to your podcasts. But until next time, goodbye.

Disclaimer

Access to our Products and Services is subject at all times to our Terms and Conditions which contain limitations and exclusions on our liability. For our full Terms and Conditions please see here.