Filtered by Subscriptions: Global Economics Use setting Global Economics

Although the manufacturing PMIs have overstated the weakness of industry for a while, the big picture from December’s surveys was that global industrial activity was barely growing at the end of 2023. The forward-looking indicators point to further …

2nd January 2024

The rerouting of trade ships away from the Red Sea has come at a time of disruption to shipping elsewhere in the world, but it is unlikely to alter the broad pattern of falling core inflation in 2024. We expect the recent rise in oil prices to prove …

21st December 2023

Most major DMs need to shrink their primary budget deficits significantly and, for various reasons, most are likely to find it hard to do so. This will exacerbate growing worries about fiscal sustainability. Fiscal deficits increased significantly in …

20th December 2023

Some of the negotiations by trade unions and large firms in advanced economies over recent months have resulted in large pay rises of up to 10%. However, they have typically also locked in much smaller gains for next year and hence shouldn’t cause serious …

18th December 2023

We recently held an online Drop-In session to discuss the December policy meetings and the outlook for monetary policy in the year ahead. (See a recording here .) This Update answers several of the questions that we received. Would the Fed ease policy …

Although the flash PMIs ticked up in most cases in December, they suggest that advanced economies will start 2024 on a weak footing. Meanwhile, outside of the US, the subdued outlook for demand seems to be weighing on employment growth, which should take …

15th December 2023

We think that global growth will undershoot consensus expectations in 2024 as the lagged effects of monetary policy tightening filter through. Among the advanced economies, the US will continue to outperform Europe. And while China’s policy-induced …

Table of Key Forecasts Global Overview – We think that global growth will undershoot consensus expectations in 2024 as the lagged effects of monetary policy tightening filter through. Among the advanced economies, the US will continue to outperform …

13th December 2023

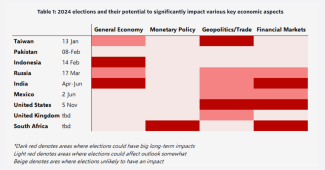

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

7th December 2023

We held two online Drop-In sessions today to discuss the outlook for 2024 and the risks to our forecasts. (See a recording here .) This Update summarises the answers to several of the questions that we received. Are there recessions coming in advanced …

5th December 2023

The manufacturing PMI surveys have overstated the weakness in industrial production over the past couple years. But, even taking this into account, November’s PMIs suggest that while global industry might be past the worst, it looks set to end 2023 and …

1st December 2023

In this Global Economics Update , we describe eight of the biggest risks to our economic forecasts for 2024. The unusual nature of this cycle and uncertainties surrounding the transmission of monetary policy mean that the biggest risks relate to central …

30th November 2023

While global goods trade rose in September, timelier indicators suggest that it has softened so far in Q4. And with props to Chinese exports likely to prove temporary, and advanced economies set to slow, we think that the general weakness of world trade …

29th November 2023

The S&P Global PMIs have provided misleading signals about the strength of activity in the US and Europe this year. But, for what it’s worth, the flash surveys for November suggest that DMs are ending 2023 on a weak note, with activity stagnating or …

24th November 2023

Shifts in the long-term outlook for interest rates relative to GDP growth have left the fiscal position in most developed economies looking more precarious. Unless governments manage to reduce their sizeable primary deficits, market concerns about public …

21st November 2023

While the US economy considerably outperformed its DM peers in Q3, we think that all advanced economies will suffer a weak Q4. High interest rates are weighing on credit growth, and a further rise in debt servicing costs in the coming quarters is likely …

17th November 2023

During the past decade, the global economy has transitioned out of an era in which globalisation was the key driver of economic and financial relationships into one shaped by geopolitics. Previously, most governments had believed that closer economic …

16th November 2023

We expect growth to slow and inflation to drop to central bank targets in major DMs in 2024. But the latest business expectations surveys on the face of it suggest that the risks to our forecasts are tilted towards activity and inflation being more …

15th November 2023

Bank lending data from the major advanced economies confirmed that lending was very subdued in September and the latest bank lending surveys show that banks have since tightened their lending criteria further. With demand for loans also falling, the drag …

9th November 2023

We held a Drop-In last week to explain our thoughts on the latest policy communications from the Fed, ECB, and Bank of England following their decisions to leave rates on hold. (See the recording here .) This Update answers several of the questions that …

6th November 2023

October’s manufacturing PMIs suggest that global industrial activity continued to contract at the beginning of Q4 and forward-looking indicators point to further weakness ahead. The output component of the global manufacturing PMI fell from 49.7 in …

2nd November 2023

Although consumer spending has remained remarkably resilient in the US so far this year, it has weakened in other advanced economies. And as the lagged effects of high interest rates filter through to households in an environment of low consumer …

Global goods trade rose slightly in August and timelier data point to further gains in September. But we expect global trade to fall again in due course as economic downturns in several advanced economies weigh on their demand for traded goods. According …

27th October 2023

The October flash PMI surveys suggest that economic activity got off to a weak start in Q4, especially in Europe. And with weak activity taking some of the steam out of labour markets and inflation, we are growing more confident in our view that the Fed, …

24th October 2023

Overview – Global headline inflation has fallen sharply from its peak a year ago and, despite a temporary setback due to higher fuel inflation, we expect it to fall a lot further over the coming year. The huge drag from energy inflation is now largely in …

