Filtered by Subscriptions: Global Markets Use setting Global Markets

Even though we expect the S&P 500 to end 2024 at a much higher level than it is now, we doubt it will build on its recent gains over the coming months given the outlook for the economy. The story for much of this year has been the surprising resilience of …

10th November 2023

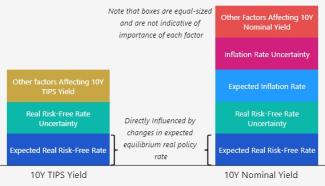

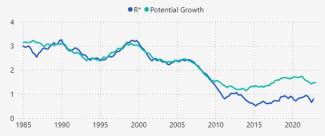

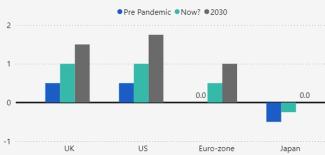

Following the release of our new analysis on real equilibrium interest rates (R*) last month, we held an online Drop-In last week and in-person Roundtable events with clients yesterday to discuss our findings. This Update answers several of the questions …

9th November 2023

We think the Bank of Japan’s continued steps towards policy normalisation are consistent with somewhat higher JGB yields and a significant rebound in the yen over the coming quarters. To recap, the BoJ made another tweak to its Yield Curve Control (YCC) …

2nd November 2023

Although Treasury yields have fallen back in recent days, the big picture is that they are still much higher than they were when headline and core inflation peaked more than a year ago in the US. In this Focus , we examine the role of inflation in the …

Our View: Growth in the US and other advanced economies will disappoint, keeping pressure on “risky” assets but favouring “safe” ones. But when the economic environment improves, “riskier” assets will rebound, with equities further boosted by enthusiasm …

31st October 2023

In line with our upwardly revised forecasts for the 10-year US Treasury yield, we’ve raised our projections for 10-year government bond yields in most other developed market economies. But we still expect those yields to fall, in general, by the end of …

27th October 2023

We think the Chilean peso is poised for a rebound in 2024 as the headwinds from the narrowing interest rate differential and the terms of trade deterioration reverse. The Chilean peso has underperformed nearly all other major emerging market currencies …

26th October 2023

The war between Hamas and Israel – and the potential for escalation to the wider region – has increased the uncertainty around the economic and financial market outlook, but in most scenarios is unlikely to generate a sustained hit to major asset markets. …

We still expect the 10-year Treasury yield to fall in the coming quarters. But we’ve revised up our projections for that yield from now to end of 2025, and now think it will reach its cyclical low in 2024. There are two key reasons why we have pushed up …

19th October 2023

The full report is available to download from the button at the top right to Global Economics, Global Markets, Asset Allocation and The Long Run subscribers, as well as to CE Advance clients. If this is outside of your current subscription and you would …

17th October 2023

Chapter 4: Financial market implications …

Chapter 3: Where will inflation (and nominal rates) settle? …

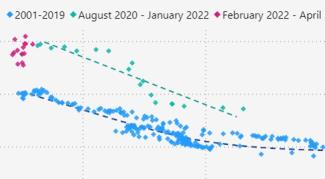

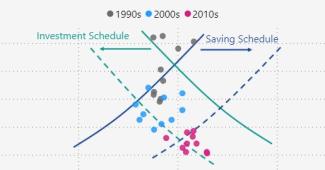

Chapter 2: How will the savings/investment balance affect r*? …

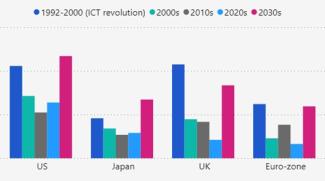

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

We think the macroeconomic environment will continue to play the key role in the outlook for emerging markets (EM) dollar-denominated sovereign bonds this year and next. Despite country-specific risks, we expect the yields of most of those bonds to fall …

13th October 2023

Estimates suggest that the term premium of US 10-year Treasuries has bounced back to positive territory. We think that this can be at least partly explained by demand and supply factors. And we suspect that term premia might rise a bit more, even though …

12th October 2023

The government bond sell-off over the past three months raises uncomfortable questions around the risks of financial instability and the outlook for fiscal policy. This note takes stock of what has driven the rise in long-term sovereign bond yields and …

6th October 2023

While we think the risk of a material increase in euro-zone “peripheral” spreads has risen, our central forecast remains that they will end 2024 a bit below their current levels. Last week, long-dated euro-zone peripheral bond yields reached highs not …

5th October 2023

The sell-off in bond markets has taken a breather today, helped in part by softer data on the US labour market. However, the scale of the moves over the past week has invoked comparisons to previous financial crises that have been caused by sharp moves in …

4th October 2023

The valuations of “risky” assets have only been undermined a little by the big rise in the yields of “safe” assets in recent months. We think that the valuations of risky assets may fall a bit more in the near term, as growth falters. But further ahead …

2nd October 2023

We think the “higher-for-longer” narrative that has taken hold in the market won’t last through 2024. We suspect that central banks will generally cut faster than investors seem to expect and that, as a result, the bond market sell-off will turn into a …

28th September 2023

Although the 10-year Treasury yield rose further to a post-Global-Financial-Crisis high of ~4.5% in the wake of this week’s FOMC meeting, we continue to forecast that it will drop back to 3.75% by the end of this year and to 3.25% by the end of next year. …

22nd September 2023

We expect long-dated government bond yields in most developed market (DM) economies to fall over the remainder of this year and next, as central banks shift focus to monetary easing. But, in some cases, we now predict those falls to be smaller than we had …

