This Weekly Roundup highlights our analysis on what could happen if the Strait of Hormuz reopens, where global inflation is heading, why shrinking the Fed's balance sheet won't work, how to lower China's saving rate and whether inflation is a threat to equities.

1. Reports of an imminent US-Iran deal are raising hopes that the Strait of Hormuz could soon reopen. But even if it does, oil prices may not quickly return to pre-war levels. The latest episode of our weekly podcast (Apple or Spotify) explores what a reopening would mean for oil markets and inflation worldwide.

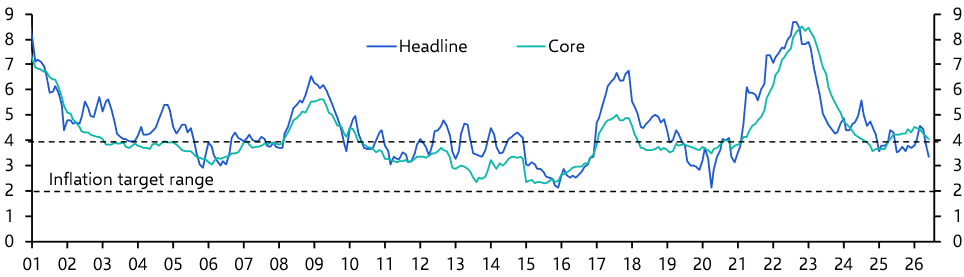

2. Reopening won't stop inflation in some advanced economies rising to 3-4%. But this is not 2022: the broader backdrop suggests markets may still be overestimating how far central banks would ultimately need to tighten in response to another energy shock. Our latest Global Inflation Watch examines how inflation is evolving and central banks are responding. Read the report and join the authors for an online Drop-In briefing on Tuesday 2nd June.

3. Although history shows inflation tends to be bad for equity returns, particularly when driven by a supply shock, current price pressures aren't high enough to be alarming, while the link between inflation and valuations is weaker now than in the past. Clients can assess the risks themselves with our new choose-your-own-adventure equities and inflation dashboard.

4. Europe may ramp up trade defences against Chinese imports, but it will do so only gradually, in part because of internal division about how tough to get. This is partly why we expect China – whose imports from the euro-zone have fallen by 30% since 2019, even as its exports to Europe have risen by the same amount – to continue to gain market share.

5. Kevin Warsh’s swearing-in has revived talk of his pet idea of shrinking the Fed’s balance sheet. But as this February report explained, doing so would not necessarily create room for the lower rates he (and the president) want. Under the Fed’s ample-reserves framework, quantitative tightening would only nudge up longer-end yields, while pushing QT too far risks a funding-market squeeze.

6. The UK may want to increase spending on defence, but its limited fiscal space means this will have to be funded partly through borrowing, but also through spending cuts elsewhere, higher taxes and lower ambitions for public spending. And the upside from all that spending would be modest too.

7. Plans to give China’s migrant workers greater access to public services are being celebrated as a critical step to boost consumption. But the evidence doesn’t support the view that these plans will significantly lower China’s savings rate, which is likely to remain high so long as Beijing holds back on social spending.