The war in Iran has reinforced a narrative that was already well established in our research: China is emerging as one of the principal beneficiaries of global energy disruption. The closure of the Strait of Hormuz and the resulting spike in hydrocarbon prices have accelerated demand for the green technologies China produces at scale: electric vehicles, lithium-ion batteries and solar panels. The macroeconomic implications are substantial.

A structural shift, not a cyclical uptick

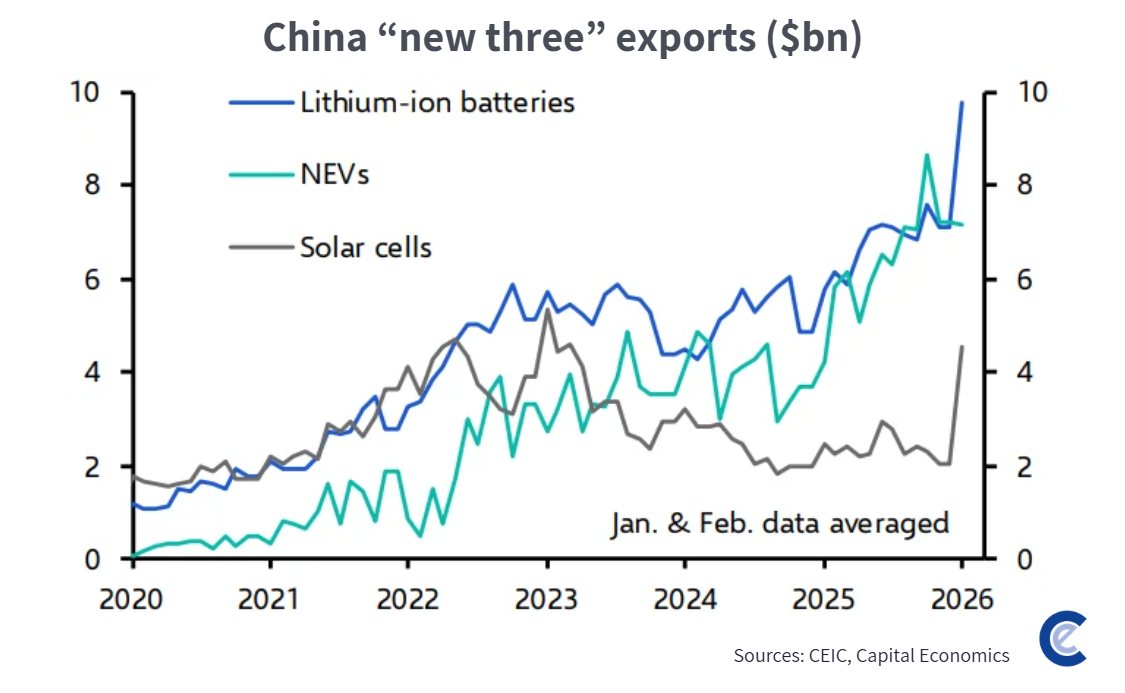

China's green tech exports were already on a remarkable trajectory before the conflict began. In 2025, EVs, batteries and solar panels collectively accounted for around 4.5% of China's total exports, but were responsible for almost 20% of its export growth, in a year when total exports grew by around 5%. That asymmetry reflects a structural dynamic: years of state-backed industrial investment have created enormous manufacturing capacity, while weak domestic demand has pushed producers to find markets abroad. The conflict has added a demand-side accelerant to a supply-side story that was already well advanced.

The most recent trade data, through March 2026, shows China's exports of these three product categories reaching record highs in both value and volume terms, with broad-based growth across Europe, Asia and Latin America. April data, due shortly, is expected to confirm that trend.

Where the growth Is coming from

A notable feature of recent export data is the shifting destination mix. The EU remains a large market, but its share of China's solar panel exports has fallen from around 50% in 2023 to approximately 37% today, reflecting both tariff pressure and the EU's limited capacity to absorb the volume China can now supply. The growth frontier has moved to emerging markets. Pakistan, Brazil and India are now among the top five destinations for Chinese solar panels, and Brazil has seen EV registrations of Chinese-branded vehicles rise by around 300% since the start of this year.

This geographic shift matters for the durability of the export cycle. Emerging market consumers tend to face fewer policy headwinds and, in many cases, China's green tech products represent the most accessible and cost-effective option available. For households in countries with unstable electricity grids, solar-plus-battery systems offer both reliability and affordability. For first-time car buyers in fast-growing cities, a competitively priced EV is not a statement about sustainability. It is simply the rational choice.

Would lower oil prices reverse the trend?

A legitimate question for investors is whether a resolution to the conflict and a normalisation of oil prices would undermine this demand picture. Our view is that the sensitivity is lower than it was following the 2022 energy shock, for three reasons.

First, China's export prices for these technologies have halved since 2022, making EVs and solar panels competitive with fossil fuel alternatives across a far wider range of markets regardless of where oil prices sit. Second, emerging market adoption is structurally less reversible: unlike European consumers who switched to heat pumps and then partly switched back, many emerging market buyers are making first-time purchases rather than transitions. Third, the world has now experienced two major energy shocks within five years. The case for reducing exposure to volatile hydrocarbon supply chains has become materially harder to dismiss.

Macro implications

The combination of strong export momentum and upward revisions to China's growth forecasts is striking against a backdrop of global uncertainty. We now expect green tech to contribute between two and five percentage points to China's export growth this year, with total export growth forecast at around 15% for 2026.

The broader question is whether this wave of green tech adoption could bring forward peak oil. The structural case for an earlier inflection point is strengthening, with consensus currently placing the peak in the early 2030s. In China, the only segment of oil demand still growing is the petrochemical sector, which itself faces increasing pressure from the current energy shock. On net zero, however, we remain cautious. The emphasis among policymakers has shifted from decarbonisation toward energy security, and several major economies – including China, Indonesia and Japan – have rolled back commitments on coal reduction.

What is not in doubt is that China's position at the centre of global green tech supply, commanding around half of global solar panel and battery exports and a quarter of EVs, is now a first-order macroeconomic variable. Institutional investors tracking both the energy transition and emerging market growth trajectories should pay close attention.