The full report is available to download from the button at the top right to Global Economics, Global Markets, Asset Allocation and The Long Run subscribers, as well as to CE Advance clients. If this is outside of your current subscription and you would …

17th October 2023

Chapter 4: Financial market implications …

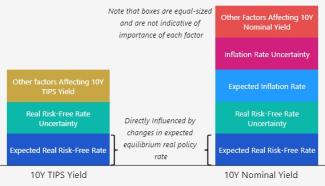

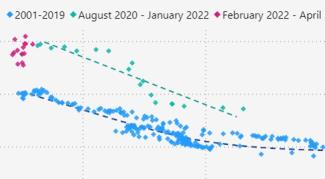

Chapter 3: Where will inflation (and nominal rates) settle? …

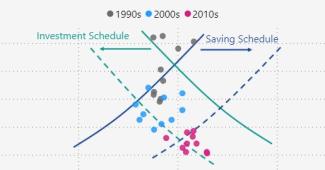

Chapter 2: How will the savings/investment balance affect r*? …

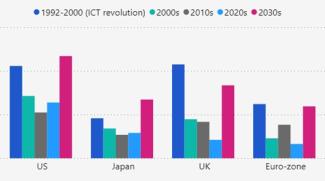

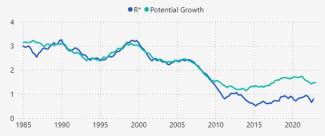

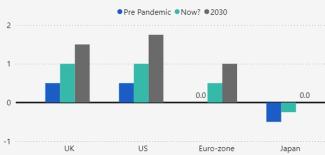

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

Perceptions matter at least as much as actual policies in determining fiscal stability. Accordingly, the surge in bond yields over the past month poses the greatest risk to those countries where the government’s commitment to fiscal rectitude over the …

16th October 2023

The latest activity and survey data have provided even more evidence that the resilience in activity in advanced economies over the first half of 2023 is now fading. High interest rates are clearly weighing on credit growth, and a further rise in debt …

13th October 2023

The government bond sell-off over the past three months raises uncomfortable questions around the risks of financial instability and the outlook for fiscal policy. This note takes stock of what has driven the rise in long-term sovereign bond yields and …

6th October 2023

The ‘higher for longer’ narrative on interest rates that is baked into market pricing is at odds with evidence of widespread falls in inflation. Higher oil prices mean that fuel inflation will be a bit higher than seemed likely a few months ago. But the …

5th October 2023

The sell-off in bond markets has taken a breather today, helped in part by softer data on the US labour market. However, the scale of the moves over the past week has invoked comparisons to previous financial crises that have been caused by sharp moves in …

4th October 2023

Note: We discussed the key takeaways from our Q4 Global Economic and Markets Outlooks in a Drop-In on Wednesday, 11 th October. To view the recording Click here . Table of Key Forecasts Global Overview – We think that the now popular assumption that …

3rd October 2023

September’s manufacturing PMIs suggest that global industrial activity stagnated at the end of Q3, and forward-looking indicators point to further weakness ahead. The recent rise in oil prices seemed to push up the prices of manufactured goods. But …

2nd October 2023

Global goods trade fell at its fastest pace since the pandemic in July and the timelier trade and survey data point to further declines in August and September. What’s more, given that we still expect several advanced economies to fall into mild …

28th September 2023

The September Flash PMIs add to evidence that economic activity in the US and Europe is weakening. This supports our view that the Fed, ECB, and Bank of England have finished hiking interest rates. Our estimate of the DM average composite PMI edged down …

22nd September 2023

We held a Drop-In yesterday to discuss the latest policy meetings of the Fed, ECB, and Bank of England and what they might mean for the future path of policy and financial markets. (See the recording here .) This Update answers several of the questions …

Despite all the talk of “higher for longer”, we believe that the global monetary policy tightening cycle is drawing to a close. In Q4, any final rate hikes in advanced economies will coincide with a number of cuts in emerging markets. And as we head into …

21st September 2023

On Tuesday 19th September, our Energy and Global Economics teams discussed the oil market outlook and its implications for inflation and monetary policy in an online briefing for clients. Watch the recording here . We are not convinced that the increase …

19th September 2023

While economic activity was generally more resilient than feared in the first half of 2023, there are growing signs that many major economies are losing momentum. We expect most advanced economies to experience mild recessions in the quarters ahead as …

14th September 2023

Although wage growth is clearly falling in the US, the same cannot be said for the UK and euro-zone despite some evidence of labour markets cooling there too. A further fall in inflation expectations and an easing in worker mismatches is probably needed …

13th September 2023

The G20 summit which concluded yesterday in New Delhi supported our view that the global economy is fracturing into US and China-led blocs, and that India still leans to the former. While the statement was light on explicit policies, calls to increase …

11th September 2023

Developments in the past few weeks have moved the dial somewhat on the global story. In major DMs, there have been more signs of activity softening either in terms of output or employment, evidence of disinflation continues to mount, and it has become …

7th September 2023

Although a rise in Chinese manufacturing output meant that the decline in global manufacturing activity eased slightly in August, the outlook for industry in advanced economies in particular remains weak. Meanwhile, although the PMIs also pointed to a …

1st September 2023

Not only did global goods trade fall in June, but timelier trade and survey data for July and August point to further declines. Meanwhile, with the lagged impact of high interest rates likely to weigh more heavily on demand for certain goods, it could be …

31st August 2023