21st September 2023

Given our dovish view of monetary policy in Emerging Markets (EMs) – and our increasingly less bearish view of the US economy – we think that EM local-currency government bond yields will fall across the board in the next couple of years, particularly in …

14th September 2023

We’ve revised up our projections for the S&P 500 and the 10-year Treasury yield, but still expect both to fall a bit by the end of this year. We have also tweaked our forecast for the US dollar. We had been projecting that the S&P 500 would struggle over …

Market implied rates suggest that investors expect inflation to normalise in the US and Europe in the next couple of years. While we share that view, we think they are overestimating the level of policy rates required to achieve inflation targets. As a …

8th September 2023

A “soft landing” for the economy in the US seems increasingly possible, so we look back at previous similar episodes to get an idea of what might be ahead for equities there. Despite the Fed’s aggressive tightening cycle over the past year and a half, it …

7th September 2023

Growth in most advanced economies will disappoint later this year, putting pressure on “risky” assets and favouring “safe” ones. Developed markets (DM) government bond yields will therefore decrease further, helped by central banks shifting towards easing …

31st August 2023

We think there is ample scope for the US stock market to perform strongly in 2024 and 2025. Admittedly, this year’s rally in the S&P 500 hasn’t had much to do with expectations of faster growth in earnings per share (EPS). Instead, it seems mainly to …

Gilt yields and sterling have fallen from their cycle highs over the past month or so, and we think the worsening economic growth outlook in the UK and elsewhere mean that this trend will continue over at least the next couple of quarters. Although …

24th August 2023

We think the 10-year Treasury yield will end the year well below its current level. The sell-off in Treasuries seems to have abated somewhat today. But they haven’t had too much relief: the 10-year yield still isn’t that far below the fresh cycle peak it …

23rd August 2023

With the headwinds growing for China’s economy, we think its equity markets will struggle, its 10-year yield will continue to fall and its currency won’t rebound as quickly as we’d thought. At the start of the year China’s economy was powering ahead. But …

17th August 2023

Since our last Financial Market Stress Monitor on 13 th May, strains have continued to ease. This abbreviated Stress Monitor takes stock of developments since then. Overall, stress across core financial markets appears about as low as at any point …

10th August 2023

The yield of 10-year Japanese government bonds (JGBs) may come closer to the new “just-in-case” cap of 1.0% in the coming months, but we doubt it will settle that high further ahead. Since the Bank of Japan (BoJ) effectively abandoned Yield Curve Control …

The US government losing another one of its “AAA” ratings after Fitch Ratings’ downgrade decision Wednesday is more symbol than substance. But three key related points are worth highlighting. First, the market reaction differs significantly from that of …

4th August 2023

We suspect the boost to “risky” assets from the resilience of the economy may have mostly run its course. Risky assets in the US have stumbled over the past couple of days as Treasury yields have climbed. But that still leaves them having made quite big …

The key points that stand out from the recent moves by central banks in Brazil, Chile and Hungary to cut interest rates are, first, how quickly policymakers have shifted from hawkish to dovish and, second, how they appear to be front-loading their …

3rd August 2023

We think El Ni ño poses downside risks to the prices of emerging market assets, in general. But even if the effect in aggregate wasn’t all that large, there are several vulnerable sectors where such an event could create some relative winners and …

The BoJ’s decision earlier today to, in effect, end its long-standing Yield Curve Control (YCC) policy means that long-term government bond yields in Japan will become more responsive to economic conditions and developments in global markets. While that …

28th July 2023

Our View : Growth in most advanced economies will disappoint later this year, putting pressure on “risky” assets and favouring “safe” ones. Developed markets (DM) government bond yields will therefore decrease further, helped by central banks shifting …

The continued rise in the valuations of “risky” assets relative to “safe” ones mostly seems to reflect growing confidence in the economic outlook. We think that optimism will be disappointed and that risk premia may rise again – and valuations may fall – …

26th July 2023

Japan bulls have proposed a range of explanations to justify the outperformance of the TOPIX relative to other equity indices over recent months. While there are some signs that firms are enjoying stronger pricing power, we aren’t convinced that a …

24th July 2023

The Treasury yield curve has been inverted for a long time by past standards, but we think it could remain so until next year even if there’s a recession in the interim. At the start of this month, it briefly looked as though the beginning of the end of …

21st July 2023

Despite today’s big reaction in markets in the UK to better-than-expected inflation news , we still think investors are overestimating the peak in interest rates there and underestimating how much monetary policy will be eased in 2024 and beyond. Indeed, …

19th July 2023

The stock market in the US has rarely rallied in recessions that have taken place there since the mid-1850s. Our forecast is that it will take a knock amid a recession in H2 2023 before powering ahead. We would point to five key examples of the stock …

14th July 2023

June’s soft US CPI print seems to have given investors renewed hope that inflation could fall back to normal levels without the economy slowing too much, if at all. We continue to think that the chance of a more-significant economic slowdown is …

13th July 2023

Not so long ago, a higher 10-year TIPS yield almost invariably meant an underperformance of US “growth” stocks vis-à-vis their “value” peers, a lower gold price, and a stronger dollar. That’s changed in 2023, though, with the relationships weakening …

We still think the yields of long-dated sovereign bonds in Canada, Australia and New Zealand will fall by the end of this year, but no longer expect them to do so by much more than the yields of bonds elsewhere. Canada, Australia and New Zealand have led …

7th July 2023